Overview

In June 2026, global financial markets were shaped by a combination of rising inflation, evolving central bank expectations, escalating trade tensions, and heightened geopolitical risks. While inflation continued to remain a concern in several major economies, policymakers remained cautious, signalling that interest rate cuts would be data dependent. Renewed trade negotiations among major economies increased uncertainty around global supply chains, weighing on export-oriented sectors and manufacturing activity. Meanwhile, geopolitical tensions—including the ongoing Russia–Ukraine conflict and instability in the Middle East—continued to complicate trading environment, while supporting elevated energy prices. Equity markets displayed mixed performance, with AI-driven technology stocks remaining vulnerable to changing narratives. Overall, investors entered the second half of 2026 balancing uncertain macroeconomic fundamentals against persistent geopolitical and trade-related risks.

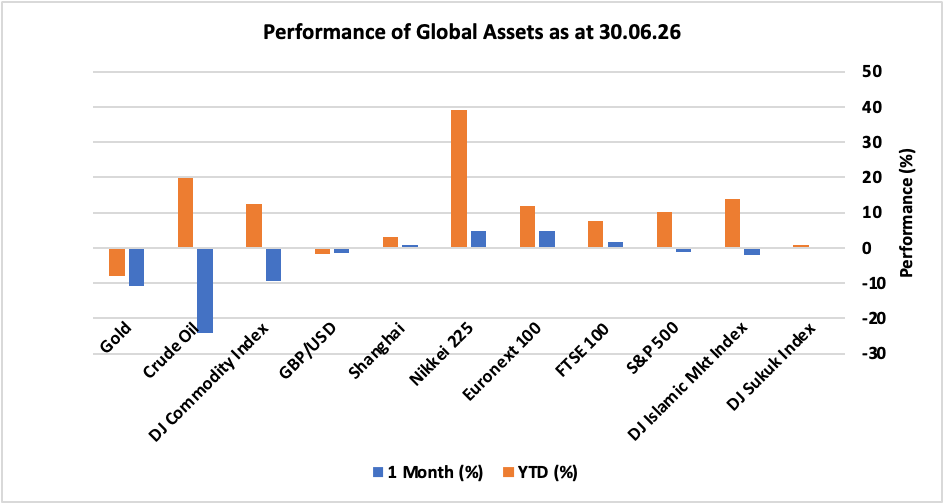

Looking at the performance, major global financial assets experienced a mixed performance where European and Asian equity markets continued positive momentum amid rotation out of US tech and overall US equity markets, which delivered negative returns, while commodities went down significantly due to oil and gold correction amid peace talks in the Middle East. Japan’s Nikkei 225 delivered strong 4.67% returns followed by Europe’s Euronext 100 that rose by 4.65%. UK FTSE 100 rose 1.65% during the month. On the other hand, US S&P 500 and DJ Islamic Markets Index declined by 1.22% and 2.12%, respectively. DJ Sukuk Index ended the month up 0.2%. Commodities fell sharply as DJ Commodity index dropped by 9.4% driven by over 24% decline in Crude oil prices while gold fell by 10.7%. Lastly, UK pound depreciated 1.56% against the US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in June 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in June:

UK

- The annual inflation rate in the UK stood at 2.8% in May 2026, unchanged from the previous month and below market expectations of 3.0%. The reading remained at its lowest level since March last year.

- The Bank of England voted 7-2 to keep Bank Rate unchanged at 3.75% in June 2026, as policymakers weighed easing inflation against continued uncertainty from volatile global energy markets linked to Middle East tensions. Two members of the Monetary Policy Committee preferred a 0.25 percentage point hike to 4%.

- The UK economy expanded by 0.6% quarter-on-quarter in Q1 2026, confirming preliminary estimates and accelerating from a revised 0.1% growth in Q4. This marked the strongest quarterly expansion since Q1 2025.

- The UK unemployment rate fell to 4.9% in the three months to April 2026, defying expectations that it would remain at 5.0%. The number of unemployed people declined by 105 thousand to 1.764 million.

US

- The annual inflation rate in the US rose to 4.2% in May 2026, marking its highest level since April 2023, from 3.8% in April and in line with market expectations. This represents the third consecutive monthly acceleration in headline inflation.

- The Fed kept the federal funds rate unchanged at 3.50%-3.75% for a fourth consecutive meeting in June 2026, in line with expectations. This is the first meeting under new Fed Chair Kevin Warsh.

- The US economy expanded an annualized 2.1% in Q1 2026, revised up from 1.6% in the second estimate, and above 0.5% in Q4 2025.

- The US unemployment rate remained at 4.3% in May 2026, matching market expectations.

Europe

- Eurozone consumer price inflation held at 3.2% in May 2026, the highest since September 2023 and well above the European Central Bank’s 2.0% target.

- The European Central Bank raised interest rates by 25 basis points at its June 2026 meeting, the first increase since 2023, as policymakers emphasized their commitment to anchoring inflation at the 2% medium-term target.

- The Eurozone economy shrank by 0.2% in the first quarter of 2026, revised down from an initially reported 0.1% growth, according to final EUROSTAT data.

- The Euro Area seasonally adjusted unemployment rate rose to 6.3% in April 2026, the same as in the previous month and above market expectations of 6.2%.

China

- China’s annual inflation held steady at 1.2% in May 2026, unchanged from the previous month but slightly below market expectations of 1.3%.

- The People’s Bank of China kept its key lending rates at record lows for a 13th straight month in June 2026, as widely expected. The move reflected caution over the fallout from the conflict in the Middle East, even as growth momentum has recently sputtered amid mixed economic data.

- China’s GDP grew 1.3% qoq in Q1 2026, matching market expectations and following a 1.2% increase in Q4. The latest result marked the strongest quarterly expansion since Q4 of 2024, supported by continued policy backing from Beijing.

- China’s surveyed urban unemployment rate edged lower to 5.1% in May 2026, compared with both market expectations and the previous month’s 5.2%.

Others

- Japan’s annual inflation rate edged higher to 1.5% in May 2026 from 1.4% in the previous month, as declines in electricity and gas prices moderated amid the expiration of government subsidies.

- The Bank of Japan lifted its key short-term rate by 25bps to 1.0% in a 7-1 vote at its June meeting, marking the highest level since September 1995 and aligning with market expectations. The decision aimed at preventing the Iran war-driven energy shock from fueling broader inflation.

- The headline inflation rate in Canada rose to 3.2% in May of 2026 from 2.8% in the previous month, ahead of market expectations of 3% and the 2.8% rate from the previous month to mark the fastest inflation rate since December 2023.

- The Bank of Canada left the target for its benchmark overnight rate steady at 2.25% for a fifth consecutive meeting in June 2026, in line with expectations. Policymakers said that so far, there has been limited evidence of broad-based pass-through of higher energy prices to other consumer prices.

- Russia’s headline annual inflation rate fell for the second month to 5.3% in May 2026, down from 5.6% in April and below market estimates of 5.4%.

The Bank of Russia cut its policy rate by 25bps to 14.25% in its June 2026 decision, contrasting with the median market consensus of a 50bps cut to 14%. The central bank noted that pro-inflationary risks prevailed in the medium term when citing the warrant for restrictive monetary policy.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.