What are Emerging Markets

There is no standardised official definition for Emerging Markets (EM), however, the International Monetary Fund (IMF) labels certain countries as “emerging markets” based on economic factors such as their integration into the global financial system, population demographics like per capita income, liquidity and depth of capital markets, and the nature of a country’s trade balance (exports/imports). Emerging markets are considered less mature than developed markets, however, they are advanced compared to frontier markets.

Some of the dominant emerging markets include South Korea, India China, Saudi Arabia, Brazil, Taiwan, Thailand, Indonesia, Malaysia, Singapore, Hong Kong, South Africa and Turkey. Emerging markets offer growth and diversification opportunities for global portfolios; therefore, it is good time to review them as we start 2023 with renewed hopes after a tough year for financial markets

We will share both the case for and against emerging market equities.

A case for investing in Emerging Markets

• Emerging markets equities can potentially do well after crisis

Emerging markets had a worse turmoil last year as almost all the financial markets closed the year with significant drawdown in asset values as a result of multi-decade high inflation, central banks’ hawkish approach, global supply chain disruptions, and Russia-Ukraine war. The MSCI EM Index went down 21% in 2022 and 30% from the peak of May 2021. Although it is up about 9% in the first moth of 2023, however, it is still 24% down from the May 2021 level.

There are many factors behind this poor performance, including high inflation, rising interest rates in the developed economies, geopolitical and supply chain issues and rising global recession worries amongst other country specific factors. Moreover, China’s crackdown on technology giants and homebuilders, and zero covid policy has had a negative impact on MSCI EM Index performance. The global energy prices and strong US dollar put further pressure on EM asset valuations. The MSCI EM Index is trading at about 10x forward earnings and the MSCI China Index at 8x forward earnings, while the S&P 500 Index is trading at around 17x forward earnings.

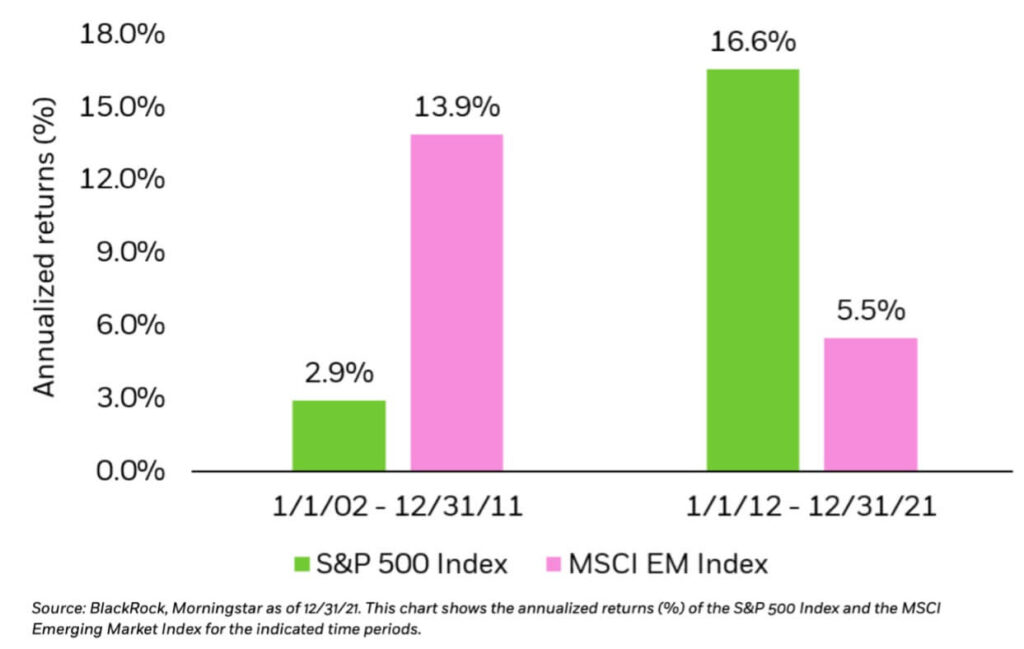

It is difficult to predict what the next decade brings for emerging market equities, however, having a look at the last two decades can offer some insights. The S&P 500 Index outperformed the MSCI EM Index with a wide margin due to the boom in US tech sector in the last decade that started from 2012 (see chart below). However, MSCI EM Index significantly outperformed S&P 500 Index in 2002 to 2011 time slot, and that was the decade when we saw the Global Financial Crisis (GFC) of 2007-08. As US markets are trading at about 60% premium to MSCI EM Index, therefore, a reasonable allocation to EM can be a prudent decision particularly during periods of high market and economic uncertainty in the developed economies.

MSCI EM Index vs. S&P 500 Index performance 2002 – 2021

• Pro-growth stance in China

Economists believe China will prioritise its economic growth over other issues that have been the central focus in the last couple of years. The most important trigger would be the end of zero covid policy that China had pursued. The opening of the world’s largest population and second largest economy will boost its consumer demand and GDP growth. Overtime, China is expected to be highly integrated with the emerging and frontier markets through its belt and road initiative, this will help China and connected economies. Moreover, China is better able to stimulate its economy as it did not experience high inflation and rising interest rates as is the case with developed economies.

• Industry leading companies offering enhanced Alpha potential

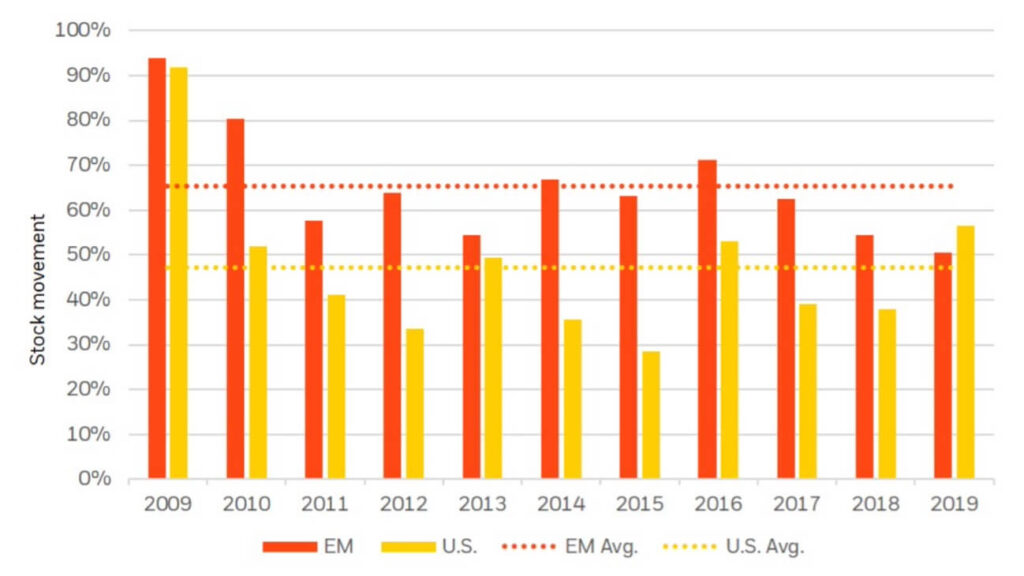

Although emerging markets are still developing but many companies are doing great and are already leaders in their respective industries. For example, Asia is known to be the hub of semiconductor chips technology with significant economic moat. Samsung, Taiwan Semiconductor Manufacturing Company, and Mediatek are few of the names that have revolutionised the world modern technologies supported by semiconductors and chips. Who is unaware of BYD, China’s largest and fast-growing EV maker. These are just a few of many promising opportunities out there to explore in emerging markets. Blackrock shows (graph below) that, “over the past decade, about 65% of EM stocks moved by at least 40% annually”. This indicates that many companies offered the possibility of a high relative return.

Emerging markets companies’ Alpha potential (number of stocks moving 40% or more in price annually)

• Strength of the US dollar possibly peaking soon

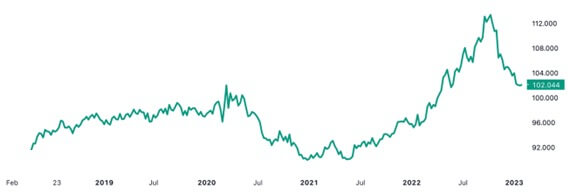

US dollar showed its muscle last year when the Fed started hiking interest rates to combat 40-year high inflation. Strong US dollar is never good news for emerging markets as the cost of many commodities and energy products increased due to import-oriented economic systems. As evident in recent months, US dollar may already have peaked (chart below) as inflation outlook is softening and the pace of hiking interest rates is slowing. The Fed is expected to halt hiking rates in coming months and then may start pivoting towards the end of the year or start of the next year if they get inflation under control. Emerging markets’ currencies will experience appreciation when dollar start weaking. Furthermore, commodity prices can gain momentum due to economic growth and rising demand in emerging markets.

US Dollar Index

• Attractive valuations

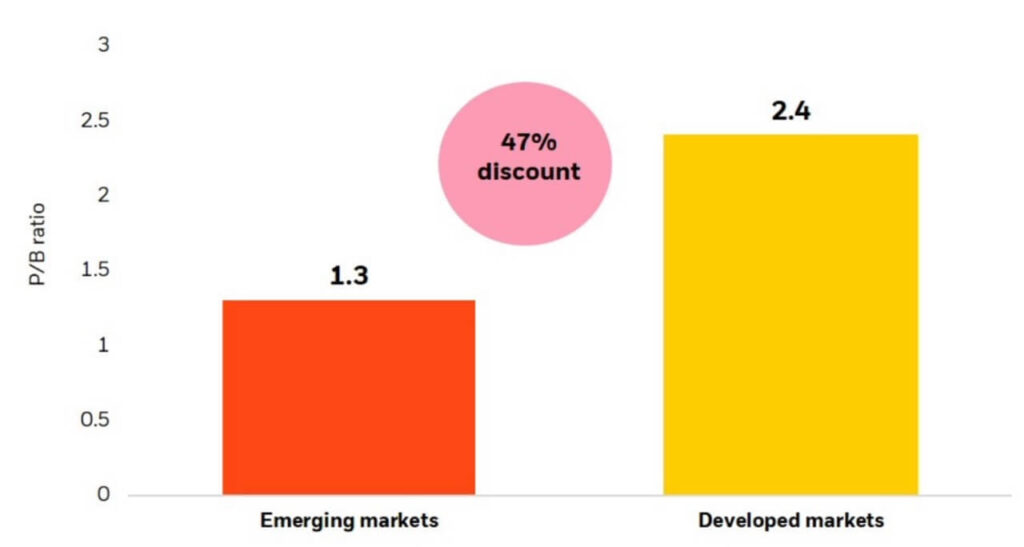

Emerging markets are offering deep discount relative to developed markets, although this discount is partly justified as these markets are generally riskier (potential risks are discussed in the following sections). Price to earnings (P/E) and price to book (P/B) ratios are two of the most widely used yardsticks to value assets and markets. At noted earlier, the emerging markets are cheap in terms of P/E multiples of MSCI EM Index vs. S&P 500 Index. P/B ratios (see chart below) also favour emerging markets as the discount is as high as 47%. The valuation picture indicates that emerging markets are well positioned to offer better capital growth opportunities, on selective basis, in the next decade.

Price-to-book ratios – emerging markets vs. developed markets (May 29, 2020)

A case against investing in Emerging Markets

The case for emerging market equities looks interesting, however, it is not free of risks. Apparently, low valuations offer much needed conviction to allocate a good portion of the portfolio to emerging markets, nonetheless, low valuations might be due to valid reasons. In this section, we will see some of the most critical risks to emerging market equities.

• Emerging markets are relatively more volatile than developed market

It is generally believed that emerging market equities tend to be more volatile as compared to their developed counterparts. Over the last 10 years, the average standard deviation in emerging markets is 18 vs. 14 in developed markets. High volatility is a friend of few but an enemy of most retail investors. This heightened volatility comes from political risks, monetary policies uncertainties, economic vulnerabilities, swings in the commodity prices, lack of depth and liquidity in the market, and many other factors.

• Currency risk

Emerging market currencies posit a significant threat to foreign portfolio investments. Although emerging market currencies are expected to gain as the US dollar weakens in coming years but that may not turn out to be the most likely scenario. Recent decades-long history tells us that emerging market currencies have been weakening against US dollar. If that trend continues in the next decade, international investors may not materialise the anticipated gains as increase in asset values could be offset, at least partly, by the loss in currency values.

• Other challenging factors

Quality research is an important ingredient for successful investment. Stock selection could present a challenge for potential EM equity investors as conducting research is hard due to lack of appropriate data bases and sometimes misrepresentation of financial results. Another factor against emerging market equities is the high cost of investing compared to developed markets, partly attributed to less developed financial infrastructure and lack of market efficiencies. In general, the annual management charges for an emerging markets fund/ETF are much higher than those for developed markets.

Lastly, macroeconomic picture is still blur for emerging markets. Global inflation is still not under control and rates are rising globally that is likely to hurt export-led economies, as demand contracts. The risk of global supply chain disruptions and further escalation of Russia-Ukraine war could yet again translate into food and energy crisis that can hit emerging markets harder than the developed markets, due to greater dependence on import of energy in particular. That extreme scenario would be bad news for emerging market investors as capital flight is a real phenomenon for these markets.

And finally ….. have an open discussion with your Financial Adviser

Keeping calm and controlling your emotions during increased market volatility is difficult but it is the right thing to do. However, if you feel nerves and need assistance, talking to your Financial Adviser is always fruitful.

You can book a free consultation with one of our Financial Advisers to learn more about our investment approach and how we can help you.

Disclaimer

Financial Data as of 27th January 2023. Past performance is not a reliable indicator of current or future returns. This overview contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.