Economic and Market Overview

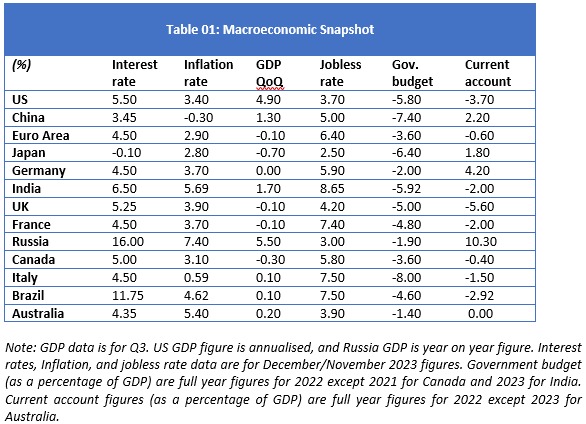

Q4 of 2023 has been good for investors as markets celebrated an upright run after difficult months in summer. Falling inflation numbers in all the major economies compel the policy makers to change their hawkish tone. Now it looks like the rates have peaked and they are possibly expected to start coming down in coming months. Despite the high-speed increase in interest rates, economies showed resilience and unemployment rate remained moderate. Amongst key economies, the recent inflation figures show a decline in the US, UK, Euro-Area, and Brazil, whereas inflation remained steady in Canada but rose in Russia. During the quarter, all key central banks including the Federal Reserve, the Bank of England and ECB kept interest rates unchanged. Moreover, the Federal Reserve signaled that there will be at least three rat cuts in 2024, although markets are pricing more than that. On the GDP growth front, recent figures show a mixed picture where we can see a growth in the US, but negative growth in the UK and Euro-Area. Unemployment rate marginally fell in the US and Euro Area but remained steady in the UK and China. Meanwhile, China’s economy showed some signs of improvement driven by number of stimulus initiatives taken by the government. However, those measures failed to get the economy out of deflationary conditions. The overall outlook for the Chinese economy remains uncertain, amid weak overseas demand and a property downturn. The key events pricing in are growth concerns, mixed economic data, and geopolitical tensions, which are weighing on investors’ enthusiasm for equities in the region.

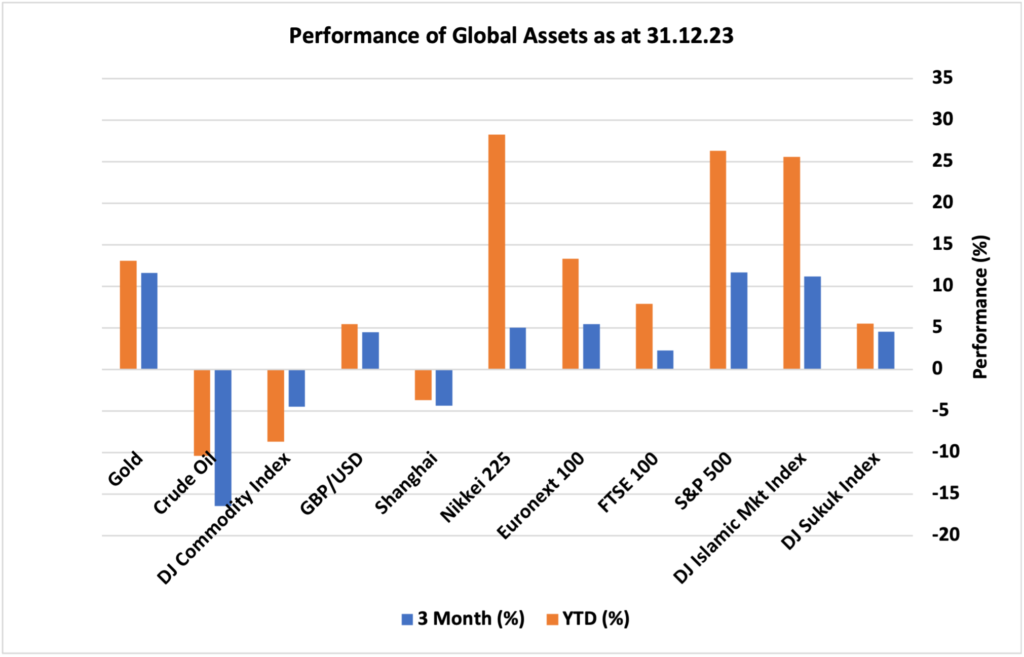

Looking at the performance of major asset classes over the course of Q4 2023, equity markets rebounded strongly after a sluggish summer amid falling inflation levels in all major economies and the signals from central banks that interest rates will start falling in the first half of next year. S&P 500 index was the leader with 11.7% quarterly return followed by DJ Islamic markets index with 11.2% and 2.81%. Europe’s Euronext 100 and Japan’s Nikkei 225 rose by 5.44% and 5.04%, respectively. UK FTSE 100 returned only 2.31% mainly because of its high exposure to energy (which dropped in value significantly in the quarter) and international exposure that had a weigh on its performance due to currency exposure (UK Pound appreciated against US Dollar in the quarter by 4.5%). China’s Shanghai Index fell 4.36% as there are still concerns of deflation and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing. On an annualized basis, equity markets booked 2023 as one of the best performing years in the equity markets recent history. Gold returned 11.6% amid falling US dollar against pound and concerns over slowing global economy. DJ sukuk index surged 4.54% in the fourth quarter amid falling yields as market consensus is shifting towards interest rates cut in the first half of 2024. Commodities remained under pressure where crude oil fell over 16% amid concerns over slowing global economy after historic speed of rates hike and struggling world’s second largest economy. Overall, DJ Commodity Index dropped by 4.49% in last quarter of 2023.

Performance of global assets Q4 2023

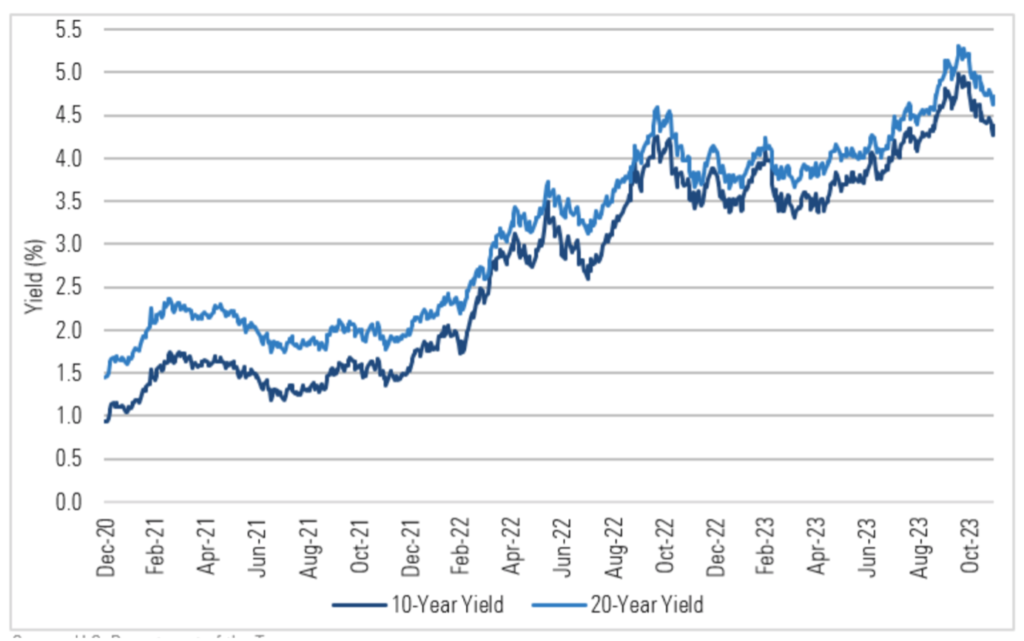

One of the fastest moving rate hike cycles in the recent history posed a challenge for fixed income investors. Bonds yields touched 5% level in August 2023 that resulted into a substantial drop in bonds portfolio values. Bonds’ values fall when yields rise and vice versa. However, when central banks signalled in the latter half of the year that interest rates are at their peak levels and they might start cutting rates next year after holding them steady in three consecutive meetings, bonds yields started falling sharply from 5% towards 4% in Q4 2023. This reversal in yields helped bonds values to start recovering. Many asset managers preferred to lock-in the high yield for years to come to boost portfolio returns through high yields and capital gains in the falling rates environment in the years to come.

10- and 20-Year Treasury Yields

Key News & Events in Q4 2023

UK

It appears that the monetary tightening cycle has peaked as the Bank of England kept interest rates steady at 5.25% during the quarter. In its recent meeting in December, the Bank of England held its policy interest rate at 5.25% keeping borrowing costs at their highest level since 2008, as policymakers opted for a ‘wait and see’ approach following the latest inflation and labour data, which suggested that monetary tightening may be taking effect with lags. The central bank has not increased rates after August 2023. The most recent published inflation figure for November shows inflation easing to 3.9%, although still a long way off from the central bank’s inflation target of 2% but rates are moving in the right direction. This marked the lowest rate since October 2021, mainly due to a slowdown in energy and food inflation and a decline in the cost of accommodation services. Meanwhile, unemployment rate has not changed since June 2023, which remained at 4.2% as per the latest October 2023 data, the highest level since October 2021, indicating that the labour market may be cooling off. Moreover, the UK economy is showing weaknesses where UK quarterly economic growth was confirmed at negative 0.1% during the third quarter of 2023.

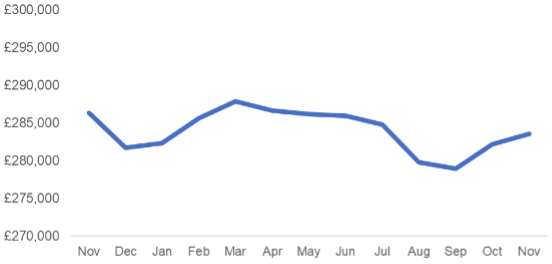

The UK housing market has been struggling throughout the year as prices declined mainly due to higher mortgage costs after a fast interest rate hike cycle. However, in the fourth quarter of 2023, house prices recovered some of their lost values mainly driven by the hopes that interest rates have peaked, and easy monetary policy era is coming soon. This expectation pushed mortgage rates down as lenders are adjusting their policies to remain competitive in the market. The Halifax House Price Index shows that average house prices are back to around £284,000 in November after touching £278,000 in September, recording just over 2% price appreciation in Q4 2023.

Average UK house price: 12 months to November 2023

US

The US Federal Reserve (Fed) looks to soften its stance towards monetary policy based on recent macroeconomic data. The Fed kept the target range for the federal funds rate at a 22-year high of 5.25%-5.5% in its December 2023 meeting. Throughout the Q4, rates remained at that level, however, outlook has shifted from ‘higher for longer’ to at least three rate cuts in 2024. The minutes from December FOMC policy meeting show that members indicated they expect three quarter-percentage point cuts by the end of 2024. This policy stance change in Q4 is based on the fact that inflation is moving down to Fed’ 2% target. The chairman of the Fed Jay Powell said “you would not wait for the inflation to go down to 2% before you start cutting rates, you would start doing that beforehand as the impact of these polices works in lags.” The annual inflation rate fell to 3.1% in November, the lowest level since July 2023. Unemployment rate came down to 3.7% in November from 3.8% in October, indicating that the labour market remains tight based on historical standards.

On the growth front, GDP in Q3, 2023 was stronger than previous quarters at 4.9% (slightly below the 5.2% estimates), compared to just over 2% in the previous two quarters driven mainly by government spending, robust non-residential investments, and resilient consumer spending. It looks like the covid era savings is still helping consumption levels to remain resilient and they are having their impact on economic growth. On the fiscal side, the US debt is at all-time high, crossing $34 trillion in December 2023. This could have serious implications in the US as well as throughout the world because of contagion effects if the ability to payback deteriorates. While the US federal debt has risen faster in recent years, higher interest rates pose the added challenge of sharply higher annual interest payments. However, when rates begin to ease, this will relieve some pressure, but mounting government debt remains a broader-term risk.

Europe

GDP growth in Euro Area is slowing in recent quarters and it has turned to negative 0.1% in Q3 of 2023 where Germany, France, and Netherlands contributed the most in this contraction. According to experts, GDP growth rate in Euro Area is expected to be 0.30% by the end of Q4. In the long-term, the Euro Area GDP growth rate is projected to trend around 0.30% in 2025. Although the inflation was seen moderating throughout 2023, however, it spiked to 2.9% in December from 2.4% in November, primarily driven by energy-related base effects. On the policy front, the ECB kept interest rates at the same level to 4.5% in its December meeting and signalled that it is likely done tightening policy, as inflation has taken a falling path. Unemployment in the block remained low in Q4 and fell to 6.4% in November from 6.5% in the previous month. The central bank has also significantly reduced its GDP growth projections, now anticipating the economy to expand by 0.7% in 2023, 1% in 2024, and 1.5% in 2025.

China

China’s central bank is pushing for economic stimulus policy by keeping interest rates at low levels. Rates remained at 3.45% throughout Q4 2023. This initiative is mainly driven by deflationary environment in the country where the economy is struggling to achieve its desired growth. The rate of inflation fell to negative 0.5% in November from negative 0.2% in October. Deflation is a killer for the economy as businesses get hard to make decent margins and remain competitive. The Chinese economy grew by a seasonally adjusted 1.3% in Q3 of 2023, ahead of market expectations of 1% and accelerating from 0.5% increase in Q2. This recorded the fifth consecutive period of quarterly expansion, driven by monetary stimulus measures over the past three months, including interest rate cuts and constant liquidity injections by the country’s central bank. However, the property sector remained a drag on the economy, as China’s biggest property developers faced a large-scale default.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.