Overview

The month of April was volatile reflecting some of the headwinds mainly driven by uncertainty about the economy and the recent weak data stoking fears of a recession along with uncertainty about the impact of tighter bank lending and central bankers’ actions in coming months. The world economies and financial markets are continuing to face high uncertainties as inflation is still elevated and interest rates are increasing to counter high inflation.

The bond market is expecting a cut in interest rates towards the end of FY 2023 as bonds’ yields have decreased somewhat 50bps to 100bps, which helped bond prices recover. Bond prices increase when yields fall. The recent banking turmoil has weighed on the markets; however, the consensus view is that the banking system is on a far firmer footing than during the 2007-09 crisis and there is plenty of bad news already baked-in to share valuations. The stress in the market has reduced somehow and the financial markets appear to have embraced these developments. However, it is still very early to say anything about the health of the financial markets as monetary tightening cycle is expected to continue for the near future resulting in credit tightening to fight inflation.

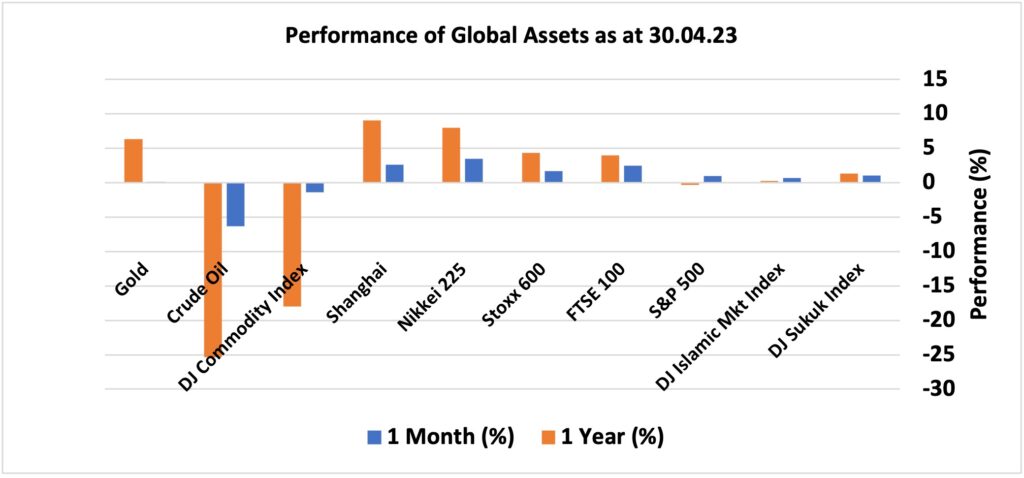

Reflecting falling yields, DJ Sukuk Index returned 1%; however, emerging and Asian equity markets had been the best performing assets in April. Among equity markets, Japan’ Nikkei 225 surged 3.44%, China’s Shanghai index appreciated by 2.57%, Europe’s Stoxx 600 climbed 1.68%, and the UK’s FTSE 100 index retuned 2.48% during the period. The US broad equity benchmark S&P 500 increased just under 1% while DJ Islamic market index returned only 0.67% in April. Commodities were the worst performers among major asset classes as oil continued to fall despite OPEC’s surprise decision at the start of April to cut production. Crude oil plunged above 6% while DJ Commodity index dropped 1.44% during April. Gold remained largely flat with only 0.07% upside.

Market Snapshot

News & Key Events in April

UK

• The consumer price inflation rate in the UK eased to 10.1% year-on-year in March 2023, down from 10.4% in February but more than market expectations of 9.8%. The inflation rate remained above 10% mark for the seventh consecutive period and the Bank of England’s 2% target for almost two years.

• The UK economy expanded slightly by 0.1% on quarter in the final three months of 2022, following a 0.1% contraction in the previous period.

US

• The annual inflation rate in the US slowed for a ninth consecutive period to 5% in March of 2023, the lowest since May of 2021 from 6% in February, and below market forecasts of 5.2%.

• The US economy grew by an annualised 1.1% in Q1 2023, slowing from a 2.6% expansion in the previous quarter and missing market expectations of a 2% growth.

Europe

• The consumer price inflation rate in the Euro Area slightly increased to 7% in April 2023, from March’s 13-month low of 6.9%.

• The Eurozone economy grew slightly by 0.1% in the first quarter of 2023 after a flat fourth quarter, but missed market consensus of a 0.2% expansion.

• Germany’s consumer price inflation eased to 7.2% year-on-year in April 2023, down from 7.4% the month before and slightly below market expectations of 7.3%.

• Germany’s GDP was unchanged in the first quarter of 2023, following a 0.5% contraction in the previous three-month period and missing market expectations of a 0.2% expansion.

China

• The People’s Bank of China (PBoC) left its key lending rates steady for the eighth straight month at April fixing, as the economic recovery has returned on track after the withdrawal of most anti-COVID measures last December.

• China’s annual inflation rate unexpectedly came in at 0.7% in March 2023, compared with February’s print and market consensus of 1%.

• The Chinese economy grew by 2.2% on a seasonally adjusted basis in the three months to March of 2023, picking up from an upwardly revised 0.6% growth in the fourth quarter.

Others

• The annual inflation rate in Japan came down to 3.2% in March 2023 from 3.3% in the previous period.

• Russia’s GDP fell by 2.7% year-on-year in the fourth quarter of 2022, after a downwardly revised 3.5% decline in the previous three-month period and compared with market forecasts of a 7% slump.

• The annual inflation rate in Australia dropped to 7% in Q1 of 2023 from an over-30-year high of 7.8% in the previous period, compared with market forecasts of 6.9%.

• The annual inflation rate in Canada fell to 4.3% in March of 2023, the lowest since August 2021, in line with market expectations and dropping from 5.2% in the previous month amid significant base-year effects for energy costs.

Disclaimer

Data as of 30 April 2023. This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.