In Q1 2026, global economies and financial markets were shaped by a complex mix of sticky inflation, uneven growth momentum, heightened policy uncertainty, and geopolitical risks. While inflation remained a key theme in some major economies, it remained sticky in core components, leading central banks to adopt a cautious and data-dependent approach to interest rate decisions. Growth indicators showed divergence, with the US remaining relatively resilient, while Europe and the UK experienced softer economic activity and China delivered on promised numbers despite ongoing structural challenges. Bond markets were volatile as expectations for rate cuts were repeatedly repriced, while equity markets saw increased dispersion between defensive sectors and growth-oriented technology stocks amid rising energy prices as geopolitical situation became more intensified. Currency markets reflected these dynamics, with the US dollar strengthening during periods of risk aversion. Overall, macroeconomic conditions in Q1 reinforced a cautious investment environment amid lingering inflation risks and fragile global growth.

Macroeconomic picture

The key macroeconomic indicators across major economies reflected a mix of resilience and fragility amid evolving policy and geopolitical dynamics. In the United States, growth remained relatively robust, supported by a strong labour market and steady consumer spending, although core inflation proved sticky, making the Federal Reserve’s job difficult. The Eurozone experienced subdued growth, with weak industrial output and cautious consumer demand, even as headline inflation edged closer to target, allowing the European Central Bank to signal a gradual shift toward policy easing. The United Kingdom saw modest economic activity with soft retail and housing data, while inflation, though declining, remained above target, constraining the Bank of England’s flexibility. In Japan, inflation stayed slightly above the Bank of Japan’s target, supported by wage growth, while economic expansion remained moderate, reinforcing a gradual policy normalization stance. Meanwhile, China showed uneven recovery trends, with improved manufacturing activity and targeted stimulus measures offset by weak property markets and subdued consumer confidence. Overall, Q1 highlighted divergent macroeconomic paths, with policymakers balancing growth support against lingering inflationary pressures.

The following table lists the latest key macroeconomic indicators across major economies (as of 07 April 2026).

Financial markets performance

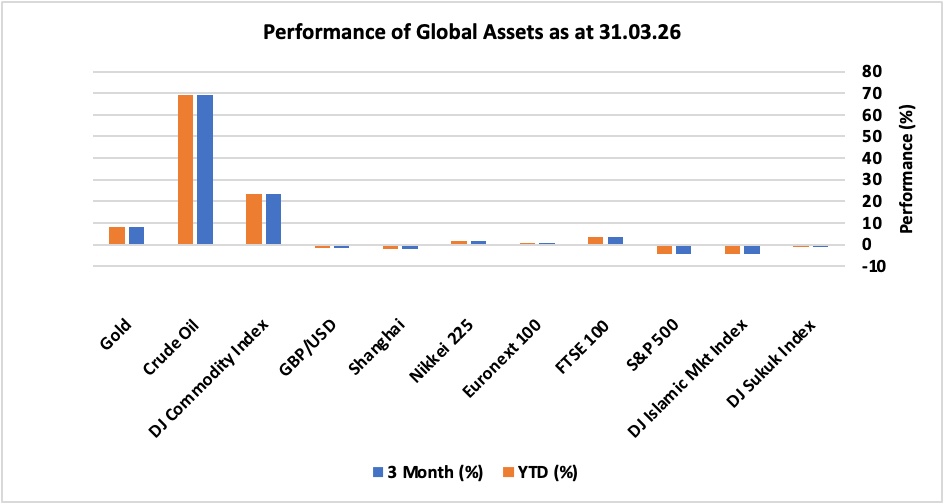

Looking at the performance, most of the major global financial assets experienced extreme volatility and negative momentum (except commodities) in Q1 amid geopolitical fears resulting from War in Middle East, despite resilient corporate earnings and positive developments in AI theme. US equity markets recorded significant losses as S&P 500 declined by 4.33% whereas DJ Islamic Markets Index booked negative 4.25% returns during the month. While in Europe, UK FTSE 100 and EU Euronext 100 delivered positive 3.42% and 0.77%, respectively, largely driven by higher energy sectors weight in the indices. In Asia, Japan’s Nikkei 225 rose by 1.44% while China’s Shanghai index tumbled 1.94%. DJ Sukuk Index ended the month down 1.14% amid rising yields whereas US dollar strengthened, which appreciated 1.71% against UK pound. In commodities, DJ Commodity index climbed by 23.5% driven by nearly 69% surge in Crude oil prices amid extreme geopolitical risks.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q1 2026, as well as their progress year-to-date.

Performance of global assets – Q1 2026

Treasury Yields

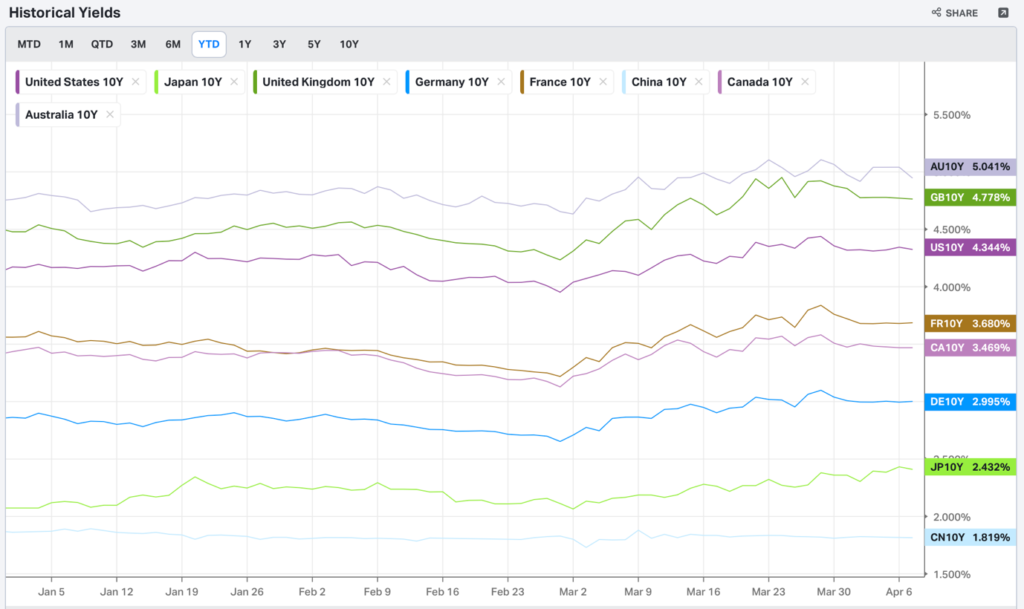

In the first quarter of 2026, 10‑year Treasury yields from major economies experienced notable volatility, reflecting heightened uncertainty in the global financial landscape. The quarter was characterised by a slight upward movement in yields as investors responded to a combination of rising geopolitical tensions, particularly relating to ongoing conflicts in Eastern Europe and the Middle East, and a cautious stance from central banks worldwide, who largely refrained from implementing further rate cuts.

Central banks, mindful of the softening economic data and the ambiguous outlook for inflation and growth, opted for a wait-and-see approach, signalling their intent to monitor developments before adjusting monetary policy further. This hesitancy was compounded by persistent concerns over increasing government debt burdens, unresolved trade frictions, and the broader geopolitical situation, all of which contributed to elevated risk perceptions among market participants.

As a result, demand for safe-haven assets remained robust, but the perceived risks surrounding long-term fiscal and geopolitical stability kept long-dated yields from easing significantly. The interplay of these factors created an environment in which investors required higher compensation for holding longer-term government bonds, thereby sustaining elevated yields despite otherwise subdued economic momentum. Overall, the first quarter saw Treasury markets navigating a complex mix of macroeconomic and geopolitical headwinds, with policy uncertainty and risk aversion driving yield dynamics.

10-Year Treasury Yields

Source: Koyfin

Geopolitical situation

In Q1 2026, geopolitical developments were dominated by a major escalation in the Middle East alongside the Russia–Ukraine war. The most significant event was the outbreak of the U.S.–Israel war with Iran on 28 February 2026, when coordinated strikes targeted Iranian military and nuclear infrastructure, triggering widespread retaliation through missile and drone attacks across Israel and U.S. bases in the Gulf. The conflict rapidly expanded regionally, disrupting energy routes such as the Strait of Hormuz and intensifying global security concerns. At the same time, the Russia–Ukraine conflict remained active, with continued military engagements and renewed diplomatic efforts, including trilateral peace talks in Abu Dhabi during January–February. Notably, geopolitical linkages deepened as Iran’s ties with Russia and Ukraine’s involvement in countering Iranian drones highlighted the growing interconnectedness of global conflicts. Overall, Q1 2026 was marked by escalating tensions, overlapping conflicts, and rising risks to global stability and economic conditions.

Key News & Events in Q1 2026

UK

- The annual inflation rate in the UK steadied at 3% in February 2026, maintaining the same level as in January and aligning with market expectations. Price pressures remained broadly stable, with food, energy, and core goods components showing limited movement. This stability suggests that recent monetary policy actions and external factors such as moderating global commodity prices may have helped anchor inflation expectations, providing some reassurance to households and businesses facing cost-of-living challenges.

- The Bank of England refrained from cutting rates in the first quarter of 2026 and, in its latest policy meeting in March, unanimously decided to keep the Bank Rate at 3.75%. This cautious stance reflected heightened uncertainty stemming from the conflict in the Middle East, which triggered a sharp spike in global energy and commodity prices. As a result, households experienced increases in fuel and utility costs, while businesses faced higher expenses for inputs and transportation. The central bank emphasised the need to monitor international developments closely and maintain flexibility in its approach to future policy adjustments.

- The British economy expanded by 0.1% on a quarterly basis during the last three months of 2025, matching the growth rate recorded in the previous quarter and confirming the preliminary estimate. This modest expansion was supported by resilient consumer spending and steady government investment, although business sentiment remained subdued due to ongoing global uncertainties. The data underscores the UK’s fragile recovery, with economic momentum limited by external risks, elevated inflation, and concerns about future demand.

- The UK unemployment rate held steady at 5.2% in the three months to January 2026, coming in just below analysts’ expectations of 5.3%. However, this figure still represents the highest jobless rate seen since the three months to February 2021, indicating persistent challenges in the labour market. Employers remained cautious in hiring amid economic uncertainty and rising costs, while policymakers watched employment trends closely for signs of sustained weakness that could impact consumer confidence and broader recovery prospects.

US

- The annual inflation rate in the US held steady at 2.4% in February 2026, unchanged from January, in line with expectations and remaining at its lowest level since May 2025. This stability in consumer prices reflects the impact of recent monetary policy actions, as well as moderating energy and food costs, which have helped anchor inflation expectations. For households and businesses, this provides some relief amid ongoing concerns about living costs, although inflation remains above the Federal Reserve’s target, keeping policymakers vigilant for any signs of renewed upward pressure.

- The Fed left the federal funds rate steady at the 3.5%–3.75% target range for a second consecutive meeting in March 2026, in line with expectations. Policymakers noted that economic activity has been expanding at a solid pace, yet job gains have remained low and inflation continues to be somewhat elevated. This cautious approach reflects uncertainty around global developments, particularly the escalation of conflict in the Middle East, which has contributed to volatile commodity prices and increased risks to the economic outlook. The Federal Reserve emphasised the importance of monitoring incoming data and maintaining flexibility in its policy stance.

- The US economy expanded at an annualised rate of 0.7% in Q4 2025, marking the weakest performance since a contraction in the first quarter of 2025 and falling well below the 1.4% growth seen in the advance estimate. This slowdown was largely attributed to subdued consumer spending and softer business investment, as external uncertainties and higher borrowing costs weighed on economic momentum. Despite this, pockets of resilience remain, with government spending and certain sectors continuing to support overall growth, even as concerns about future demand persist.

- The US unemployment rate fell to 4.3% in March 2026 from 4.4% in February, coming in below market expectations of 4.4%. This slight improvement suggests ongoing resilience in the labour market, although job gains have been modest and wage growth remains moderate.

Europe

- Euro area annual inflation climbed to 2.5% in March 2026, up from 1.9% in February and slightly below market expectations of 2.6%, according to a preliminary estimate. This acceleration was largely driven by rising energy and food prices, as well as persistent supply chain challenges across the region. The increase signals that inflationary pressures remain strong, prompting analysts to closely monitor the potential impact on consumer spending and business confidence in the coming months.

- The European Central Bank kept interest rates unchanged at its March 2026 meeting, no change since June 2025, reaffirming its commitment to stabilising inflation at 2% in the medium term. The ECB’s decision reflects ongoing caution amid persistent inflation and moderate economic growth, with policymakers emphasising the need for stability and signalling a readiness to adjust policy if inflation diverges from its target. Market participants are now looking to future meetings for any hints on policy shifts, especially if inflation remains elevated or economic conditions deteriorate.

- The Euro Area economy grew by 0.2% in Q4 2025, below earlier estimates of 0.3% and down from 0.3% in Q3, highlighting modest momentum despite lower interest rates, and resilience amid headwinds from US trade tariffs on EU imports. The subdued growth rate points to ongoing challenges for businesses, particularly in manufacturing and export sectors, as global trade tensions and supply disruptions continue to weigh on activity. Nevertheless, the Euro Area has managed to avoid recession, demonstrating underlying strength in domestic demand and services.

- The unemployment rate in the Euro Area increased to 6.20 percent in February from 6.10 percent in January of 2026. This uptick suggests that labour market conditions are beginning to soften, potentially reflecting delayed effects from slow economic growth and ongoing external challenges. The rise in unemployment is most pronounced in countries with significant exposure to global trade, underscoring the importance of targeted policy interventions to support job creation and retraining efforts.

China

- China’s annual inflation surged to 1.3% in February 2026, a significant rise from the 0.2% recorded in January. This marked the highest level since January 2023 and exceeded market forecasts of 0.8%. The increase was primarily driven by higher food and energy prices, alongside a rebound in consumer demand. This uptick in inflation signals a shift in price dynamics after a prolonged period of subdued inflation, and analysts are closely watching for its effects on household spending and broader economic sentiment.

- The People’s Bank of China (PBoC) opted to maintain its key lending rates at historic lows for the tenth consecutive month in March 2026, in line with market expectations. This decision reflects the central bank’s commitment to supporting economic stability rather than implementing aggressive monetary stimulus. By keeping rates steady, the PBoC aims to encourage borrowing and investment without fuelling excessive inflation, especially as global conditions remain uncertain.

- China’s gross domestic product (GDP) expanded by 1.2% quarter-on-quarter in Q4 2025, surpassing market expectations of a 1.0% increase and up from the 1.1% growth recorded in Q3. This represents the fastest pace of expansion in three quarters, underpinned by resilient domestic demand and continued government support for key industries. Despite ongoing challenges in the property sector and weak external demand, the latest figures indicate that the Chinese economy retains considerable momentum heading into 2026.

China’s surveyed urban unemployment rate edged up to 5.3% in February 2026, increasing from 5.2% in the previous month and exceeding market projections of 5.1%. The rise in unemployment suggests that job creation has not kept pace with labour market entrants, particularly in sectors impacted by global economic uncertainty and domestic restructuring efforts. Policymakers are likely to prioritise measures to support employment and retraining, aiming to bolster consumer confidence and sustain economic growth.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.