Overview

After a few months (summer period) of lacklustre market performance, November proved to be a month of joy for both equity and fixed income investors. Major central banks kept policy rates steady at their November meetings. The US Fed officials emphasized that any additional policy tightening would consider the cumulative impact of prior rate hikes, the time lags accompanying with how monetary policy impacts economic activity and inflation, and developments in both the economy and financial markets. The US economy continues to show resilience – expanding an annualised 5.2% in Q3 2023. Meanwhile, sadly the ruthless killing of Palestinians particularly in Gaza by occupying Israeli forces continues, despite calls by majority of countries and general public for a ceasefire. The US and UK have sided with the Israeli occupying forces and continue to misuse their UN status to prevent a ceasefire. A temporary ceasefire between Israel and Hamas in the Gaza Strip took effect from 24 November 2023 to 30 November 2023. Since October 7, Palestinians killed by Israeli forces amount to over 20,000, including 8,697 children and 4410 women. Diplomacy continues in the background but no material actions have been taken by neighbouring countries or the Arab nations – any meaningful involvement of those countries could possibly trigger a sharp increase in risk aversion in financial markets, unravelling the prevailing susceptibilities.

Towards the end of November, Charlie Munger passed away at the age of 99. He was Warren Buffett’s right-hand man. His achievements cannot be summarised in this market update and perhaps is a topic for a separate article, however, couple of things worth mentioning. Charlie was the one who taught Warren Buffett that, instead of buying troubled companies at cheap prices, buy wonderful businesses at fair or acceptable prices. Over more than five decades partnership with Warren Buffet, Berkshire Hathaway achieved above 20% annualised returns vs S&P 500 that returned under 10% over the same period, a significant above 10% outperformance. “Berkshire Hathaway could not have been built to its present status without Charlie’s inspiration, wisdom and participation,” Buffett said in a statement.

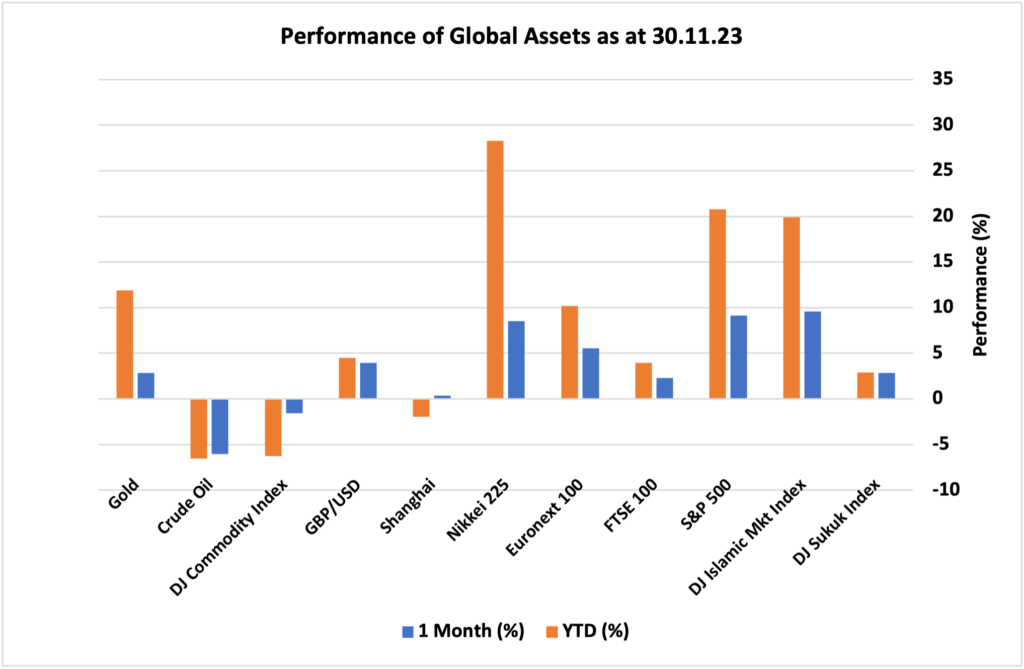

Looking at the performance of major asset classes, equity markets ended the month with a thrilling performance at the backdrop of falling inflation levels in all major economies and the market consensus that interest rates might have peaked. DJ Islamic market index was the leader with 9.58% monthly return followed by US S&P 500 index and Japan’s Nikkei 225 with 9.13% and 8.52%, respectively. Europe’s Euronext 100 got the next spot with 5.56% monthly performance. UK’s FTSE 100 returned only 2.29% in November impacted partially by falling energy prices as FTSE 100 index is energy sector heavy weight and partially by appreciation of UK Pound against US Dollar (3.96% in November) as majority of FTSE 100 constituents’ revenue comes from overseas business operations. China’s Shanghai Index managed to provide only a marginal positive performance as there are still concerns of deflation and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing. On the commodity front, Gold managed to achieve 2.84% positive performance while crude oil is continuing its falling trend with around 6% fall in prices in November amid concerns over slowing global economy after historic speed of rates hike and struggling world’s second largest economy. Overall, DJ Commodity Index fell by 1.58%. Lastly, DJ Sukuk Index surged by 2.86% amid falling yields as market consensus is shifting towards interest rates cut in the first half of 2024.

Market Snapshot

News & Key Events in November

UK

• The inflation rate in the UK dropped to 4.6% in October 2023, down from 6.7% in both September and August, falling short of market expectations of 4.8%. This marks the lowest rate since October 2021, due in part to the recent reduction in energy prices following Ofgem’s decision to lower the cap on household bills.

• The Bank of England maintained its benchmark interest rate at a 15-year high of 5.25% for the second consecutive time during its November meeting.

• The British economy stalled in the third quarter of 2023, 0% growth, the weakest performance in four quarters, but beating forecasts of a 0.1% contraction, first estimates showed.

US

• The annual inflation rate in the US slowed to 3.2% in October 2023 from 3.7% in both September and August.

• The Federal Reserve kept the target range for the federal funds rate at its 22-year high of 5.25%-5.5% for a second consecutive time in November, reflecting policymakers’ dual focus on returning inflation to the 2% target while avoiding excessive monetary tightening.

• The US economy expanded an annualized 5.2% in Q3 2023. It marks the strongest growth since Q4 2021.

Europe

• The inflation rate in the Euro Area declined to 2.4% year-on-year in November 2023, reaching its lowest level since July 2021 and falling below the market consensus of 2.7%.

• As per the Financial Stability Review published in November 2023, Euro area financial stability outlook remains fragile. Higher interest rates reinforce bank profitability, but deteriorating asset quality and higher borrowing costs pose headwinds

China

• China’s consumer prices dropped by 0.2% yoy in October 2023, compared with a flat reading in the prior month and forecasts of a 0.1% fall.

• The People’s Bank of China (PBoC) maintained lending rates at the November fixing, as widely expected. The one-year loan prime rate (LPR), which is the medium-term lending facility used for corporate and household loans, was left unchanged at a record low of 3.45%; and the five-year rate, a reference for mortgages, was kept at 4.2% for the fifth straight month.

• The Chinese economy grew by a seasonally adjusted 1.3% in Q3 of 2023, topping market expectations of 1% and sharply accelerating from a downwardly revised 0.5% increase in Q2.

Others

• The annual inflation rate in Japan rose to 3.3% in October 2023 from 3% in the prior month, pointing to the highest print since July.

• The annual inflation rate in Russia rose to 6.7% in October 2023 from 6% in September, the highest since the fade-away of base effects from the invasion of Ukraine in February and matching market expectations.

• The annual inflation rate in Canada fell to 3.1% in October of 2023 from 3.8% in the previous month, slightly below market expectations of 3.2%.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.