The first quarter of 2021 has been a positive start to the year for the British economy where COVID-19 vaccine roll-out has been relatively successful whilst the country remained mostly in lockdown. Over 50% of adults have been vaccinated and the case numbers have dropped rapidly. England took on March 29th a significant step towards easing lockdown restrictions, with people being allowed to meet in groups of up to six or as two households and outdoor team sports reopening. Elsewhere in Europe, surging infections and the extension of restrictive measures were still in place, although vaccine rollout continues to gather momentum. Globally, government policy initiatives continue to remain supportive of economic activity. Nevertheless, rising inflation and budget deficit in a number of economies does pose an emerging challenge for the policy makers. The recent spike in COVID-19 cases in developing economies, particularly in India is somewhat concerning.

Europe:

The Eurozone economy shrank by 0.5% on quarter in the three months to December 2020 (see chart). The latest reading followed a record 12.5% expansion in the previous three-month period and an unprecedented 11.8% contraction in the second quarter due to the COVID-19 crisis. Among the bloc’s largest economies, France, Italy and the Netherlands contracted in the fourth quarter, while GDP growth in Germany and Spain slowed sharply. Year-on-year, the GDP shrank by 5%. The European Central Bank decided on March 11th to leave its Pandemic Emergency Purchase Program (PEPP) unchanged, at a total of €1.85 trillion ($2.21 trillion) due to last until March 2022. The ECB has said it expects to increase bond purchases significantly next quarter after borrowing costs rose in the Euro area. Annual inflation rate in the Euro Area jumped to 0.9% in January, the most in 12 months, ending 5 months of deflation. The Eurozone consumer price inflation is expected to accelerate to 1.3% in March, the highest since January 2020 and in line with market expectations, a preliminary estimate showed. Energy prices should rebound firmly and services inflation is seen picking up slightly, signalling a gradual recovery in domestic demand. Meanwhile, the annual core inflation, which excludes volatile items and at which the ECB looks in its policy decisions, is expected to slow to 0.9%.

The German economy expanded 0.3% on quarter in Q4, much better than initial estimates of a 0.1% growth, led by construction, inventories and exports while both consumer and government spending shrank due to another coronavirus lockdown imposed from November. Considering full 2020, the GDP contracted by 4.9%. The GDP is seen growing 3% in 2021 according to government forecasts. Retail sales in Germany dropped 4.5% mom in January, following a downwardly revised 9.1% plunge in the previous month as the country remained under a second coronavirus lockdown. The number of unemployed people in Germany rose by 9 thousand to 2.752 million in February 2021, following a revised 37 thousand decrease in the previous month. The jobless rate was unchanged at 6.0%. Germany recorded a €189.2 billion budget deficit in 2020, the first gap since 2013 and the highest since the German reunification 30 years ago, due to the coronavirus pandemic. It compares with a €45.2 billion surplus in 2019.

We are starting to see inflationary pressures in a number of economies. Annual inflation rate in Germany was confirmed at 1% in January of 2021. It is the first increase in consumer prices in 7 months as higher VAT rates were passed on to the consumers after the temporary reduction in VAT, which was a measure of the Federal Government’s stimulus package, ended on December 31st, 2020. Based on preliminary estimate, Germany’s consumer price inflation rate is expected to pick up to 1.7% year-on-year in March, the highest since February 2020. Meanwhile, annual inflation rate in France increased to 1.1% in March of 2021, the highest since February of 2020. On a monthly basis, consumer prices went up 0.6. the highest monthly rate since March of 2019. Norway’s annual inflation rate increased to 2.5% percent in January of 2021, the most since May 2019, from 1.4% in December 2020 and beating market expectations of 1.7% percent.

UK:

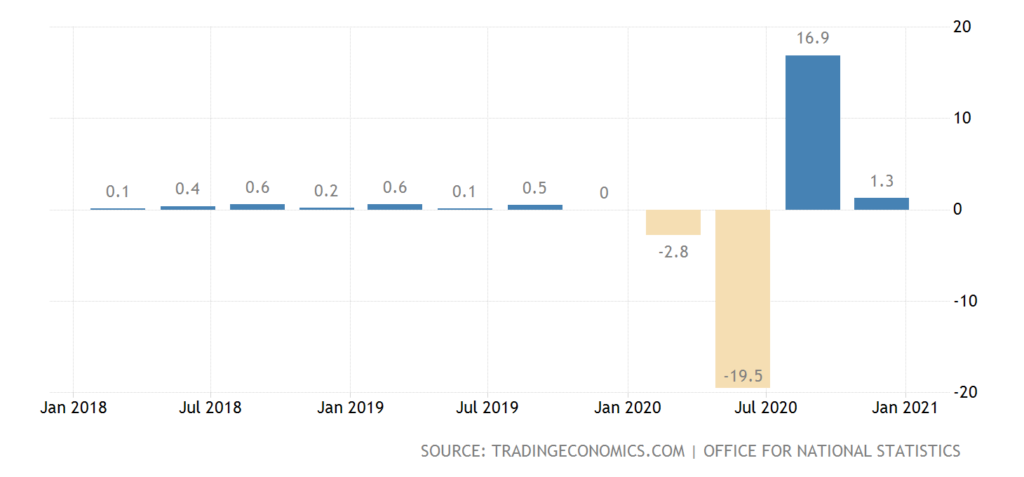

According to ONS figures, the British economy expanded 1.3% on quarter in the last three months of 2020, higher than 1% in the preliminary estimate. Q3 figures were revised up to show a 16.9% growth. Despite two consecutive quarters of growth, the level of GDP was still 7.3% below its pre-pandemic level. The levels of business investment and household consumption remain 7.4% and 9.2% lower than their pre-pandemic levels respectively. Over the year 2020 as a whole, GDP contracted by 9.9%, the largest annual fall on record. Britain’s government budget deficit hit a peacetime high of £355 billion, or 16.9% of GDP, in the 2020-21 fiscal year as a result of efforts to support businesses and households hit by the pandemic. On March 3rd, the UK Chancellor Rishi Sunak extended the government’s furlough scheme until the end of September. Other measures included an extension of both the universal credit uplift and the reduced rate for VAT on hospitality and tourism amongst other initiatives. Looking ahead, according to Office of Budget Responsibility, the government borrowing is set to fall to 10.3% of GDP in 2021-22 and 4.5% of GDP in 2022-23.

UK Quarterly GDP – Total, Percentage change, previous period

The Bank of England voted unanimously to keep its benchmark interest rate on hold at a record low of 0.1% and to leave its bond-buying programme unchanged during its March 2021 meeting, saying the UK GDP was projected to recover strongly over 2021 towards pre-Covid levels and CPI inflation was expected to return towards the 2% target in the spring. Annual house price growth in the UK accelerated to 6.9% in February of 2021 from a 6.4% in January. On a monthly basis, prices jumped 0.7%, following a 0.2% decline in January. The number of mortgage approvals for house purchase in the UK decreased to 99,000 in January 2021, slightly down from a revised 102,800 in the previous month but above market expectations of 96,000. The number of approvals, which is an indicator for future lending, was also well above the monthly average in the six months to February 2020 (67,900). Meanwhile, households’ consumer credit dropped by £2.4 billion in January, the most since last May. As a result, consumer credit declined 8.9% yoy, the biggest fall since the series began in 1994.

Britain’s retail sales rose in March by the most since June’s record increase, while PMI data suggested the country’s private sector output grew by the most since November 2013, reflecting the effect of the easing of coronavirus restrictions on consumer spending. In addition, British manufacturers’ expectations of an economic rebound rose to their highest since 1973 this month; the UK inflation rate advanced less than expected to 0.7% in March; and Britain’s unemployment rate fell for a second month in a row to 4.9%, even as the number of employees on company payrolls continued to fall.

US:

The US GDP grew an annualized 4% on quarter in Q4 2020, slowing from a record 33.4% expansion in Q3 when the economy started to recover from the coronavirus hit, lockdowns and business closures. Considering full 2020, the economy likely contracted 3.6%, the worst performance since 1946, and following 2.2% growth in 2019. The outlook for 2021 seems brighter than it was some months ago as vaccination rollout began although at a slower than expected pace and in early March the Democrats approved a massive $1.9 trillion coronavirus relief package and more recently, President Biden unveiled a $2.25 trillion infrastructure plan to boost the economic recovery. The US posted a budget deficit of $311 billion in February 2021, compared with a $235 billion gap in the same period last year.

Meanwhile, the Fed left the target range for its federal funds rate unchanged at 0-0.25% during its March meeting, and signaled a strong likelihood that there may be no rate hikes through 2023. Policymakers noted that indicators of economic activity and employment have turned up recently, although the sectors most adversely affected by the pandemic remained weak. Federal Reserve head Jerome Powell once again downplayed concerns about higher interest rates and inflation, while US Treasury Secretary Janet Yellen said that future tax hikes would likely be needed to finance future government spending. The US consumer price inflation jumped to 2.6% in March of 2021 from 1.7% in February, the highest since August 2018 and above market consensus of 2.5%, with main upward pressure coming from energy. On a monthly basis, consumer prices increased 0.6%, the most since 2012. The effects of the coronavirus pandemic are weighing on prices since in March 2020 many businesses closed and lockdowns were imposed, denting economic activity. Also, a jump in commodities and material costs, coupled with supply constraints, are pushing producer prices up and some companies are passing those costs to clients.

Japan:

The Japanese economy advanced 2.8% on quarter in the three months to December of 2020, following a 5.3% growth in the previous period. For the whole of 2020, the world’s third-largest economy shrank 4.8%, marking the first contraction since 2009. The Bank of Japan left its key short-term interest rate unchanged at -0.1% and maintained the target for the 10-year Japanese government bond yield at around 0% during its March meeting. Meantime, the central bank decided to widen the band at which it allows long-term interest rates to move around its 0% target and pledged to buy ETFs only when necessary, instead of at a set annual pace. Japan’s consumer prices declined 0.4% year-on-year in February 2021, after falling 0.6% in the previous month, as the pandemic continued to impact consumption. On a monthly basis, prices increased 0.1% after a 0.6% jump in January.

Emerging economies:

The Chinese economy advanced 6.5% yoy in Q4, after a 4.9% growth in Q3 and above market consensus of 6.1%. For full 2020, the GDP expanded 2.3%, the slowest pace in more than four decades. Still, China is likely to be the only major economy to avoid a contraction in 2020. The consumer price index in China dropped by 0.2% yoy in February 2021, after a 0.3% fall a month earlier. This was the second straight month of deflation, as prices fell for both food and non-food. On a monthly basis, consumer prices rose by 0.6% in February, the third straight month of gains. China’s banks extended CNY 1.36 trillion in new yuan loans in February of 2021, below a record of CNY 3.58 trillion in January but well above market forecasts of CNY 0.95 trillion. It is also higher than CNY 0.91 trillion a year earlier. Loans tend to be higher in the beginning of the year as banks try to get more higher-quality customers and win market share and as the PBoC makes regular liquidity injections to raise cash available ahead of the Lunar New Year holidays. This year however, the central bank has been withdrawing money from the market, raising concerns about monetary policy tightening. The bank withdrew CNY 80 billion right before the Lunar New Year. China has set its 2021 economic growth target at over 6%. Chinese leaders intend to keep consumer price inflation at around 3% and seek a budget deficit of about 3.2% of the GDP. The government also aims for an urban unemployment rate of approximately 5.5% and plans to create more than 11 million new urban jobs.

Russia’s GDP shrank 1.8% year-on-year in the fourth quarter of 2020, easing from a revised 3.5% contraction in the previous three-month period and a 7.8% slump in April-June. The hotels & restaurants sector continued to be the biggest driver of the contraction, falling 20.7% from a year earlier. Considering 2020 as a whole, the economy shrank 3%, compared with a 2% expansion in 2019. The Bank of Russia raised its benchmark interest rate by 25 bps to 4.50% during its March 2021 meeting, surprising markets that had expected the rate to remain unchanged at a record low of 4.25% and opening the prospect of further increases at its upcoming meetings. Policymakers voiced concerns about higher-than-expected consumer price growth during the first quarter, adding that inflation expectations remained elevated. Looking ahead, annual inflation is seen returning to the central bank’s target close to 4% in the first half of 2022 and remain at that level further on.

The Turkish economy expanded 5.9% year-on-year in the last three months of 2020. Considering full 2020, the economy expanded 1.8%, above 0.9% in 2019, as a near doubling of lending by state bank in the second half of the year was able to partially offset the effects of the coronavirus curfews, restrictions and curbs on business. The central bank of Turkey kept its benchmark one-week repo rate steady at 17% on January 21st 2021, in line with expectations, following a 200bps rise in the previous month. The inflation rate in Turkey increased to 14.6% in December, reaching the highest level since August of 2019. The Turkish lira traded around 7.8 per USD on March 22nd after tumbling as much as 15% to hit a near record low of 8.5 after President Tayyip Erdogan abruptly fired the country’s central bank chief, who had restored some confidence in the country’s monetary policy and has been considered the mastermind behind the currency recent strength. The move came two days after the central bank raised interest rates by 200 basis points.

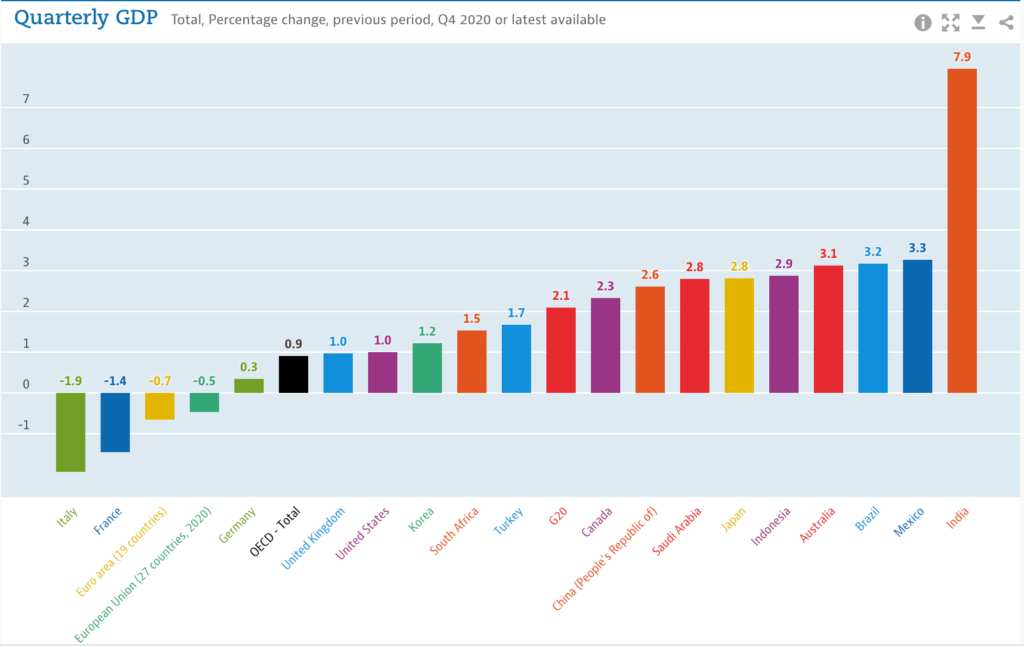

India was the best performing economy in Q4, with a growth of 7.9%. Indian finance minister Nirmala Sitharaman unveiled the Union Budget 2021 and announced measures to revive the pandemic-hit economy. The government’s fiscal deficit for the current fiscal year to March 2021 is likely to reach 9.5%, compared with the budget estimate of 3.5%. For 2021/22 the minister projected a fiscal deficit of 6.8% of GDP. To help revive an economy that suffered its deepest recorded slump as a result of the pandemic the finance minister proposed doubling healthcare spending, a vehicle scrappage policy, recapitalization of public-sector banks and divestment of some state-owned lenders.

The OECD expects the world economy would grow 5.6% this year, compared to a 4.2% expansion expected in December, as vaccine rollouts gain momentum and government stimulus measures are likely to provide a major boost to economic activity. US GDP is seen rising 6.5% in 2021, while the Eurozone should expand by 3.9% and the UK by 5.1%. China is set to grow 7.8% and India will advance 12.6%.