Economic and Market Overview

After a good first half of the year for equities, in Q3 major equity markets dropped in value on concerns over the possibility of interest rates remaining higher for longer than anticipated. The yield on the US 10-year Treasury note rose by almost 19% in Q3 from 3.86% to 4.58%, following comments from the Fed that it would cut interest rates more slowly than markets have priced in. The 10-year US Treasury benchmark hit a yield of 4.88% in early trading on Tuesday, October 3rd – its highest yield in 15 years.

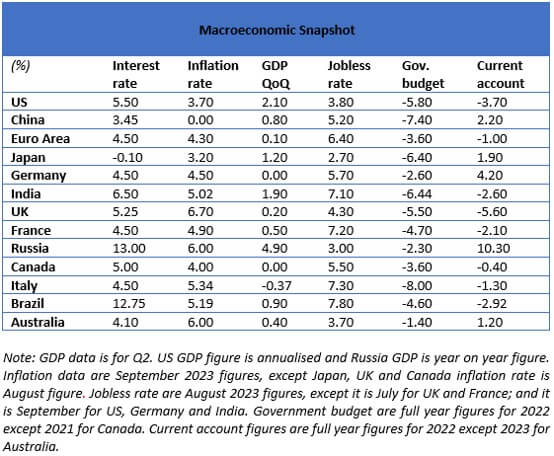

Macroeconomic picture remains challenging as both interest rates and inflation remains high, particularly in developed economies. Amongst key economies, the recent inflation figures show a decline in the UK and Euro-Area, but no change in the US, whereas inflation rose in Canada, Russia and Brazil. During the quarter, all key central banks including the Federal Reserve, the Bank of England and ECB raised interest rates. During recent meetings in September, both the Federal Reserve and the Bank of England held its policy rate at 5.25% and 5.5% respectively, but the ECB hiked interest rates to 4.5%.

On the growth front, recent figures show growth in the US, UK and Euro-Area, however, unemployment data presents a mixed picture. Unemployment in Europe drops, whilst remains somewhat volatile in the US during the year. In the UK, unemployment starts rising based on July data and moreover the house prices continue to decline. Meanwhile, China’s economy showed some signs of improvement in August, particularly in industrial production and retail sales. Inflationary conditions also improved after China slipped into deflation earlier this year. However, the overall outlook for the economy remains uncertain, amid weak overseas demand and a property downturn.

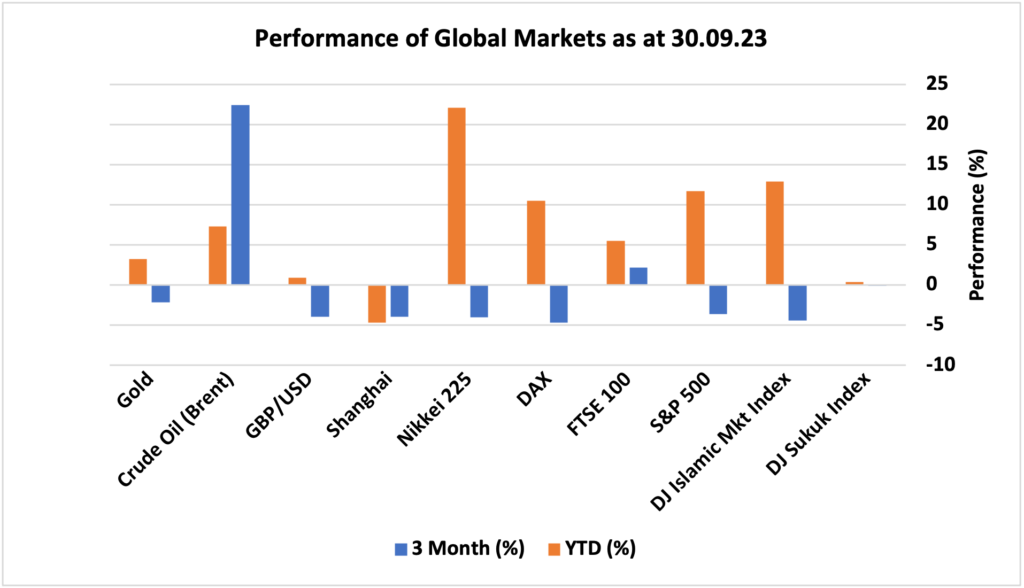

Global equity markets dropped in value during the third quarter with DAX Xetra (Germany) and DJ Islamic Market Index depreciating by 4.71% and 4.43%, respectively. Returns in Q3 have diverged, but still dominate YTD results for US equities as the market has been driven by outsized performance from the ‘Magnificent 7’ to start the year. Japan’s Nikkei 225 Index dropped by just over 4%, however, remains one of the best performing markets since the start of the year. Meanwhile, the UK FTSE 100 index rose just over 2% partly due to its tilt towards energy sector, which was supported by rise in oil prices. Commodities were positive in Q3 as energy prices rose, gold fell pressured by a strong US dollar and higher US Treasury yields. Oil prices rose to over $90 a barrel during Q3 in response to the OPEC+ announcement of extended production cuts through year-end. Recent escalation in Israel-Palestine conflict is expected to keep oil price volatility and at higher levels, at least for the short term – this is likely to make things challenging for policy makers.

UK

Monetary tightening continued as the Bank of England raised interest rates by 25bps to 5.25% during the quarter. In its recent meeting on September 21st, the Bank of England held its policy interest rate at 5.25% keeping borrowing costs at their highest level since 2008, as policymakers opted for a ‘wait and see’ approach following the latest inflation and labour data, which suggested that monetary tightening overtime may be taking effect. It was the first pause in policy tightening in nearly two years, following the central bank’s extraordinary 515 bps hikes. The most recent published inflation figure for August show inflation easing to 6.7%, although, still a long way off from the central bank’s inflation target but in the right direction. This marked the lowest rate since February 2022, mainly due to a slowdown in food inflation and a decline in the cost of accommodation services. Meanwhile, unemployment rate rose to 4.3% in May to July 2023, the highest level since the third quarter of 2021, indicating that the labour market may be cooling off. However, the UK economy continues to grow albeit at a smaller rate. The UK quarterly economic growth was confirmed at 0.2% during the second quarter of 2023.

The UK housing market has been struggling as prices decline mainly due to higher borrowing costs. According to many experts, the downward pressure on house prices is likely to extend into next year due to many factors. The Halifax House Price Index dropped by 4.7% yoy in September 2023. It was the biggest fall in house prices since August 2009. A typical UK home now costs £278,601, around the level seen in early 2022. According to Kim Kinnaird, director of Halifax Mortgages, “Activity levels continued to look subdued compared to recent years, with industry data showing lower levels of new instructions to sell homes and agreed sales”.

UK Average House Prices

US

The Federal Reserve kept the target range for the federal funds rate at a 22-year high of 5.25%-5.5% in its September 2023 meeting, following a 25bps hike in July. The minutes from September FOMC minutes show that policymakers are inclined to keep interest rates elevated for an extended period, with the next moves being uncertain and contingent on economic data. A majority of Fed policymakers judged that one more increase in the federal funds rate at a future meeting would likely be appropriate, while some judged that no further increases would be warranted. However, all agreed that policy should remain restrictive for some time until inflation moved down sustainably to 2%. The annual inflation rate remained steady at 3.7% in September, whilst unemployment remains somewhat volatile (moving up and down within 3.4% to 3.8% band, without any consistent trend) particularly over the past 18 months. US unemployment rate was 3.8% in September indicating that the labour market remains tight based on historical standards, but expected to ease in coming months. Meanwhile, growth in Q2, 2023 was stronger than expected at 2.1%, driven mainly by robust non-residential investment and resilient consumption. While consumers have remained resilient, but we are seeing household excess savings being drawn down and credit card debt levels rising, which will eventually impact economic growth.

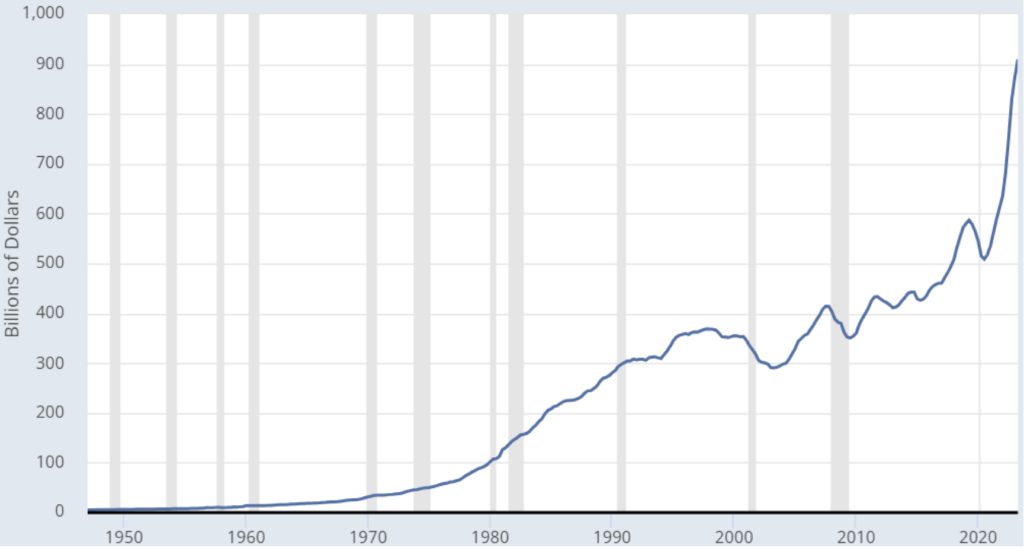

In August, Fitch Ratings downgraded the US Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘AA+’ from ‘AAA’. According to Fitch, the rating downgrade of the US reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden. In Fitch’s view, there has been a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters, notwithstanding the June bipartisan agreement to suspend the debt limit until January 2025. The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management. Even after the downgrade, the US once again averted a government shutdown after a bill ensuring funding until November 17th was signed into law by President Joe Biden minutes before October 1st deadline. The line graph below shows the amount of government interest payments dating back to 1947. While the US federal debt has risen faster in recent years, higher interest rates pose the added challenge of sharply higher annual interest payments. However, when rates begin to ease, this will relieve some pressure, but mounting government debt remains a broader-term risk.

US Government annualised interest payments as of Q2 2023

Europe

In Europe, both growth and inflation has been slowing but unemployment remains low. The Euro Area GDP expanded 0.1% on quarter in the three months to June 2023. It follows a 0.1% growth in the previous quarter. In contrast, the German economy stagnated in the second quarter of 2023 compared to the previous three months, following two consecutive periods of contraction. The inflation rate in the Euro Area declined to 4.3% year-on-year in September 2023, reaching its lowest level since October 2021. On the policy front, the ECB raised interest rates for the 10th consecutive time on September 14th to 4.5% and signaled that it is likely done tightening policy, as inflation has started to decline but is still expected to remain too high for too long. According to the September ECB staff macroeconomic projections for the Euro Area, average inflation is forecasted to be at 5.6% in 2023 and 3.2% in 2024, both higher than previous estimates, primarily due to an elevated path for energy prices. In contrast, the 2025 rate projection has been cut to 2.1%. The central bank has also significantly reduced its GDP growth projections, now anticipating the economy to expand by 0.7% in 2023, 1% in 2024, and 1.5% in 2025.

China

China’s economy showed some signs of improvement in August, particularly in industrial production and retail sales. The Chinese economy grew by 0.8% in the second quarter of 2023, but slowing sharply from the 2.2% expansion observed in the previous quarter. While this marks the fourth consecutive quarter of economic expansion, it also highlights that the recovery in China is losing momentum and remains uneven due to the ongoing property downturn, the possibility of disinflation, record high unemployment rates among young adults, and declining exports. Chinese property developers continue their struggle to stay afloat as both financing and sales dry up. Weakness in property market is perhaps the most challenging growth headwind for China. Over the past months, a number of new stimulus measures have been announced with the aim of stabilising the housing market. Meanwhile, youth unemployment rate in China increased to a fresh record high of 21.30% in June 2023, meaning more than one in five of those between 16 to 24 years old are unemployed.

As the rest of the economies struggle with high inflation, in China the consumer prices rose by 0.1% yoy in August 2023 after the first drop in over 2 years of 0.3% a month earlier. The People’s Bank of China (PBoC) maintained lending rates in September, as policymakers assessed the impact of previous easing measures, including an interest rate cut in August and a recent reduction in the reserve requirement ratio for banks. The one-year loan prime rate (LPR), which is the medium-term lending facility used for corporate and household loans, was kept unchanged at a record low of 3.45%; and the five-year rate, a reference for mortgages, was held at 4.2% for the third straight month.

Others

The Bank of Japan (BoJ) maintained its key short-term interest rate at -0.1% and that of 10-year bond yields at around 0% in its September meeting by unanimous vote. The central bank also left unchanged an allowance band of 50bps set on either side of the yield target, as well as a cap of 1% adopted in July. The annual inflation rate in Japan edged down to 3.2% in August 2023 from 3.3% in the prior month. Meanwhile, the Bank of Russia raised its key interest rate by 100bps to 13% in its September 2023 meeting, furthering the extraordinary 350bps rate hike from the middle of August. The central bank noted that inflationary pressures in the Russian economy remain high, as growth in domestic demand outpaces low capacity due to the war-driven labour force crisis, in addition to a weakening ruble.

To summaries, despite the resilience witnessed in economic activity year to date, recession risks remain elevated. Interest rates appear to be peaking in most developed economies, with some expected to possibly raise further, but most of the rate rises are over and done with – now it’s the case of ‘wait-and-see’ to understand the effect of monetary tightening on key economic indicators including inflation, unemployment, growth and others. In the UK, the economy continues to grow a little but inflation is easing and unemployment rising, which is the desired effect policy makers like to see. Likewise in Europe, growth is meagre and inflation is coming down, but unemployment remains somewhat sticky. Nevertheless, we are seeing signs of slowdown in Euro Area as a whole, but there may be disparities within Euro Area economies. Meanwhile, the US economy continues to grow and labour market remains tight, but we are seeing household excess savings being drawn down and credit card debt levels rising, which will eventually impact economic growth. The US government debt poses a risk to the US economy and possibly the USD dollar, particularly in the medium to long term. There is more talk of a soft landing for the US economy where recession is avoided. This is possible but we view recession is likely. Given the macroeconomic backdrop including the possibility of ‘higher rates for longer’; the evolving political uncertainties witnessed by escalation in conflicts around the world; and the dispersion in valuations within and across the global markets, we remain cautious and diligent when picking investments and continue to adjust our broader asset allocation where necessary and appropriate as we navigate through this challenging period.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

Data as of 30 September 2023. This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.