Overview

December recorded another good month for investors followed by November’s joyous performance for both equity and fixed income markets. Major central banks kept policy rates steady at their December meetings and signalled the end of tightening. The US Fed officials emphasized that there may be at least three rate cuts next year, although markets may be expecting more as it appears to be ‘priced for soft landing’. The sharp U-turn from the central banks ignited one of the biggest post-meeting rallies across risk assets in recent years. The combination of looming rate cuts and recent economic data shows that the economy remains resilient, reinforced prospects of a ‘soft landing’ for the US economy.

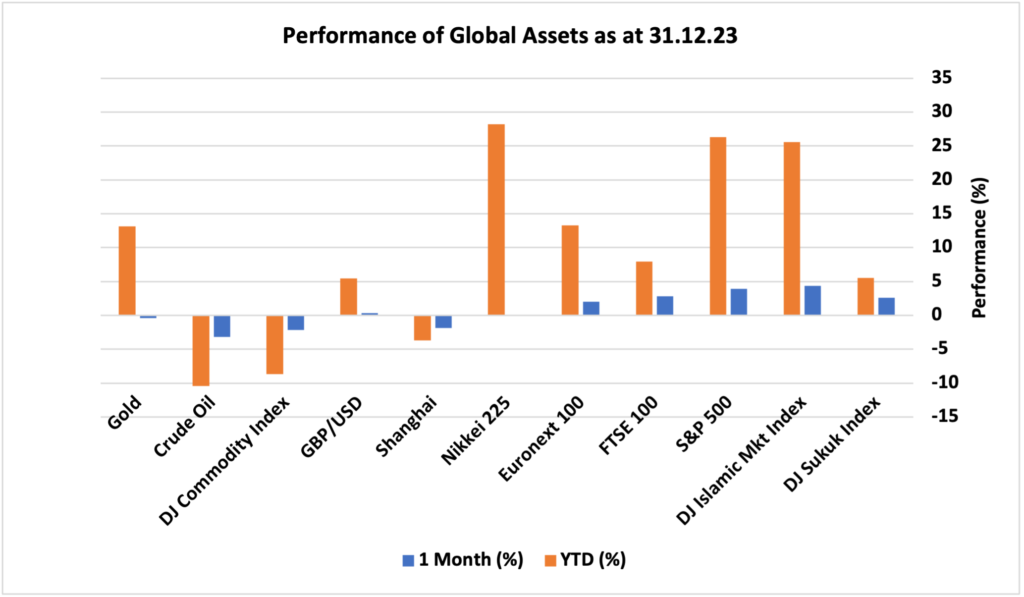

Meanwhile, the Chinese market trailed global peers with the Shanghai Index dropping by 1.87% in December. The index is down by 3.7% on annualised basis compared to Japan and US markets, which surged over 20% in 2023. The key events pricing in are growth concerns, mixed economic data, and geopolitical tensions, which are weighing on investors’ enthusiasm for equities in the region. Moreover, the credit ratings agency Moody’s has put credit ratings of several Chinese Local Government Financing Vehicles (LGFVs) on review for downgrade amid negative outlook for the country’s sovereign bonds. Moody’s cited that the increase in debt burdens, deteriorating liquidity conditions of country’s financial institutions, and weak forecasts for the Chinese economy, despite government efforts to bolster growth, are the reasons for their action.

Looking at the performance of major asset classes, equity markets continued the upside trend from the previous month ended December at a good note amid falling inflation levels in all major economies and signals from central banks that interest rates will start moving downward in the first half of next year. DJ Islamic market index was the leader with 4.35% monthly return followed by the US S&P 500 index and UK FTSE 100 with 3.92% and 2.81%, respectively. Europe’s Euronext 100 got the next spot with just over 2% return in December. Nikkei 225 was mostly flat, while China’s Shanghai Index fell 1.87% as there are still concerns of deflation and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing. On an annualised basis, equity markets booked 2023 as one of the best performing years in the equity markets recent history. On the fixed income side, the DJ Sukuk Index returned 2.56% amid falling yields as market consensus is shifting towards possible interest rates cut in the first half of 2024. Commodities remained under pressure where crude oil fell over 3% amid concerns over slowing global economy after historic speed of rate hikes and struggling world’s second largest economy, China. Overall, DJ Commodity Index dropped by 2.18% and Gold was down roughly half a percentage point.

Market Snapshot

News & Key Events in December

UK

• Annual inflation rate in the UK slowed to 3.9% in November 2023, the lowest since September 2021, from 4.6% in October.

• The Bank of England voted by a majority of 6-3 to uphold its benchmark interest rate at a 15-year high of 5.25% for the third consecutive time during its December meeting, aligning with policymakers’ efforts to combat inflation, even in the face of indications pointing to a deteriorating economic landscape.

• The British economy shrank 0.1% on quarter in Q3 2023, compared to initial estimates of a flat reading.

US

• The annual inflation rate in the US slowed to 3.1% in November 2023, the lowest reading in five months, from 3.2% in October.

• The Federal Reserve kept the fed funds rate steady at 5.25%-5.5% for a third consecutive meeting in December 2023, in line with expectations but indicated 75bps cuts in 2024. Policymakers said that recent indicators suggest economic growth has slowed, and job gains have moderated but remain strong, and unemployment rate has remained low.

• The US economy expanded an annualized 4.9% in the third quarter of 2023. This marks the strongest growth since Q4 2021.

Europe

• Annual inflation rate in the Euro Area decreased to 2.4% in November 2023, the lowest since July 2021, from 2.9% in October.

• The ECB maintained interest rates at multi-year highs for the second consecutive meeting in December and signalled an early conclusion to its last remaining bond purchase scheme, all as part of efforts to combat high inflation.

• The Eurozone economy contracted by 0.1% during the third quarter of 2023, marking a reversal from a downwardly revised 0.1% growth in the preceding three-month period.

China

• China’s consumer prices fell by 0.5% yoy in November 2023, steeper than a 0.2% drop in the prior month.

• The People’s Bank of China (PBoC) maintained its lending rates steady at the December fixing, as the central bank continued its attempt to revive a sputtering economy. The one-year loan prime rate (LPR), which is the medium-term lending facility used for corporate and household loans, was held unchanged at a record low of 3.45% for the fourth consecutive month; and the five-year rate, a reference for mortgages, was left at 4.2% for the sixth straight month.

• The Chinese economy grew by a seasonally adjusted 1.3% in Q3 of 2023. This was the fifth consecutive period of quarterly expansion, buoyed by a slew of monetary stimulus measures over the past three months, including interest rate cuts and constant liquidity injections by the country’s central bank.

Others

• The annual inflation rate in Japan dropped to 2.8% in November 2023 from 3.3% in the prior month, pointing to the lowest print since July 2022.

• The Bank of Japan (BoJ) maintained its key short-term interest rate at -0.1% and that of 10-year bond yields at around 0% in a final meeting of the year by unanimous vote, as widely expected.

• The annual inflation rate in Russia rose to 7.5% in November from 6.7% in the previous month, the highest since base effects from Russia’s invasion of Ukraine rolled over in February of 2023.

• The annual inflation rate in Canada was at 3.1% in November of 2023, remaining unchanged from the previous month and firmly above market expectations of 2.9%.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.