Overview

February was a good month for stock market with relatively strong earnings reports and resilient macroeconomic data combined with signs of an uptick in European activity, all contributing to monthly as well as year-to-date gains. In contrast, fixed income markets were broadly down amid strong US dollar and surging yields. The economic resilience, together with signs that inflationary pressures have not yet entirely dispelled, suggest that key central banks will likely be on hold for a little longer than previously expected. Fixed income markets (i.e., sukuks) therefore suffered given the decreased likelihood of pending rate cuts. Meanwhile, the UK economy slid into a technical recession in the final quarter of 2023. The Office for National Statistics said UK GDP shrank by 0.3% in the final three months of the year, making the second successive quarterly decline. According to the UK Finance Minister Jeremy Hunt, high inflation remains “the single biggest barrier to growth,” since it is forcing the Bank of England to keep interest rates strong and stalemate economic growth.

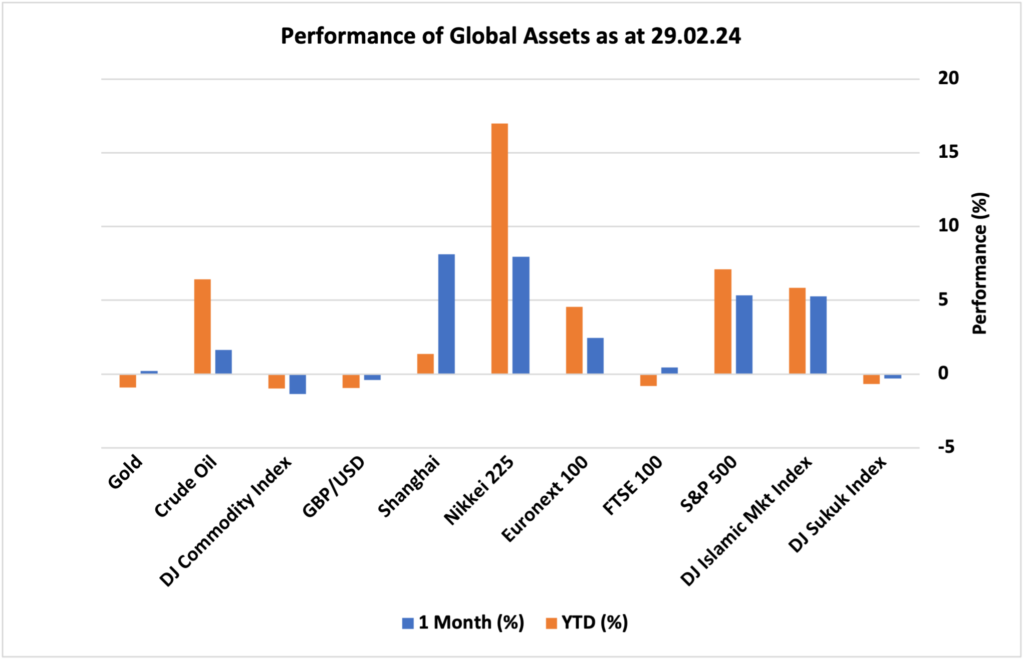

Looking at the performance of major asset classes, equity markets showed a positive momentum in February amid falling inflation levels in all major economies and hopes that interest rates will take downward trajectory sometime in the first half of 2024. Asian markets grabbed investors’ focus as both Japan’s Nikkei 225 and China’s Shanghai Index surged roughly 8% as these markets are perceived to be undervalued relative to other advanced markets, particularly US and Europe. In China, Beijing is on the forefront to fuel the economy through easy monetary policy amid weakness in the property sector that is continuing to drag on the broader economic recovery. The next best performing equity markets were the US S&P 500 index and DJ Islamic market index, both appreciated by just over 5%, which are pricing in rate cuts in the near future. European shares, represented by Euronext 100, surged nearly 2.5% while UK FTSE 100 index increased 0.5% only, reflecting a looming recession and uncertainty around macroenvironment. On the commodities side, oil surged 1.6% in February amid conflict in Middle East and Red Sea in addition to OPEC+ drive to cut supply. DJ Commodity Index was down by 1.40%. On the fixed income side, DJ Sukuk Index fell 0.30% after dollar strengthened and yields started upward tendency as officials appeared reluctant to cut rates pre-mature. Lastly, UK pound fell 0.4% against US dollar as US economy looks more resilient relative to its UK counterpart.

Market Snapshot

News & Key Events in February

UK

• The UK inflation rate was unchanged at 4% in January 2024, holding close to November’s two-year low and falling below the market expectation of 4.2%.

• The Bank of England kept the key Bank Rate unchanged at a 16-year high of 5.25% for the fourth consecutive time during its first meeting of 2024, in line with market expectations. However, two policymakers preferred to increase it by 25bps while one member preferred to reduce it by 25bps.

• The British economy contracted 0.3% on quarter in Q4 2023, following a 0.1% decline in Q3. Technically, the UK economy entered recession amid a broad-based decline in output.

• Labour scraps its plans for a £28bn annual green investment, with Sir Keir Starmer saying the policy is unaffordable because of the Conservatives’ economic record. In response, Sunak says Starmer’s “U-turns on major things, he can’t say what he would do differently”.

US

• The annual inflation rate in the US fell back to 3.1% in January 2024 following a brief increase to 3.4% in December.

• The US economy expanded an annualized 3.2% in Q4 2023, slightly below 3.3% in the advance estimate, following a 4.9% growth in Q3.

• According to Energy Secretary Granholm, the US is on track to meet 50% EV target by 2030 despite slowing growth. On the other hand, Apple has cancelled work on its electric car, a decade after it kicked off the project. Staff working on the project will be shifted to the company’s Artificial Intelligence (AI) division, mainly, Generative AI.

Europe

• The consumer price inflation rate in the Euro Area declined to 2.6% year-on-year in February 2024, down from 2.8% in the previous month. It was the lowest rate in three months but still exceeded the European Central Bank’s target of 2%.

• The European Central Bank officials agreed that it was premature to discuss interest rate cuts, despite recent indications of cooling inflationary pressures across the Eurozone, as shown in the minutes from the most recent ECB meeting. They expressed concerns that such a move might be premature and could potentially hinder or delay the timely return of inflation to target levels.

• The Euro Area economy stagnated in the last quarter of 2023, following a 0.1% contraction in the previous three-month period, as persistently high inflation, record borrowing costs, and weak external demand continued to exert downward pressure on growth.

China

• China’s consumer prices fell by 0.8% yoy in January 2024, the most in more than 14 years. It was the fourth straight month of decline in CPI, the longest streak of drop since October 2009.

• The People’s Bank of China (PBoC) slashed its reference for mortgages, the 5-year loan prime rate, by 25bps to 3.95% at the February fixing, more than market forecasts of a reduction of 15bps. It was the first rate cut since June 2023 and the largest since that rate was introduced in 2019, as the board ramped up efforts to spur credit demand and reverse a property downturn. Meanwhile, the 1-year rate was retained at 3.45%, defying consensus of a drop of 15bps. Both key lending rates are at record lows.

• The Chinese economy grew by a seasonally adjusted 1% in Q4 of 2023, matching market expectations but moderating from an upwardly revised 1.5% increase in Q3. This was the sixth consecutive period of quarterly expansion, with weakness in the property sector continuing to drag on the broader economic recovery.

• The Chinese Coast Guard (CCG) pledged to begin conducting regular maritime inspections around Taiwan-controlled Kinmen Island. Normalizing PRC maritime enforcement around the island will erode Taiwan’s control over its territorial waters and risk confrontations between the PRC and Taiwan’s maritime law enforcement.

Others

• Israeli military continues its aggression against civilians in Gaza. Over 30,000 civilians including 12,000 children have been killed by the occupying Israeli forces. The deliberate restriction of aid by the Israeli forces is resulting in famine, which is putting at risk the lives of over 2.3m living in Gaza.

• Bitcoin breaks $60,000: The bitcoin rally continued as the cryptocurrency crossed another big threshold at $60,000, inching closer and closer to its all-time high amid upcoming halving, approval of spot Bitcoin ETFs, Momentum and FOMO.

• Several OPEC+ countries announced extension of additional voluntary cuts of 2.2 million barrels per day for the second quarter of 2024.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.