Economic and Market Overview

Q1 2024 proved to be another good quarter for financial markets as investors continued to be somewhat optimistic. The prevailing investor confidence mainly relies on three key factors: resilient economies and corporate profits, optimism on the AI hype, and expectations that interest rates will start taking downward trajectory in the near future. Inflation rates are moderating, and rates are peaked, both factors indicate central bankers will pivot in coming months to bring rates down. However, resilient economic growth and sticky inflation could lead to the possibility of interest rates and bond yields staying higher for longer than the markets are pricing in, which is a tail risk for the financial markets.

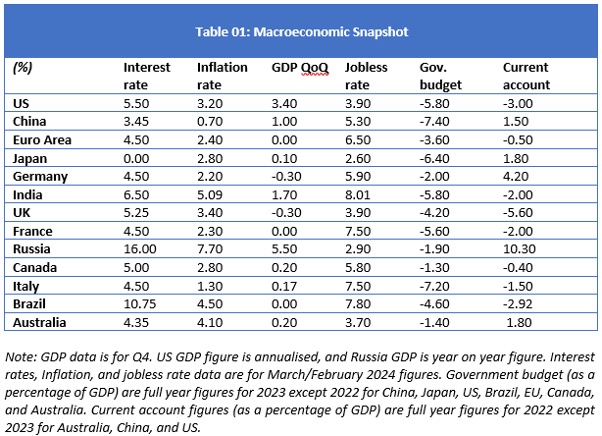

Despite the high-speed increase in interest rates, economies showed resilience and unemployment rates remained moderate. Amongst key economies, the recent inflation figures show a decline in the US, UK, Euro-Area, and Brazil, whereas inflation remained steady in Canada but rose in Russia and a reversal is seen in China that was experiencing a deflationary cycle. During the first quarter, all key central banks including the Federal Reserve, the Bank of England and ECB kept interest rates steady. Moreover, the Federal Reserve signaled that there will be at least three rate cuts in 2024, although the probability to start cutting rates pushed back to June from March 2024. On the GDP growth front, recent figures show a mixed picture where we can see a growth in the US, but negative growth in the Euro-Area and UK (which is now in technical recession). Unemployment rate increased in the US and China but remained steady in the Euro Area. Moreover, Chinese economy showed some signs of improvement driven by several stimulus initiatives taken by the government. Although the Luner year shopping season helped Chinese economy to get out of deflationary cycle, the overall outlook for its economy remained uncertain amid weak overseas demand and a property downturn.

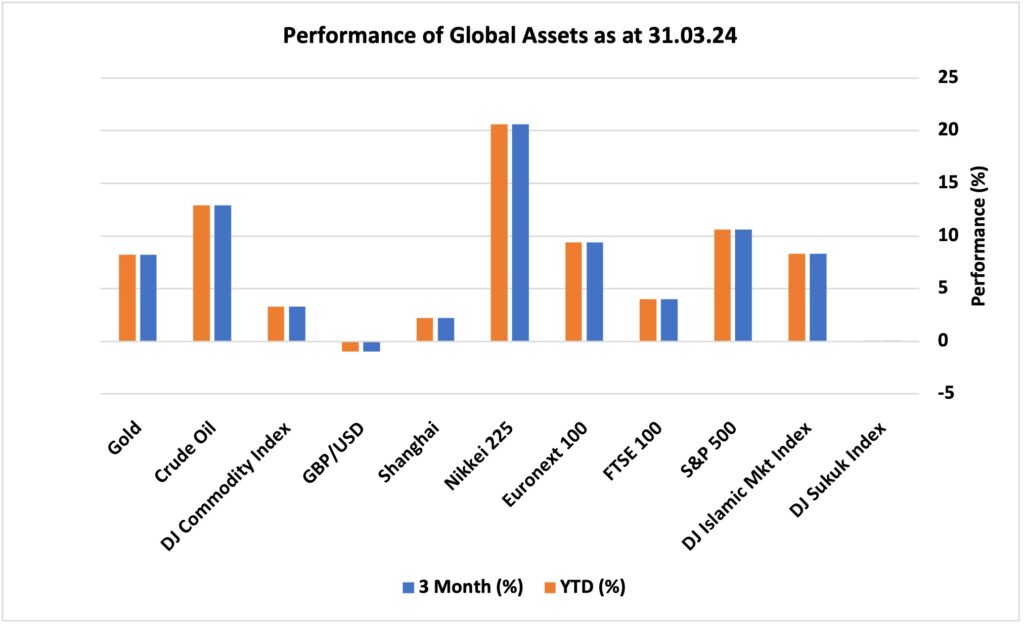

Looking at the performance of major asset classes over the course of Q1 2024, equity markets continued strongly on the positive momentum set by the last quarter of 2023 amid falling inflation levels in all major economies and the signals from central banks that interest rates will start falling sometime in 2024. Japan’s Nikkei 225 surprised international investors’ with another stellar quarter that surged another 20% in Q1 of 2024 at the backdrop of corporate reforms and world’s greatest investor Warren Buffet’s increased confidence on Japanese’ companies. S&P 500 index was the second best performing equity market with 10.6% quarterly return followed by Europe’s Euronext 100 and DJ Islamic markets index with 9.4% and 8.3%, respectively. The UK FTSE 100 returned only 4%, impacted by fears of recession as UK economy entered technical recession in the last quarter of 2023. China’s Shanghai Index increased only 2.2% after a negative performance in the previous quarter amid slow growth and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing. DJ sukuk index closed the quarter flat as yields increased again after falling in the previous quarter. Commodities’ markets also rewarded investors with good returns where oil rose by 12.9%, gold surged by 8.2%, and DJ Commodity Index increased by 3.3% in the first quarter of 2024 amid delays in interest rate cutting cycle. Lastly, UK pound fell against US dollar by roughly 1% in the first quarter of 2024.

Performance of global assets Q1 2024

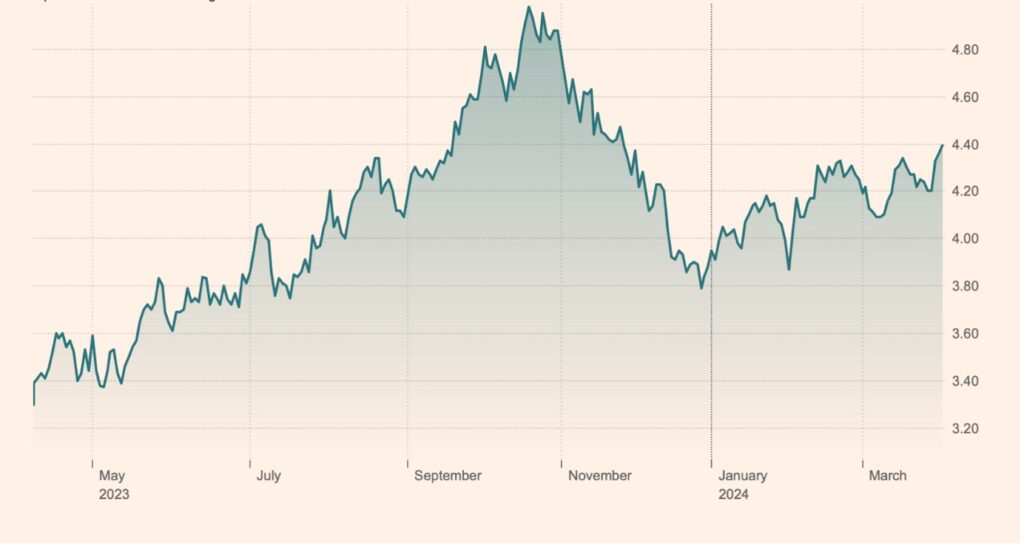

In Q1 of 2024, yields started rising again, and at the end of the quarter, they are back to around 4.4% level that was last seen in November 2023. This reversal is mainly driven by delay in rate cutting cycle. The Federal Reserve signaled that there will be at least three rate cuts in 2024, although the probability to start cutting rates pushed back to June from March 2024.

10-Year Treasury Yields

Key News & Events in Q1 2024

UK

• The Bank of England maintained the Bank Rate at 5.25% during its March meeting, its highest level since 2008, as policymakers awaited clearer signals indicating that the country’s persistent inflationary pressures had subsided. The Monetary Policy Committee voted by an 8-1 margin in favour of keeping rates unchanged, with one member advocating for a 25-basis point decrease. The central bank has not increased rates after August 2023.

• The most recent published inflation figure for February shows the inflation rate dropped to 3.4% year-on-year in February 2024, down from 4% recorded in both January and December and falling below the market expectation of 3.5%. It was the lowest rate since September 2021.

• The UK’s economy shrank by 0.3% in the final quarter of 2023, entering a technical recession for the first time since the aftermath of the COVID-19 outbreak in the initial half of 2020, as high inflation, record borrowing costs, and weak external demand weighed on demand and activity.

• The unemployment rate edged up to 3.9% from November 2023 to January 2024, largely unchanged from the previous quarter but slightly above the market consensus of 3.8%.

• Second half of 2023 proved to be difficult for UK housing market where average house price dropped below £280,000. However, in the fourth quarter of 2023, house prices started recovering some of their lost values mainly driven by the hopes that interest rates have peaked, and easy monetary policy era is coming soon. The first quarter of 2024 continued the uptrend with average house price topping £292,000.

US

• The US Federal Reserve (Fed) looks to soften its stance towards monetary policy based on recent macroeconomic data. The Federal Reserve left the fed funds rate steady at a 23-year high of 5.25%-5.5% for a fifth consecutive meeting in March 2024, in line with market expectations. Policymakers still plan to cut interest rates three times this year, similar to the quarterly forecasts in December.

• Inflationary pressures are softening but with some surprises where annual inflation rate in the US unexpectedly edged up to 3.2% in February 2024, compared to 3.1% in January and above forecasts of 3.1%.

• The US economy expanded an annualized 3.4% in Q4 2023, slightly above the 3.2% previously reported, supported by consumer spending and non-residential business investments, according to the third estimate from the BEA.

• It looks like the rate tightening cycle is finally having its weigh on employment where the unemployment rate in the United States rose by 0.2% to 3.9% in February 2024, touching the highest level since January 2022 and surpassing market expectations of 3.7%. The number of unemployed people increased by 334,000 to 6.5 million.

Europe

• The Euro Area economy stagnated in the fourth quarter of 2023, following a 0.1% contraction in the previous three-month period, as persistently high inflation, record borrowing costs, and weak external demand continued to exert downward pressure on growth.

• Meanwhile, the ECB has projected inflation to average 2.3% in 2024 (compared to 2.7% in December projections), 2% in 2025 (compared to 2.1%), and 1.9% in 2026.

• The European Central Bank maintained its interest rates at historically high levels during its March meeting, as policymakers balanced concerns over a looming recession with persistently elevated underlying inflationary pressures. The main refinancing operations rate remained at a 22-year pinnacle of 4.5%, with the deposit facility rate unchanged at an unprecedented 4%.

• The unemployment rate in the Euro Area stood at a record low of 6.5% in February 2024, matching January’s revised figure. The number of unemployed individuals increased by 17 thousand from the prior month to 11.102 million.

China

• The Chinese economy grew by a seasonally adjusted 1% in Q4 of 2023, matching market expectations but moderating from an upwardly revised 1.5% increase in Q3. This was the sixth consecutive period of quarterly expansion, with weakness in the property sector continuing to drag on the broader economic recovery.

• The People’s Bank of China kept benchmark lending rates unchanged at the March fixing, as widely expected. The one-year loan prime rate (LPR), the benchmark for most corporate and household loans, was retained at 3.45%. Meanwhile, the five-year rate, a reference for property mortgages, was maintained at 3.95% following the biggest-ever reduction of 25bps in February. Both rates are at record lows, as the central bank seeks to spur an economic turnaround in the face of headwinds from the property sector and a near-record low in consumer confidence.

• China’s consumer prices rose by 0.7% yoy in February 2024, above market forecasts of 0.3% and a turnaround from the sharpest drop in over 14 years of 0.8% in January. The latest result was the first consumer inflation since last August, hitting its highest level in 11 months due to robust spending during the Lunar New Year holiday.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.