In Q2 2026, global economies and financial markets were shaped by sticky inflation, uneven economic growth, and heightened geopolitical uncertainty. Inflation continued to pose a challenge across several advanced economies amid the surge in energy prices in later part of Q1 and Q2 resulting from Middle East tensions. This complicated the disinflation process and reinforced a cautious stance among major central banks. Economic activity remained resilient in the United States but softened across Europe, the UK, and China, reflecting weaker industrial production and subdued consumer demand. Financial markets experienced elevated volatility as investors repeatedly reassessed the path of interest rates amid shifting macroeconomic data. Commodity prices, particularly oil and gold, softened supported by progress on geopolitical fronts, while equity market performance varied across regions and sectors. Overall, Q2 2026 highlighted the delicate balance between uncertain macroeconomic fundamentals and persistent geopolitical and inflation-related headwinds.

Macroeconomic picture

The key macroeconomic indicators across major economies reflected a mix of resilience and fragility amid evolving policy and geopolitical dynamics. In the United States, growth remained relatively robust, supported by a healthy labour market and steady consumer spending, although core inflation remained elevated amid higher oil prices, making the Federal Reserve’s job difficult. The Eurozone experienced subdued growth, with weak industrial output and cautious consumer demand, even as headline inflation edged lower, although still higher than European Central Bank’s 2% targe. The United Kingdom saw accelerated economic activity with higher-than-expected growth while inflation remained above target, constraining the Bank of England’s flexibility to cut rates. In Japan, inflation softened although policy rate remained high at 1%, while economic expansion remained moderate. Meanwhile, China showed strong economic growth supported by Govt stimulus measures offset by weak property markets and subdued consumer confidence. Inflation and policy rates remained steady. Overall, Q2 highlighted divergent macroeconomic paths, with policymakers balancing growth support against lingering macro pressures.

The following table lists the latest key macroeconomic indicators across major economies (as of 03 July 2026).

Financial markets performance

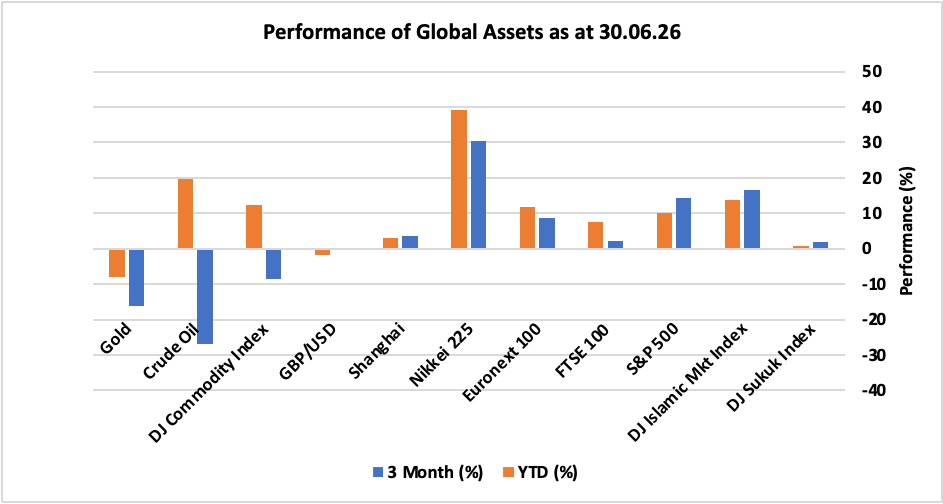

Looking at the performance, global risk assets delivered strong positive returns driven by resilient corporate earnings and positive developments in AI theme, however, commodities and gold performed poorly in the quarter amid geopolitical fears softened resulting from Middle East peace talks. US equity markets recorded significant gains as S&P 500 surged by 14.4% whereas DJ Islamic Markets Index booked 16.70% returns during the month. While in Europe, UK FTSE 100 and EU Euronext 100 delivered positive 2.15% and 8.7%, respectively. In Asia, Japan’s Nikkei 225 surged by 30.4% while China’s Shanghai index rose 3.7%. DJ Sukuk Index delivered positive 1.9% amid softening yields whereas US dollar strengthened, which appreciated 0.39% against UK pound. In commodities, DJ Commodity index tumbled by 8.5% driven by nearly 27% drop in Crude oil and 16.3% decline in gold prices amid easing geopolitical risks in the Middle East.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q2 2026, as well as their progress year-to-date.

Performance of global assets – Q2 2026

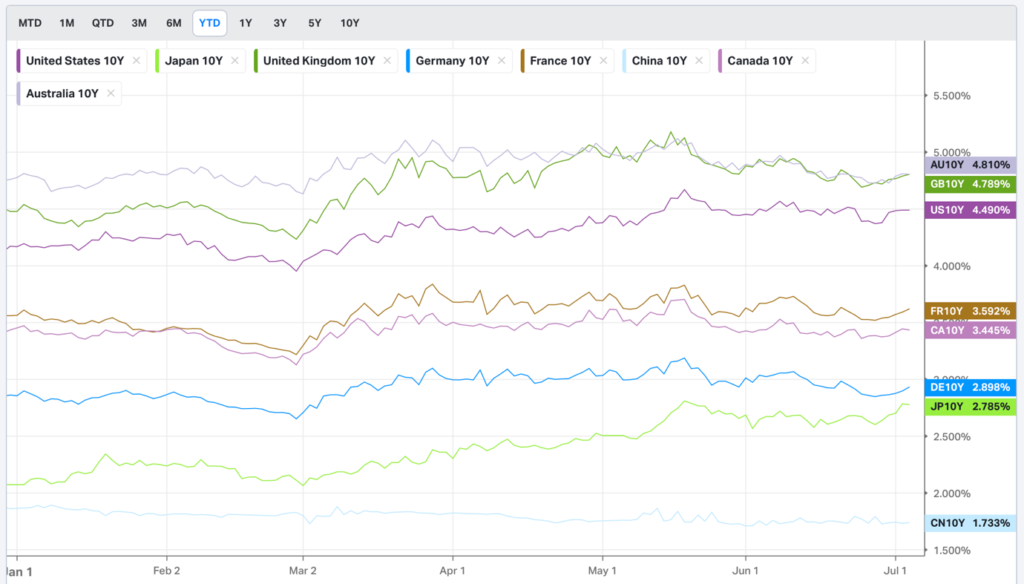

Treasury yields

In the second quarter of 2026, 10‑year Treasury yields from major economies experienced a softening trend, reflecting easing pressures on geopolitical fronts although macro factors remained largely uncertain. The quarter was characterised by a slight downward movement in yields as investors responded to a combination of geopolitical tensions, particularly relating to ongoing conflicts in Eastern Europe and the Middle East, and a cautious stance from central banks worldwide, who largely refrained from implementing further rate cuts. Central banks, mindful of the mixed economic data and the outlook for inflation and growth, opted for a wait-and-see approach, signalling their intent to monitor developments before adjusting monetary policy further. Overall, the first quarter saw Treasury markets navigating a complex mix of macroeconomic and geopolitical headwinds, with policy uncertainty and risk aversion driving yield dynamics.

10-Year Treasury Yields

Source: Koyfin

Geopolitical situation

During Q2 2026, geopolitical developments were dominated by the continuing Russia–Ukraine war and the escalation of the U.S.–Iran conflict, both of which significantly influenced global markets. The Russia–Ukraine conflict remained intense, with sustained missile and drone attacks, continued fighting along the eastern front, and further Western military assistance to Ukraine, while diplomatic efforts made limited progress toward a ceasefire. In the Middle East, despite continued hostilities, Q2 2026 also saw renewed diplomatic efforts to de-escalate tensions between the United States and Iran. Through mediation by regional partners, including Gulf states, both sides engaged in indirect and direct negotiations aimed at securing a ceasefire, reducing attacks on strategic energy infrastructure, and ensuring the safe passage of commercial shipping through the Strait of Hormuz. Although a comprehensive peace agreement remained elusive, these diplomatic initiatives helped ease immediate fears of a broader regional conflict and provided intermittent support to global financial markets. Overall, persistent geopolitical uncertainty remained a key driver of market volatility throughout the second quarter of 2026.

Key News & Events in Q2 2026

UK

- The annual inflation rate in the UK stood at 2.8% in May 2026, unchanged from the previous month and below market expectations of 3.0%. The reading remained at its lowest level since March last year.

- The Bank of England voted 7-2 to keep Bank Rate unchanged at 3.75% in June 2026, remained at this level in Q2, as policymakers weighed easing inflation against continued uncertainty from volatile global energy markets linked to Middle East tensions. Two members of the Monetary Policy Committee preferred a 0.25 percentage point hike to 4%.

- The UK economy expanded by 0.6% quarter-on-quarter in Q1 2026, confirming preliminary estimates and accelerating from a revised 0.1% growth in Q4. This marked the strongest quarterly expansion since Q1 2025.

- The UK unemployment rate fell to 4.9% in the three months to April 2026, defying expectations that it would remain at 5.0%.

US

- The annual inflation rate in the US rose to 4.2% in May 2026, marking its highest level since April 2023, from 3.8% in April and in line with market expectations. This represents the third consecutive monthly acceleration in headline inflation, with energy costs jumping 23.5% due to the energy shock triggered by the conflict with Iran.

- Interest rate remained at 3.75% in Q2. Inflation proved sticky but the US central bank remains committed to restoring inflation to its 2% target, Federal Reserve Chair Kevin Warsh said at the ECB’s annual Forum on Central Banking in Sintra, Portugal.

- The US economy expanded an annualized 2.1% in Q1 2026, revised up from 1.6% in the second estimate, and above 0.5% in Q4 2025.

- The US unemployment rate dropped to 4.2% in June 2026, down from 4.3% in both May and April, and below expectations, as many people left the workforce.

Europe

- Eurozone consumer price inflation dropped to 2.8% in June 2026, down from 3.2% in May and below market expectations of 3.0%, according to preliminary data. This marks the lowest rate since February, before the Iran war disrupted energy supplies and pushed oil prices higher, though it remains above the European Central Bank’s 2.0% target.

- The European Central Bank raised interest rates by 25 basis points to 2.4% from 2.15% at its June 2026 meeting, the first increase since 2023, as policymakers emphasized their commitment to anchoring inflation at the 2% medium-term target.

- The Eurozone economy shrank by 0.2% in the first quarter of 2026, revised down from an initially reported 0.1% growth, according to final EUROSTAT data. This marks the first contraction since Q4 2022 and the sharpest decline since mid-2020, driven by a significant downward revision to Ireland’s GDP, which plummeted 12.1% in Q1.

- The Euro Area seasonally adjusted unemployment rate came in at 6.2% in May 2026, tying the record lows from late 2024 and unchanged from the prior month. Analysts had estimated it at 6.3%.

China

- China’s annual inflation held steady at 1.2% in May 2026, unchanged from the previous month but slightly below market expectations of 1.3%.

- The People’s Bank of China kept its key lending rates at record lows at 3%-3.5% for a 13th straight month in June 2026, as widely expected. The move reflected caution over the fallout from the conflict in the Middle East, even as growth momentum has recently sputtered amid mixed economic data.

- China’s GDP grew 1.3% qoq in Q1 2026, matching market expectations and following a 1.2% increase in Q4. The latest result marked the strongest quarterly expansion since Q4 of 2024, supported by continued policy backing from Beijing.

China’s surveyed urban unemployment rate edged lower to 5.1% in May 2026, compared with both market expectations and the previous month’s 5.2%. It marked the lowest reading since December 2025.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.