Overview

In May 2026, global financial markets were driven by a combination of resilient economic growth, persistent inflationary pressures, evolving trade policies, and ongoing geopolitical uncertainties. Economic data from the United States and several major economies continued to indicate solid labour markets and consumer spending, leading investors to reassess the timing and pace of potential interest rate cuts by central banks. Trade tensions remained a key focus, with tariff-related discussions and restrictions on strategic industries contributing to uncertainty around global supply chains and international trade flows. Geopolitical developments, particularly in the Russia–Ukraine conflict continued to impact global economies and financial markets. Equity markets generally remained supported by strong corporate earnings, especially within technology and artificial intelligence-related sectors, although elevated valuations increased sensitivity to economic surprises. Overall, investor sentiment in May balanced optimism over economic resilience with caution regarding inflation, trade frictions, and geopolitical risks.

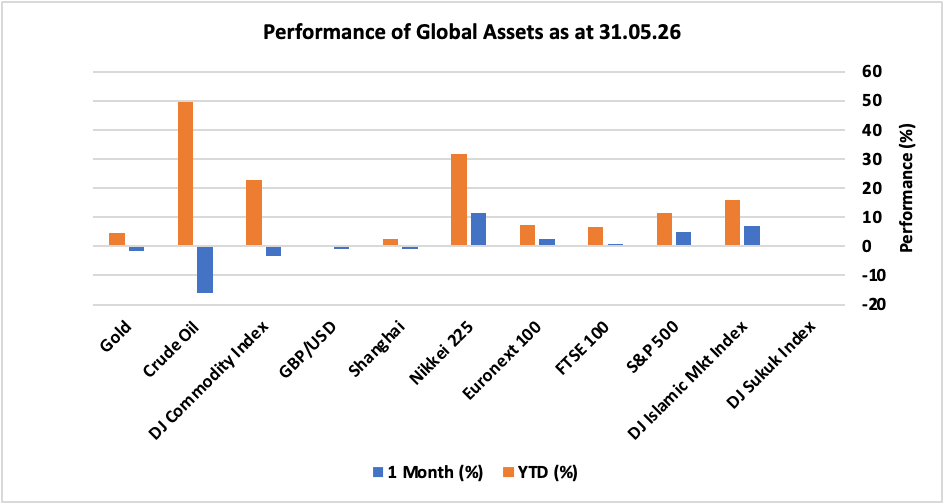

Looking at the performance, major global financial assets experienced a mixed performance where equity markets continued positive momentum amid AI optimism while commodities went down and sukuks ended flat. Resilient corporate earnings and positive developments in AI theme contributed to the positive momentum equities. Equity markets delivered a strong positive performance as Japan’s Nikkei 225, DJ Islamic Markets Index, and US S&P 500 climbed by 11.5%, 6.9%, and 4.95%, respectively. While in Europe, EU Euronext 100 and UK FTSE 100 delivered positive 2.5% and 0.9%, respectively, falling short of global peers amid potential economic shocks impacted by rising energy costs and resulting inflationary pressures. However, China’s Shanghai index declined roughly 1%. DJ Sukuk Index ended the month up 0.39%. In commodities, DJ Commodity index declined by 3.50% driven by over 16% decline in Crude oil prices while gold fell by 1.6%. Lastly, UK pound depreciated 0.89% against the US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in May 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in May:

UK

- The annual inflation rate in the UK slowed to 2.8% in April 2026 from 3.3% in March, coming in below market expectations of 3.0% and marking the lowest reading since March last year.

- The UK economy expanded by 0.6% in Q1 2026, matching market expectations and marking the strongest growth since Q1 2025. This follows an upwardly revised 0.2% increase in the previous quarter.

- The UK unemployment rate rose to 5.0% in the three months to March 2026, above expectations and February’s 4.9%.

US

- The annual inflation rate in the US accelerated to 3.8% in April 2026, the highest since May 2023, and compared to 3.3% in March. Figures came above forecasts of 3.7% as the oil shock triggered by the war with Iran continues to push prices higher.

- A majority of Fed officials highlighted that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%, minutes from the FOMC meeting in April 2026 showed.

- The US economy expanded an annualized 1.6% in Q1 2026, up from 0.5% in Q4 but below 2% in the advance estimate, primarily reflecting downward revisions to investment and consumer spending.

- The US unemployment rate held at 4.3% in April 2026, in line with market expectations.

Europe

- Eurozone consumer price inflation reached 3.2% in May 2026, up from 3.0% in April and matching market expectations, according to preliminary data. This marks the highest rate since September 2023, staying significantly above the European Central Bank’s 2.0% target.

- A number of ECB members viewed the April decision to keep rates unchanged as a close call and indicated they would have supported a rate hike had it been proposed, according to the latest ECB meeting minutes. Policymakers warned that the energy-driven supply shock was proving more persistent than previously expected, increasing the risk of broader and more entrenched inflationary pressures, while the war in the Middle East was seen as a key source of uncertainty for both inflation and growth.

- Eurozone economic growth was confirmed at 0.1% in the first quarter of 2026, marking the weakest expansion since Q2 2025, reflecting pressure from tight energy supplies after the Middle East conflict disrupted flows of oil, its byproducts, and liquefied natural gas.

- The Euro Area seasonally adjusted unemployment rate rose to 6.3% in April 2026, the same as in the previous month and above market expectations of 6.2%.

China

- China’s annual inflation accelerated to 1.2% in April 2026 from 1.0% in the previous month, exceeding market expectations of 0.8%

- The People’s Bank of China maintained its key lending rates at record lows for a 12th straight month in May 2026, matching market expectations.

- China’s GDP grew 1.3% qoq in Q1 2026, matching market expectations and following a 1.2% increase in Q4. The latest result marked the strongest quarterly expansion since Q4 of 2024, supported by continued policy backing from Beijing.

- China’s surveyed urban unemployment rate edged down to 5.2% in April 2026 from a more than one-year high of 5.4% in the previous month, coming in below market expectations of 5.3% and marking its lowest level since January 2026.

Others

- Japan’s annual inflation edged down to 1.4% in April 2026 from 1.5% in the prior month.

- The headline inflation rate in Canada rose to 2.8% in April of 2026 from 2.4% in the previous month, the highest in two years, albeit firmly under the market consensus of 3.1%.

Russia’s headline annual inflation rate eased to a four-month low of 5.6% in April 2026 from 5.9% previously and below the expected 5.8%.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.