Overview

March proved to be another good month for financial markets as investors continued to be somewhat optimistic. The prevailing investor confidence mainly relies on three key factors: resilient economies and corporate profits, optimism on the AI hype, and expectations that interest rates will start taking downward trajectory in the near future. Inflation rates are moderating, and rates are peaked, both factors indicate central bankers will pivot in coming months to bring rates down. However, resilient economic growth and sticky inflation could lead to the possibility of interest rates and bond yields staying higher for longer than the markets are pricing in, which is a tail risk for the financial markets.

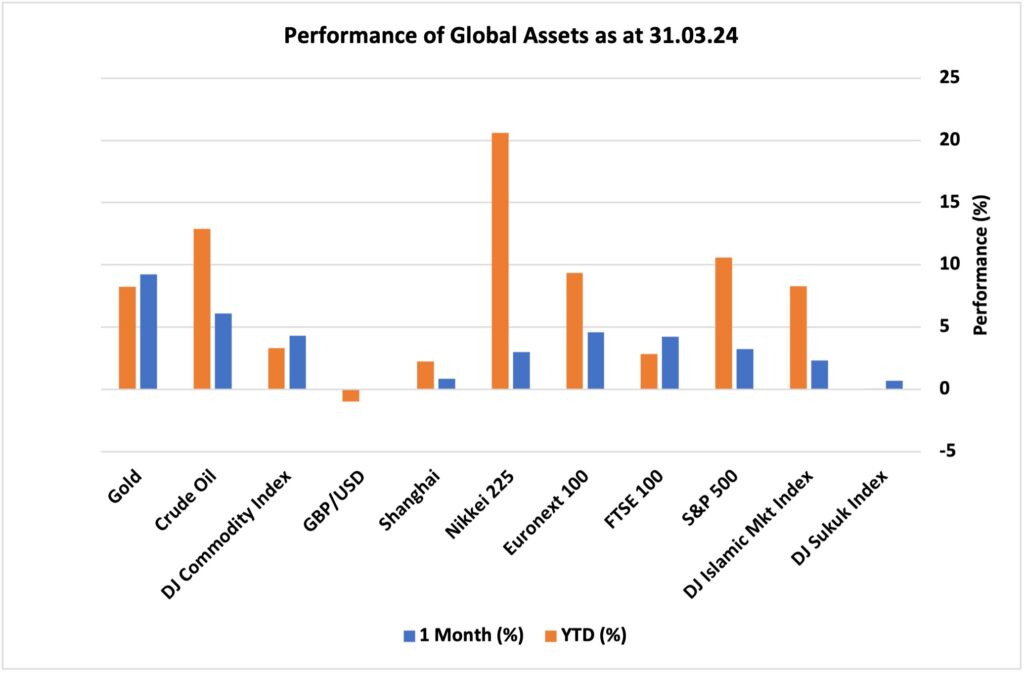

Looking at the performance of major asset classes, equity markets continued to show strength and ended the month on a positive note amid moderating inflation levels in all major economies and hopes that interest rates will start easing sometime in coming months. In equity markets, European stocks took the lead where Euronext 100 surged 4.6% followed by UK FTSE 100 index that increased 4.2% amid inflation falling quicker than what was anticipated. The US S&P 500 index gained 3.2% while Japan’s Nikkei 225 notched another 3%. DJ Islamic market index, the benchmark for shariah-compliant investments, increased 2.3% in March. Commodity markets delivered best performance with gold appreciating 9.2% and DJ Commodity Index increased by 4.30% while Oil surged just over 6% in March amid conflicts in Middle East and Red Sea in addition to OPEC+ drive to cut supply. On the fixed income side, DJ Sukuk Index gained 0.70% amid moderating yield curves. Lastly, UK pound largely remained flat against US dollar as policy makers on both sides decided to keep interest rates unchanged.

Market Snapshot

News & Key Events in March

UK

• The inflation rate dropped to 3.4% year-on-year in February 2024, down from 4% recorded in both January and December and falling below the market expectation of 3.5%.

• The Bank of England maintained the Bank Rate at 5.25% during its March meeting, its highest level since 2008, as policymakers awaited clearer signals indicating that the country’s persistent inflationary pressures had subsided.

• The UK’s economy shrank by 0.3% in the final quarter of 2023, entering a technical recession for the first time since the aftermath of the COVID-19 outbreak in the initial half of 2020, as high inflation, record borrowing costs, and weak external demand weighed on demand and activity.

• The Chancellor Jeremy Hunt announced pre-election spring budget statement on 6th March 2024 and called it a “budget for long term growth”. He said the UK economy has managed to deal with the financial crisis driven by the pandemic and energy crisis caused by war in Europe. He admitted that rates remain high in a motion to bring down inflation. Here are the key highlights of Spring Budget 2024.

US

• Annual inflation rate in the US unexpectedly edged up to 3.2% in February 2024, compared to 3.1% in January.

• The Federal Reserve left the fed funds rate steady at a 23-year high of 5.25%-5.5% for a fifth consecutive meeting in March 2024, in line with market expectations. Policymakers still plan to cut interest rates three times this year, similar to the quarterly forecasts in December.

• The US economy expanded an annualised 3.4% in Q4 2023, slightly above the 3.2% previously reported, supported by consumer spending and non-residential business investments, according to the third estimate from the BEA.

Europe

• The consumer price inflation rate in the Euro Area was confirmed at 2.6% year-on-year in February 2024, the lowest rate in three months but still exceeding the European Central Bank’s target of 2%.

• The European Central Bank maintained its interest rates at historically high levels during its March meeting, as policymakers balanced concerns over a looming recession with persistently elevated underlying inflationary pressures.

• The Euro Area economy stagnated in the fourth quarter of 2023, following a 0.1% contraction in the previous three-month period, as persistently high inflation, record borrowing costs, and weak external demand continued to exert downward pressure on growth.

• As assessment report by the European Environment Agency (EEA), asserted that the bloc is not prepared to respond to the increasingly severe risks that climate change poses. The policy adviser’s first-ever report on the threats faced by the world’s fastest-warming continent warns of “catastrophic” consequences.

China

• China’s consumer prices rose by 0.7% yoy in February 2024, above market forecasts of 0.3% and a turnaround from the sharpest drop in over 14 years of 0.8% in January.

• The People’s Bank of China kept benchmark lending rates unchanged at the March fixing, as widely expected. The one-year loan prime rate (LPR), the benchmark for most corporate and household loans, was retained at 3.45%. Meanwhile, the five-year rate, a reference for property mortgages, was maintained at 3.95% following the biggest-ever reduction of 25bps in February.

• The Chinese economy grew by a seasonally adjusted 1% in Q4 of 2023, matching market expectations but moderating from an upwardly revised 1.5% increase in Q3. This was the sixth consecutive period of quarterly expansion, with weakness in the property sector continuing to drag on the broader economic recovery. China has set a 2024 growth target of around 5% in its annual parliamentary meeting.

Others

• The annual inflation rate in Japan climbed to 2.8% in February 2024 from 2.2% in the prior month, accelerating for the first time in four months and reaching the highest since last November.

• The annual inflation rate in Russia sped up to a one-year high of 7.7% in February 2024. The Bank of Russia held its benchmark interest rate at 16% in its March 2024 meeting, as expected, but signalled that it will leave borrowing costs at a restrictive level for a long period to achieve its disinflation target.

• The annual inflation rate in Canada slowed further to 2.8% in February 2024 from 2.9% in January 2024 and marking the lowest reading since June 2023.

• Shooting at Moscow concert venue leaves over 130 dead. The attack on a Moscow concert hall was the worst in Russia for years.

• On March 04, 2024, the OPEC Secretariat noted the announcements of several OPEC+ countries extending additional voluntary cuts of 2.2 million barrels per day, aimed at supporting the stability and balance of oil markets.

• Bitcoin, on March 14, 2024, set a new record of $73,750, with a market capitalisation reaching $1.44 trillion.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.