Overview

In April 2025, global financial markets were influenced by a combination of resilient economic data, rising inflation concerns, evolving tariff policies, and heightened geopolitical tensions. Resilient labour market and consumer spending figures in the US reinforced expectations that major central banks would maintain restrictive monetary policies for longer. Trade tensions between major economies, particularly involving the US and China concerning technology-related export restrictions, added pressure to global supply chains and manufacturing sectors. Energy markets remained sensitive to supply disruption fears amid ongoing geopolitical risks in Eastern Europe and the Middle East. Equity markets were supported by US-Iran ceasefire and strong AI driven tech sector. Overall, investor sentiment improved in April despite uncertainties around economic landscapes, inflation, trade, and geopolitical headwinds.

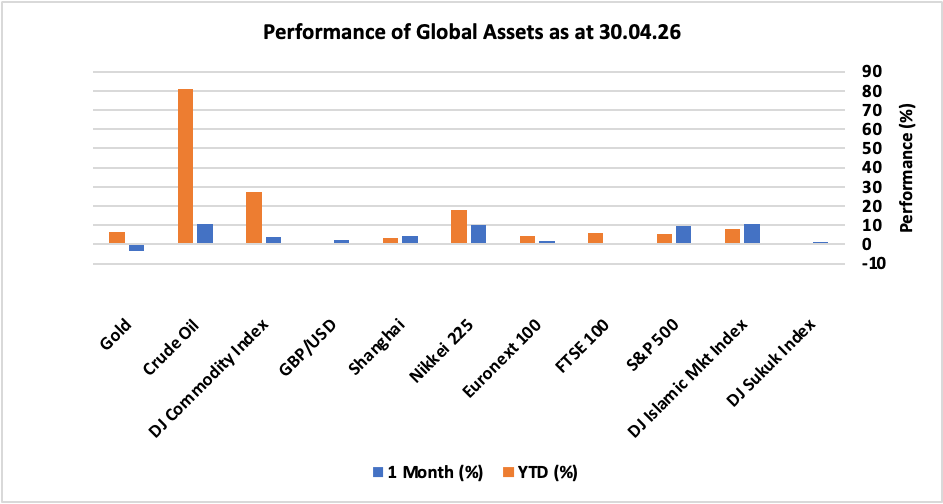

Looking at the performance, all major global financial assets, experienced strong recovery after a significant fall in prices in the previous month amid geopolitical fears resulting from War in Middle East. Resilient corporate earnings and positive developments in AI theme also contributed to the positive momentum. Equity markets delivered a strong positive performance as US S&P 500 climbed by 9.7% whereas DJ Islamic Markets Index booked positive 10.6% returns during the month. Asian equity markets also recorded significant gains as Japan’s Nikkei 225 led the momentum with mouth-watering returns of over 10.3% followed by China’s Shanghai index that surged 4.14%. While in Europe, EU Euronext 100 and UK FTSE 100 delivered positive 1.57% and 0.43%, respectively, falling short of global peers amid potential economic shocks impacted by rising energy costs and resulting inflationary pressures. DJ Sukuk Index ended the month up 1.39% amid softening pressure on yields. In commodities, DJ Commodity index climbed nearly 3.74% driven by over 10% surge in Crude oil prices, although gold fell by 3.3%. Lastly, UK pound appreciated 2.25% against US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in April 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in April:

UK

- The annual inflation rate in the UK rose to 3.3% in March 2026, up from 3% in each of the previous two months and in line with expectations. This marks the highest reading in three months.

- The Bank of England voted 8–1 to keep Bank Rate unchanged at 3.75% in April 2026, with one member preferring an increase to 4% and several policymakers indicating they could consider additional rate increases in the future. Policymakers highlighted that the conflict in the Middle East has created significant uncertainty for global energy prices.

- The British economy expanded 0.1% on quarter in the last three months of 2025, the same as in the previous quarter and in line with the preliminary estimate.

- The UK unemployment rate fell to 4.9% in the three months to February 2026, defying expectations of it remaining at the previous period’s 5.2%. The decline in unemployment coincided with a rise in economic inactivity, indicating that some Britons are leaving the workforce rather than finding new jobs.

US

- The annual inflation rate in the US jumped to 3.3% in March 2026, marking the highest level since May 2024 and a sharp increase from 2.4% in both February and January. Figures came in line with forecasts, with the rise primarily driven by higher energy costs, mostly gasoline and fuel oil, due to the war with Iran.

- The Fed kept the federal funds rate unchanged at the 3.5%–3.75% target range for a third consecutive meeting in April 2026, in line with expectations. The decision was not unanimous, with Governor Miran voting to lower interest rates by 25bps and three other members objecting the language in the statement that suggested the central bank would eventually resume cutting rates.

- The US economy expanded at an annualized rate of 2.0% in Q1 2026, up from 0.5% in the previous quarter but below market expectations of 2.3%, according to a preliminary estimate.

- The US unemployment rate fell to 4.3% in March 2026 from 4.4% in February, below market expectations of 4.4%.

Europe

- Euro area annual inflation climbed to 3% in April 2026, the highest since September 2023, up from 2.6% in March and slightly above market expectations of 2.9%, according to a preliminary estimate.

- The European Central Bank kept interest rates unchanged at its April meeting, with the main refinancing rate at 2.15% and the deposit facility at 2.0%, as policymakers adopted a cautious stance, assessing the impact of the Iran war on inflation and growth. While the ECB remains well-positioned to navigate uncertainty, officials noted that upside risks to inflation and downside risks to growth have intensified.

- The Eurozone GDP expanded by 0.1% from the previous quarter in the first quarter of 2026, missing the market consensus of a 0.2% expansion, and slowing from the 0.2% increase from the earlier period, according to the first preliminary estimate.

- The Euro Area seasonally adjusted unemployment rate eased to 6.2% in March 2026 from a revised 6.3% in February, in line with market expectations.

China

- China’s annual inflation eased to 1.0% in March 2026 from February’s over three-year high of 1.3%, falling short of market expectations of 1.2%.

- The People’s Bank of China maintained its key lending rates at record lows for an 11th straight month in April 2026, matching market expectations. The move reflected caution about the fallout from the war in the Middle East, even as domestic deflationary pressures ease, and early-year growth proves resilient.

- China’s GDP grew 1.3% qoq in Q1 2026, matching market expectations and following a 1.2% increase in Q4. The latest result marked the strongest quarterly expansion since Q4 of 2024, supported by continued policy backing from Beijing.

- China’s surveyed urban unemployment rate rose to 5.4% in March 2026 from 5.3% in the previous month and above market expectations of 5.2%. This marked the highest reading in thirteen months.

Others

- Japan’s annual inflation rose to 1.5% in March 2026 from February’s near four-year low of 1.3%, with transport costs posting the fastest increase in four months, amid the effects of the Middle East tensions. The Bank of Japan kept its short-term policy rate unchanged at 0.75% at its April 2026 meeting, leaving borrowing costs at their highest level since September 1995.

- The headline inflation rate in Canada surged to 2.4% in March of 2026 from 1.8% in the previous month, tying for the highest in one year but marginally below market expectations of 2.5%. The Bank of Canada left its overnight target rate steady at 2.25% in its April 2026 meeting, aligned with market expectations and its earlier guidance, and refrained from giving a clear direction on future rates due to the uncertain geopolitical backdrop.

- Russia’s headline annual inflation rate remained unchanged at 5.9% in March 2026 compared to February, slightly above forecasts of 5.8%. The Bank of Russia cut its policy rate by 50bps to 14.5% in its April 2026 decision, as expected by markets, and signalled that the cutting cycle is likely close to ending.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.