Overview

September is rarely a great month for investors, and last month proved no exception as most asset classes dropped in value. Macroeconomic picture remains challenging as both interest rates and inflation remains high, particularly in developed economies. Amongst key economies, the recent inflation figures show a decline in the UK and Euro-Area, but no change in the US, whereas inflation rose in Canada, Russia and Brazil. In September, both the Federal Reserve and the Bank of England held its policy rate at 5.25% and 5.5% respectively, but the ECB hiked interest rates to 4.5%. On the growth front, recent figures show growth in the US, UK and Euro-Area, however, unemployment data presents a mixed picture. Unemployment in Europe drops, whilst remains somewhat volatile in the US during the year. In the UK, unemployment starts rising based on July data and moreover the house prices continue to decline. Meanwhile, China’s economy showed some signs of improvement in August, particularly in industrial production and retail sales. Inflationary conditions also improved after China slipped into deflation earlier this year. However, the overall outlook for the economy remains uncertain, amid weak overseas demand and a property downturn.

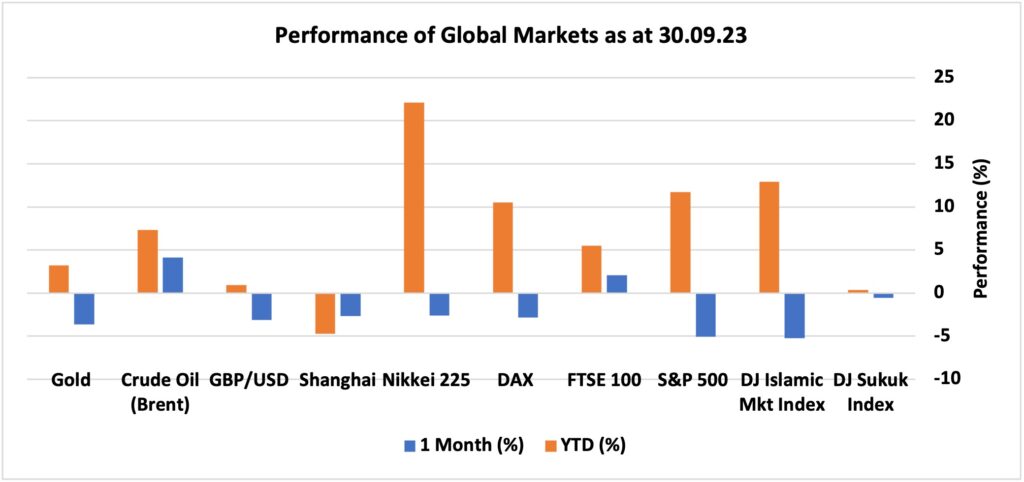

Looking at the performance of major asset classes, the DJ Islamic Market Index was one of the worst performing index in September, dropping by 5.21%. Similarly, S&P 500 and DAX Xerta (Germany) declined by 5.04% and 2.86%, respectively. Meanwhile, the UK FTSE 100 index rose just over 2% partly due to its tilt towards energy sector, which was supported by rise in oil prices. Amongst key commodities, the oil price rose by 4.12%, whilst gold declined by 3.61% during the month.

Market Snapshot

News & Key Events in September

UK

• Consumer price inflation in the UK eased to 6.7% in August 2023 from 6.8% in the previous month.

• The Bank of England held its policy interest rate at 5.25% on September 21st, keeping borrowing costs at their highest level since 2008, as policymakers opted for a wait-and-see approach following the latest inflation and labour data, which suggested that the accumulated impacts of previous policy tightening might be taking effect.

• The UK quarterly economic growth was 0.2% during the second quarter of 2023.

• The Halifax House Price Index dropped by 4.7% yoy in September 2023, following a 4.5% fall in August. It was the biggest decrease in house prices since August 2009.

US

• The annual inflation rate in the US remained steady at 3.7% in September.

• The Federal Reserve kept the target range for the federal funds rate at a 22-year high of 5.25%-5.5% in its September 2023 meeting, but signalled there could be another hike this year.

• The US economy grew at an annualised rate of 2.1% in the second quarter of 2023, compared to the first quarter’s expansion of 2%.

• The unemployment rate in the US was at 3.8% in September of 2023, remaining unchanged from the February 2022 high from the previous month.

Europe

• The inflation rate in the Euro Area declined to 4.3% year-on-year in September 2023, reaching its lowest level since October 2021.

• The ECB hiked interest rates for the 10th consecutive time on September 14th and signalled that it is likely done tightening policy, as inflation has started to decline but is still expected to remain too high for too long.

• The Euro Area GDP expanded by 0.1% on quarter in the three months to June 2023. It follows a 0.1% growth in the previous quarter.

China

• As the rest of the economies struggle with high inflation, the consumer prices rose by 0.1% yoy in August 2023.

• The People’s Bank of China (PBoC) maintained lending rates in September, as policymakers assessed the impact of previous easing measures, including an interest rate cut in August and a recent reduction in the reserve requirement ratio for banks.

• The Chinese economy grew by a seasonally adjusted 0.8% in the second quarter of 2023.

• Chinese property developers continue their struggle to stay afloat as both financing and sales dry up. Weakness in property market is perhaps the most challenging growth headwind for China. Over the past months, a number of new stimulus measures have been announced with the aim of stabilising the housing market.

• Youth unemployment rate in China increased to a record high of 21.30% in June 2023, meaning more than one in five of those between 16 to 24 years old are unemployed.

Others

• The Bank of Japan (BoJ) maintained its key short-term interest rate at -0.1% and that of 10-year bond yields at around 0% in its September meeting by unanimous vote. The central bank also left unchanged an allowance band of 50bps set on either side of the yield target, as well as a cap of 1.0% adopted in July. The annual inflation rate in Japan edged down to 3.2% in August 2023 from 3.3% in the prior month.

• The Bank of Canada held the target for its overnight rate unchanged at 5% in its September 2023 meeting.

• The Reserve Bank of Australia kept its cash rate unchanged at 4.1% during the first meeting under new Governor Michele Bullock.

• The Bank of Russia raised its key interest rate by 100bps to 13% in its September 2023 meeting.

• The central bank of Brazil lowered its key rate by 50 bps to 12.75% for the second consecutive meeting in September 2023.

Disclaimer

Data as of 30 September 2023. This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.