In Q1 2026, global economies and financial markets were shaped by a complex mix of sticky inflation, uneven growth momentum, heightened policy uncertainty, and geopolitical risks. While inflation remained a key theme in some major economies, it remained sticky in core components, leading central banks to adopt a cautious and data-dependent approach to interest rate decisions. Growth indicators showed divergence, with the US remaining relatively resilient, while Europe and the UK experienced softer economic activity and China delivered on promised numbers despite ongoing structural challenges. Bond markets were volatile as expectations for rate cuts were repeatedly repriced, while equity markets saw increased dispersion between defensive sectors and growth-oriented technology stocks amid rising energy prices as geopolitical situation became more intensified. Currency markets reflected these dynamics, with the US dollar strengthening during periods of risk aversion. Overall, macroeconomic conditions in Q1 reinforced a cautious investment environment amid lingering inflation risks and fragile global growth.

The key macroeconomic indicators across major economies reflected a mix of resilience and fragility amid evolving policy and geopolitical dynamics. In the United States, growth remained relatively robust, supported by a strong labour market and steady consumer spending, although core inflation proved sticky, making the Federal Reserve’s job difficult. The Eurozone experienced subdued growth, with weak industrial output and cautious consumer demand, even as headline inflation edged closer to target, allowing the European Central Bank to signal a gradual shift toward policy easing. The United Kingdom saw modest economic activity with soft retail and housing data, while inflation, though declining, remained above target, constraining the Bank of England’s flexibility. In Japan, inflation stayed slightly above the Bank of Japan’s target, supported by wage growth, while economic expansion remained moderate, reinforcing a gradual policy normalization stance. Meanwhile, China showed uneven recovery trends, with improved manufacturing activity and targeted stimulus measures offset by weak property markets and subdued consumer confidence. Overall, Q1 highlighted divergent macroeconomic paths, with policymakers balancing growth support against lingering inflationary pressures.

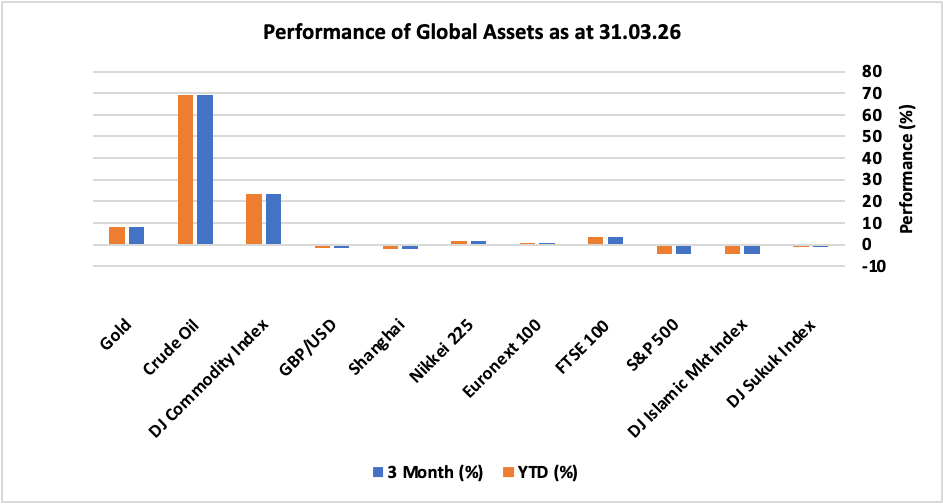

Looking at the performance, most of the major global financial assets experienced extreme volatility and negative momentum (except commodities) in Q1 amid geopolitical fears resulting from War in Middle East, despite resilient corporate earnings and positive developments in AI theme. US equity markets recorded significant losses as S&P 500 declined by 4.33% whereas DJ Islamic Markets Index booked negative 4.25% returns during the month. While in Europe, UK FTSE 100 and EU Euronext 100 delivered positive 3.42% and 0.77%, respectively, largely driven by higher energy sectors weight in the indices. In Asia, Japan’s Nikkei 225 rose by 1.44% while China’s Shanghai index tumbled 1.94%. DJ Sukuk Index ended the month down 1.14% amid rising yields whereas US dollar strengthened, which appreciated 1.71% against UK pound. In commodities, DJ Commodity index climbed by 23.5% driven by nearly 69% surge in Crude oil prices amid extreme geopolitical risks.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q1 2026, as well as their progress year-to-date.

Performance of global assets – Q1 2026

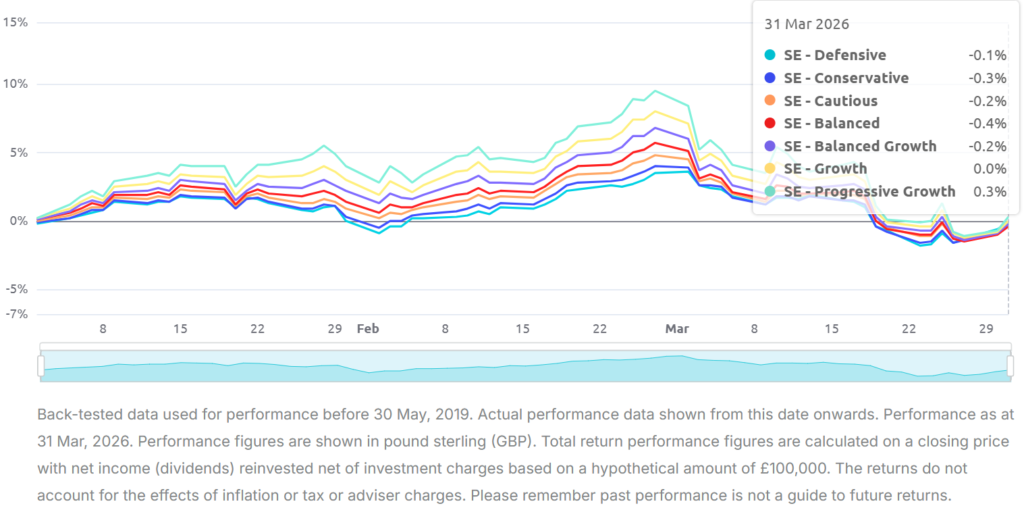

Portfolio Commentary

During the first quarter, all investment portfolios were marginally negative except Growth and Progressive Growth portfolios due to US-Iran war. In general, all our portfolios performed relatively better than the broader market because of higher allocation to European and Emerging Market equities, along with decent precious metals exposure.

Performance of Simply Ethical Online Portfolios in Q1 (01 January 2026 – 31 March 2026)

During the quarter, there were several changes made to the investment allocation for all portfolios. In the second half of January, we rebalanced all our portfolios to materialise gains on precious metals and equities in general. The broader asset allocation (split between sukuk, equities and commodities) remained constant. However, given our cautious stance on certain segments of US equities, we had reduced the exposure to US in favour of Europe and Emerging Markets – this certainly helped maintain the portfolio values during the quarter.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.