Economic and Market Overview

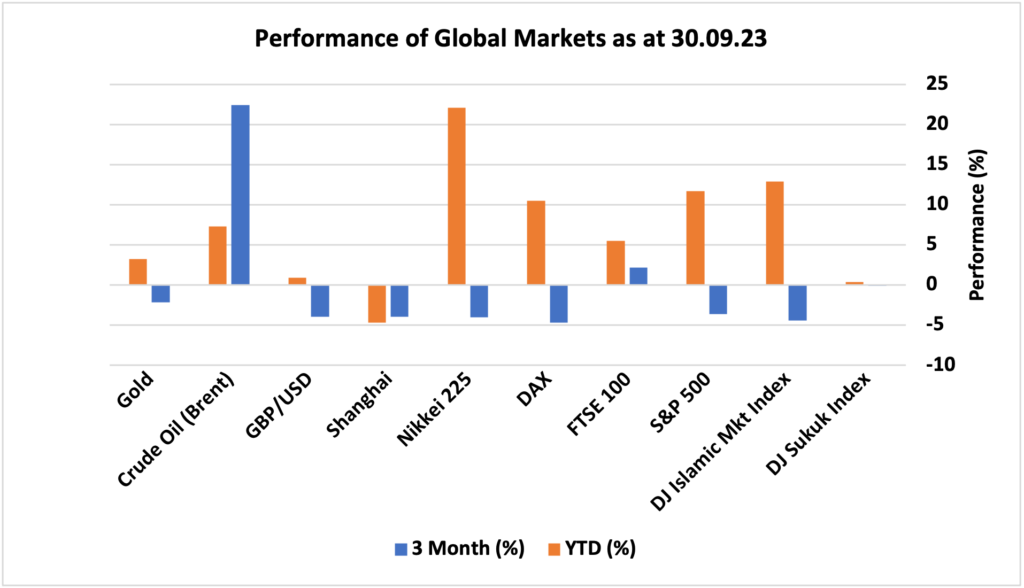

After a good first half of the year for equities, in Q3 major equity markets dropped in value on concerns over the possibility of interest rates remaining higher for longer than anticipated. The yield on the US 10-year Treasury note rose by almost 19% in Q3 from 3.86% to 4.58%, following comments from the Fed that it would cut interest rates more slowly than markets have priced in. The 10-year US Treasury benchmark hit a yield of 4.88% in early trading on Tuesday, October 3rd – its highest yield in 15 years. Macroeconomic picture remains challenging as both interest rates and inflation remains high, particularly in developed economies. Amongst key economies, the recent inflation figures show a decline in the UK and Euro-Area, but no change in the US, whereas inflation rose in Canada, Russia and Brazil. During the quarter, all key central banks including the Federal Reserve, the Bank of England and ECB raised interest rates. During recent meetings in September, both the Federal Reserve and the Bank of England held its policy rate at 5.25% and 5.5% respectively, but the ECB hiked interest rates to 4.5%. On the growth front, recent figures show growth in the US, UK and Euro-Area, however, unemployment data presents a mixed picture. Unemployment in Europe drops, whilst remains somewhat volatile in the US during the year. In the UK, unemployment starts rising based on July data and moreover the house prices continue to decline. Meanwhile, China’s economy showed some signs of improvement in August, particularly in industrial production and retail sales. Inflationary conditions also improved after China slipped into deflation earlier this year. However, the overall outlook for the economy remains uncertain, amid weak overseas demand and a property downturn.

Global equity markets dropped in value during the third quarter with DAX Xetra (Germany) and DJ Islamic Market Index depreciating by 4.71% and 4.43%, respectively. Returns in Q3 have diverged, but still dominate YTD results for US equities as the market has been driven by outsized performance from the ‘Magnificent 7’ to start the year. Japan’s Nikkei 225 Index dropped by just over 4%, however, remains one of the best performing markets since the start of the year. Meanwhile, the UK FTSE 100 index rose just over 2% partly due to its tilt towards energy sector, which was supported by rise in oil prices. Commodities were positive in Q3 as energy prices rose, gold fell pressured by a strong US dollar and higher US Treasury yields. Oil prices rose to over $90 a barrel during Q3 in response to the OPEC+ announcement of extended production cuts through year-end. Recent escalation in Israel-Palestine conflict is expected to keep oil price volatility and at higher levels, at least for the short term – this is likely to make things challenging for policy makers.

Portfolio Commentary

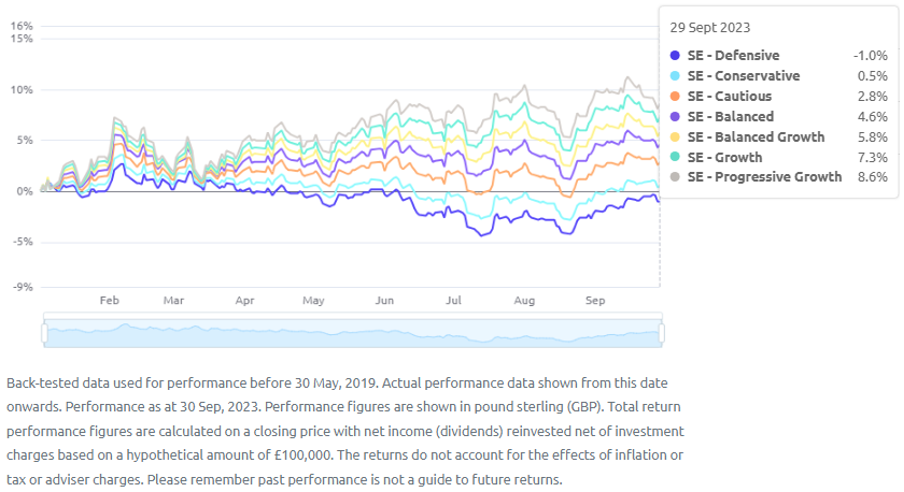

As global equity markets dropped, all our portfolios proved to be resilient by performing positively during the period. The low and medium risk portfolios performed marginally better than the higher risk portfolios (Growth and Progressive Growth) as they had relatively lower exposure to equities. Moreover, a higher exposure to sukuks, which being mostly dollar denominated was helped by stronger dollar against pound, hence delivering net positive sterling returns for UK investors. Similarly, despite drop in gold price in USD, the strength of US dollar added positively to the portfolio returns for all portfolios. Our asset allocation for any given portfolio is built to navigate inherent and emerging risks to limit the downside to portfolio values, whilst seeking to maximise gains overtime.

Performance of Simply Ethical Online Portfolios in Q3 (01 July 2023 – 30 Sept 2023)

Year to Date Performance of Simply Ethical Online Portfolios (01 Jan 2023 – 30 Sept 2023)

During the third quarter, we tactically reduced our allocation towards equities across all our portfolios, whilst simultaneously raising allocation in sukuks as we seek to de-risk the portfolios and moreover realise some gains in equities. The overall commodities exposure remained constant for all portfolios, however, the allocation in Royal Mint Physical Gold was marginally reduced in favour of WisdomTree Physical Silver for Balanced Growth, Growth and Progressive Growth portfolios. Given the macroeconomic backdrop including the possibility of ‘higher rates for longer’; the evolving political uncertainties witnessed by escalation in conflicts around the world; and the dispersion in valuations within and across the global markets, we remain cautious and diligent when picking investments and continue to adjust our broader asset allocation where necessary and appropriate as we navigate through this challenging period.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

Data as of 30 September 2023. This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.