Economic and Market Overview

The world economy and financial markets continue to face uncertainties as inflation remains elevated and interest rates rise to counter high inflation. During the first quarter, inflation in the US slowed to 5% in March. Meanwhile in the UK, it was above 10% and in the Euro Area inflation eased to 6.9% in March. All the key central banks, namely the Fed, ECB and the Bank of England raised interest rates. The Fed raised the fed funds rate by 25bps to 4.75%-5% in March, whereas the ECB raised interest rates by 50 bps to 3.5% and the Bank of England raised its key bank rate by 25bps to 4.25% during its March 2023 meeting.

In march, the news from the banking sector came to fore when Silicon Valley Bank (SVB) faced a bank run. Here is an article detailing what went wrong with SVB. SVB was the 16th largest US bank and was known as the banker for Venture Capitalists (VC funds) and technology start-ups. A contagion effect emerged after the panic and few other banks felt the pain as well. Signature bank is another example that faced similar bank run phenomenon and hence the regulator closed the bank on 12th March 2023. The First Republic Bank and many other banks’ stock prices started plunging as the investment community became vary of potential financial stability and resulting systemic risks. Financial markets observed heightened volatility as investors started to think about a possible contagion in the banking system triggering a financial crisis similar to the Global Financial Crisis (GFC) of 2008. As expected, the regulator intervened to dampen investor concerns, nevertheless, it is still very early to say anything about the health of the financial markets as the monetary tightening cycle is expected to continue for the near future.

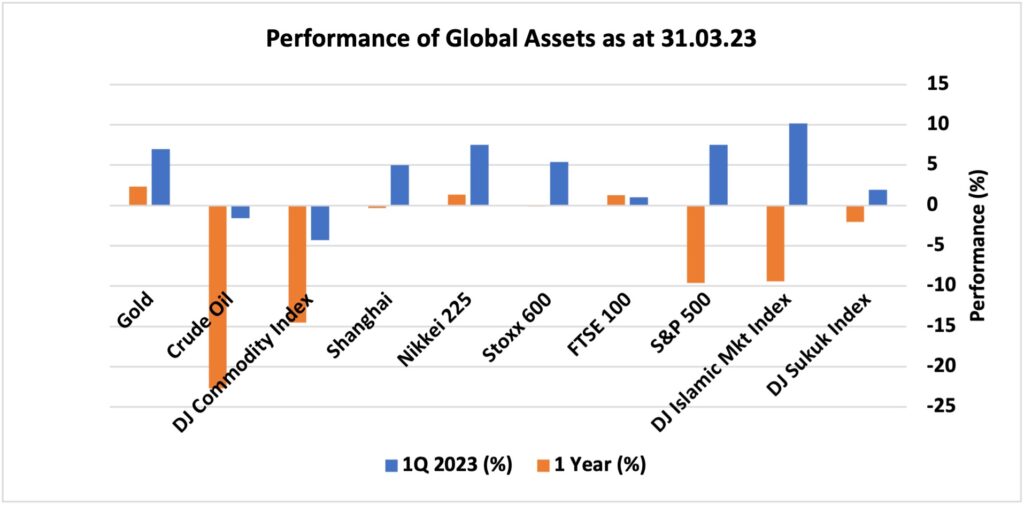

Central banks’ hawkish approach, havoc in the banking sector, geo-political situations kept the financial markets volatile during first quarter of 2023. The VIX index, the volatility risk measure, was highest in mid-March reflecting the banking sector fueled market chaos. However, despite these macro concerns, risk assets provided positive returns as all major equity indices were on the positive trajectory at the end of first quarter 2023. DJ Islamic Markets Index was the best performing equity index that booked 10.14% return and UK FTSE 100 performed worst in the equity asset class with only 1% appreciation in the first quarter of 2023. Other equity markets also rallied with both US S&P 500 index and Japan’s Nikkei 225 surging by over 7%. Gold was the best performing asset with 7.21% return in the month of March, mainly due to adverse news from the banking sector. DJ Sukuk index was up 1.92%. However, commodities did not do well in the first quarter of 2023 with DJ Commodity Index down 4.29% and crude oil down 1.6%.

Portfolio Commentary

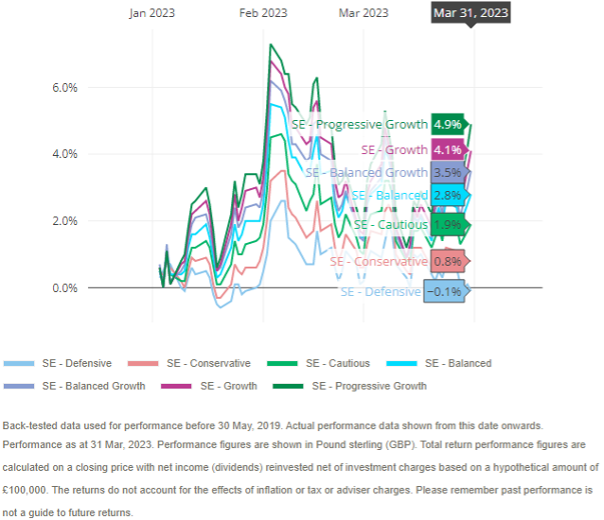

Equity markets and gold in particular rallied during the first quarter of the year as shown above. As a result, all our investment portfolios went up in value with the exception of ‘Defensive’ portfolio that went down by 0.1% due to relatively higher exposure to sukuks (73%). Sukuk investments went down in value as pound rose against US dollar in Q1. In general, most of the sukuks are denominated in US dollars, hence movement in currencies can have an impact on such portfolios. Nevertheless, our preference for higher allocation to equities (15%) and gold (10%) limits the downside related to currency movements, whilst providing long term growth potential for this particular portfolio. ‘Progressive Growth’ portfolio was the best performing portfolio with an upside of 4.9%. This is explained by higher allocation to equities (75%), which performed positively over the period.

Performance of Simply Ethical Online Portfolios in Q1 2023

During the period, a number of changes were made to portfolios. In general, we raised the allocation to emerging market equities for all portfolios (except ‘Balanced’) as emerging market equities offer relatively better valuations compared to developed market equities and moreover, it has the potential to deliver higher returns in the long term, along with diversification benefits. Our overall commodities allocation remained constant; however, we captured some gains in gold and introduced silver in ‘Balanced Growth’, ‘Growth’ and ‘Progressive Growth’ portfolios. We expect coming months to be challenging for the economy and markets as we move into low growth environment in the developed economies. Therefore, we expect equities to remain volatile with the possibility of downside risk. As a result, we had tactically raised our allocation to sukuks by 5% for both ‘Growth’ and ‘Progressive Growth’ portfolio to reduce portfolio risk. As your active investment manager, staying nimble and adjusting investment positions as events unfold will remain key to maintaining portfolio value and growth overtime.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.