Economic and Market Overview

Q4 of 2023 has been good for investors as markets celebrated an upright run after difficult months in summer. Falling inflation numbers in all the major economies compel the policy makers to change their hawkish tone. Now it looks like the rates have peaked and they are possibly expected to start coming down in coming months. Despite the high-speed increase in interest rates, economies showed resilience and unemployment rate remained moderate. Amongst key economies, the recent inflation figures show a decline in the US, UK, Euro-Area, and Brazil, whereas inflation remained steady in Canada but rose in Russia. During the quarter, all key central banks including the Federal Reserve, the Bank of England and ECB kept interest rates unchanged. Moreover, the Federal Reserve signaled that there will be at least three rat cuts in 2024, although markets are pricing more than that. On the GDP growth front, recent figures show a mixed picture where we can see a growth in the US, but negative growth in the UK and Euro-Area. Unemployment rate marginally fell in the US and Euro Area but remained steady in the UK and China. Meanwhile, China’s economy showed some signs of improvement driven by number of stimulus initiatives taken by the government. However, those measures failed to get the economy out of deflationary conditions. The overall outlook for the Chinese economy remains uncertain, amid weak overseas demand and a property downturn. The key events pricing in are growth concerns, mixed economic data, and geopolitical tensions, which are weighing on investors’ enthusiasm for equities in the region.

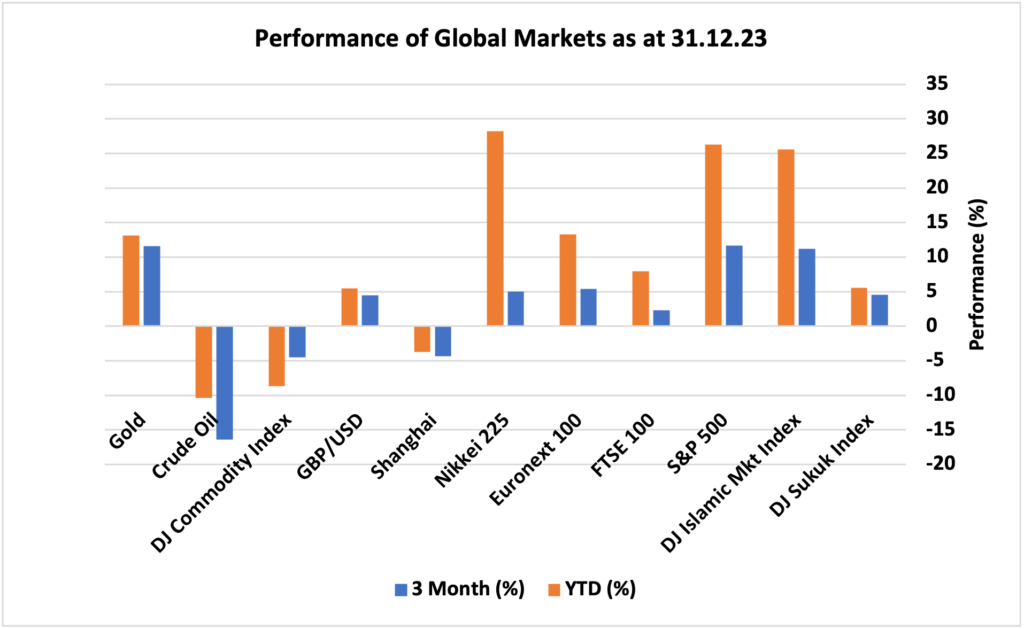

Looking at the performance of major asset classes over the course of Q4 2023, equity markets rebounded strongly after a sluggish summer amid falling inflation levels in all major economies and the signals from central banks that interest rates will start falling in the first half of next year. S&P 500 index was the leader with 11.7% quarterly return followed by DJ Islamic markets index with 11.2% and 2.81%. Europe’s Euronext 100 and Japan’s Nikkei 225 rose by 5.44% and 5.04%, respectively. UK FTSE 100 returned only 2.31% mainly because of its high exposure to energy (which dropped in value significantly in the quarter) and international exposure that had a weigh on its performance due to currency exposure (UK Pound appreciated against US Dollar in the quarter by 4.5%). China’s Shanghai Index fell 4.36% as there are still concerns of deflation and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing. On an annualized basis, equity markets booked 2023 as one of the best performing years in the equity markets recent history. Gold returned 11.6% amid falling US dollar against pound and concerns over slowing global economy. DJ sukuk index surged 4.54% in the fourth quarter amid falling yields as market consensus is shifting towards interest rates cut in the first half of 2024. Commodities remained under pressure where crude oil fell over 16% amid concerns over slowing global economy after historic speed of rates hike and struggling world’s second largest economy. Overall, DJ Commodity Index dropped by 4.49% in last quarter of 2023.

Portfolio Commentary

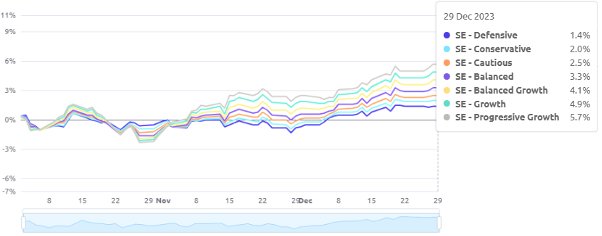

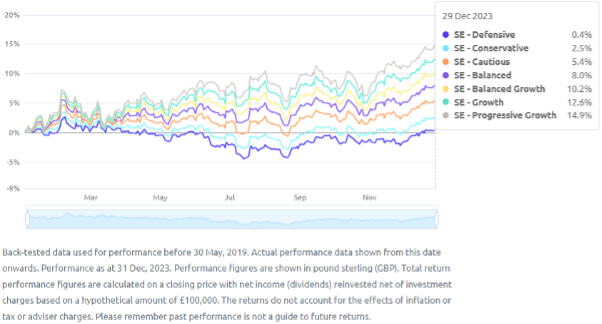

In the last quarter of the year, all our portfolios performed positively. Progressive Growth portfolio was the best performing portfolio with an uplift of 5.7% during Q4 and 14.9% for the full year. The rally in equity markets was the key driver of performance for all portfolios. Fourth quarter gains were primarily driven by increased investor confidence that the Federal Reserve was finished with its campaign of raising interest rates to combat inflation—and that the Fed might even begin cutting interest rates in the coming months. Continued strength in the job market and robust consumer spending also fuelled strong economic growth and corporate profits that helped push stock prices higher. Most of the performance of equity markets in 2023 was driven by enthusiasm over development in artificial intelligence (AI) that helped big technology stocks, magnificent 7 companies (Apple, Amazon, Alphabet Inc. (Google), Meta Platforms, Microsoft, NVIDIA and Tesla), to book over 70% return collectively. All our portfolios had higher exposure to such companies, which proved useful during the period.

Performance of Simply Ethical Online Portfolios in Q3 (01 Oct 2023 – 31 Dec 2023)

Year to Date Performance of Simply Ethical Online Portfolios (01 Jan 2023 – 31 Dec 2023)

During the last quarter, we maintained our asset allocation for all portfolios, however, there were some adjustments within equities and sukuk allocation. We adjusted the equities part of the portfolio to marginally reduce exposure in ‘Magnificent 7’ stocks, thus capturing gains whilst shifting the portfolio to better valued areas of the market. We added an actively managed fund, namely, Schroders Islamic Global Equity to all our portfolios. The fund focuses on a range of equity factors (value, profitability, momentum, low volatility, governance and sustainability) – companies are simultaneously assessed on all targeted equity factors using a fully integrated systematic, bottom-up investment approach. Meanwhile, there were some adjustments made within sukuk allocation, particularly for Defensive, Conservative, Cautious and Balanced portfolios. The overall commodities exposure remained constant for all portfolios. As your active investment manager, we remain vigilant on prevailing risks and continue to manage risks and adjust portfolios where appropriate.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

Data as of 31 December 2023. This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.