Overview

The month of February closed on a negative note for many asset classes after a strong month of January. This was mainly driven by the renewed pessimism in the markets about the state of the economies, level of inflation and interest rates, and rising geopolitical concerns. Stronger economic data suggests that the inflation will remain at elevated levels and above the target levels, longer than what the markets had anticipated in January. There seems to be a clear gap between market expectations and Fed’s declared intentions. Markets expect the Fed is close to ending rate rises and should start cutting them towards the end of 2023, however, Fed’s intention appears to keep the rates higher for longer and consider cutting them somewhere in 2024. Investors have started to realise that fighting with Fed may not prove fruitful, therefore, they have lowered their optimism, so the markets ended February with negative returns for many of the asset classes.

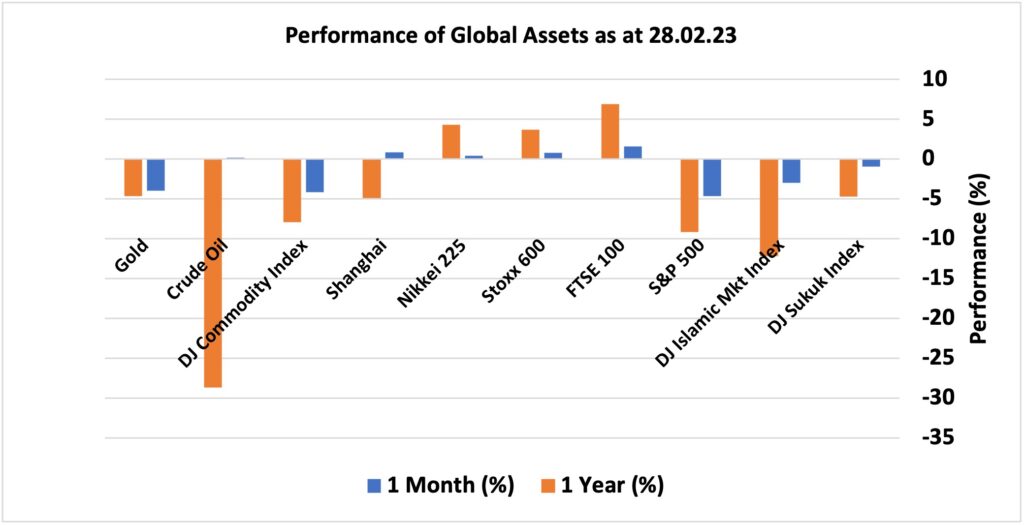

US equities were the worst performing asset class as S&P 500 plummeted 4.69% in February, reversing almost all of the gains of the previous month (January 2023). DJ Islamic Markets Index dropped 3%, however, UK broad market index, FTSE 100, soared 1.6%. DJ Commodity Index fell 4.17% and Gold lost 3.96% in February. Similarly, DJ Sukuk Index fell almost 1% amid rising yields implying interest rates would rise in coming months (bond’s prices fall as yields rise). On a yearly basis, the US equity market barometer dropped 9.18%, DJ Islamic Market Index fell 12.21% while UK FTSE 100 achieved 6.9% in the same period. Crude oil remained flat in February; however, it was the worst performer among all asset classes with 28.7% drop in price over the last one-year period. FTSE 100 Index outperformed all other assets on yearly performance basis with an increase of 6.9% followed by Nikkei 225 with 4.26% upside.

Market Snapshot

News & Key Events in February

UK

• The Bank of England voted by a majority of 7-2 to raise interest rates by 50 basis points to 4% during its February meeting, pushing the cost of borrowing to the highest level since late-2008. It was the 10th consecutive rate hike.

• Annual inflation rate in the UK fell to 10.1% in January of 2023 from 10.5% in December, below market forecasts of 10.3%. Inflation fell for a third consecutive month to the lowest since September last year.

• The British economy stalled in the last quarter of 2022, following a downwardly revised 0.2% fall in the previous period, and narrowly escaping a recession. Figures came in line with market expectations, preliminary estimates showed.

US

• Almost all FOMC participants agreed that it was appropriate to raise the target range for the federal funds rate by 25bps at the first monetary policy meeting of 2023, although a few officials favoured raising it by 50bps, minutes from the last meeting showed.

• The annual inflation rate in the US slowed only slightly to 6.4% in January of 2023 from 6.5% in December, less than market forecasts of 6.2%. Still, it is the lowest reading since October of 2021.

• The US economy expanded an annualized 2.7% on quarter in Q4 2022, slightly below 2.9% in the advance estimate. Consumer spending rose 1.4%, the least since Q1 2022 and below 2.1% in the advance estimate.

Europe

• The European Central Bank governing council member, Gabriel Makhlouf mentioned in a recent interview with the Wall Street Journal that the bank could increase interest rates above 3.5% and isn’t likely to cut them again this year since the institution moves forcefully to bring inflation back to target.

• The consumer price inflation in the Euro Area was revised slightly higher to 8.6% year-on-year in January 2023, up from a preliminary estimate of 8.5% and well above the European Central Bank’s target of 2%.

• The Eurozone quarterly economic growth was confirmed at a meagre 0.1% in the fourth quarter of 2022, down from a 0.3% expansion in the previous three-month period.

• Germany’s consumer price inflation remained unchanged at 8.7% year-on-year in February 2023, not far from a peak of 8.8% seen in October and November and above market expectations of 8.5%.

• The German economy shrank 0.4% on quarter in the last quarter of 2022, much worse than initial estimates of a 0.2% decline, marking the first drop in GDP in nearly two years.

China

• The People’s Bank of China (PBoC) kept its key lending rates steady for the sixth straight month at February fixing, as widely expected. The one-year loan prime rate (LPR), which the medium-term lending facility uses for corporate and household loans, was left unchanged at 3.65%; while the five-year rate, a reference for mortgages, was maintained at 4.3%.

• China’s annual inflation rate rose to 2.1% in January 2023 from 1.8% in December, compared with market forecasts of 2.2%. This was the highest reading in 3 months, as prices of food jumped and those of non-food gained further on the back of the Lunar New Year festival and the removal of pandemic measures.

• The Chinese economy unexpectedly showed no growth on a seasonally adjusted basis in the three months to December of 2022, compared with market consensus of a 0.8% contraction and after a 3.9% expansion in the third quarter.

Others

• The annual inflation rate in Japan rose to 4.3% in January 2023 from 4% in the prior month. This was the highest reading since December 1981, amid a rise in prices of imported raw commodities and yen weakness.

• Russia’s GDP shrank by 3.7% year-on-year in the third quarter of 2022. The annual inflation rate in Russia edged down to 11.8% in January of 2023 from 11.9% in December, missing market expectations of 11.5%.

• The annual inflation rate in Australia climbed to 7.8% in Q4 of 2022 from 7.3% in Q3 and above market forecasts of 7.5%. This was the highest print since Q1 1990, boosted by rising costs of food, automotive fuel, and new dwelling construction.

• Canada’s annual inflation rate fell to 5.9% in January of 2023, the least since February 2022 and below market expectations of 6.1%, slowing from the 6.3% in the previous month amid base-year effects.

Disclaimer

Data as of 28 February 2023. Past performance is not a reliable indicator of current or future returns. This overview contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.