Gold has occupied a unique position in financial markets for centuries. Unlike equities or fixed income assets, it does not generate income, pay dividends, or produce cash flow. Yet investors continue to hold it during periods of economic uncertainty, inflation concerns, geopolitical tension, and market stress. In recent years, gold has once again demonstrated why many investors still consider it an important portfolio diversifier, particularly in uncertain macroeconomic environments. For ethical investors, the debate around gold is not simply about returns, but also about stability, diversification, resilience, and responsible portfolio construction.

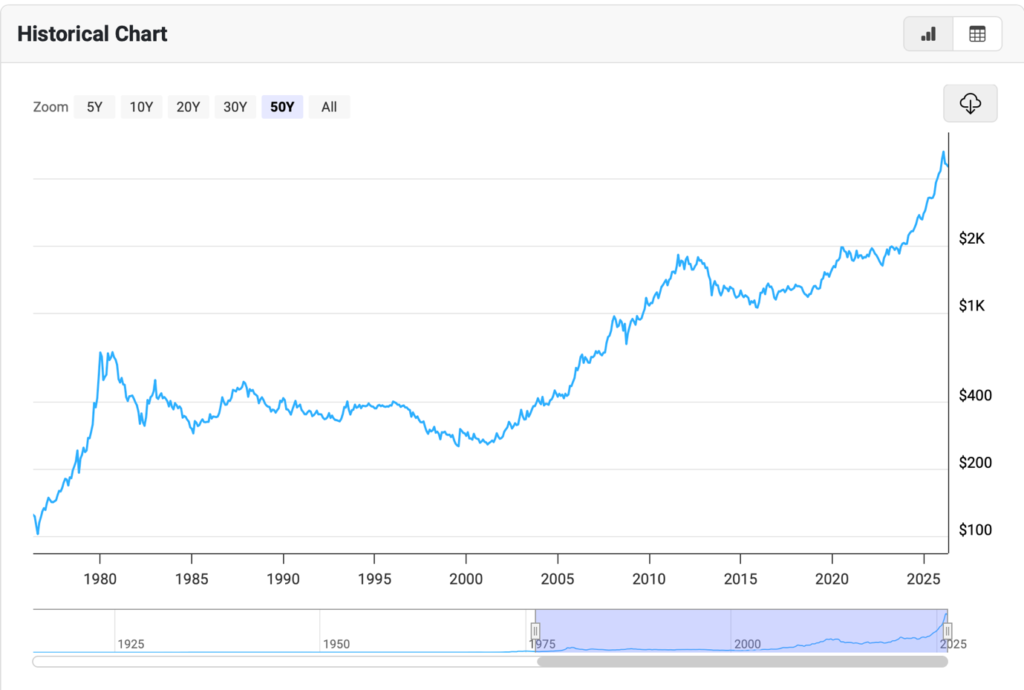

The recent surge in gold prices has reignited discussion about whether the precious metal still deserves a place in long-term portfolios. Gold has experienced significant volatility over the past year, with sharp rallies followed by notable pullbacks. However, such price swings are not unusual in major gold bull markets. Historical trends from previous cycles, particularly during the 1970s and the early 2000s, show that gold often experiences temporary corrections even within broader long-term upward trends.

Source: Macrotrends

Gold’s role as a diversifier

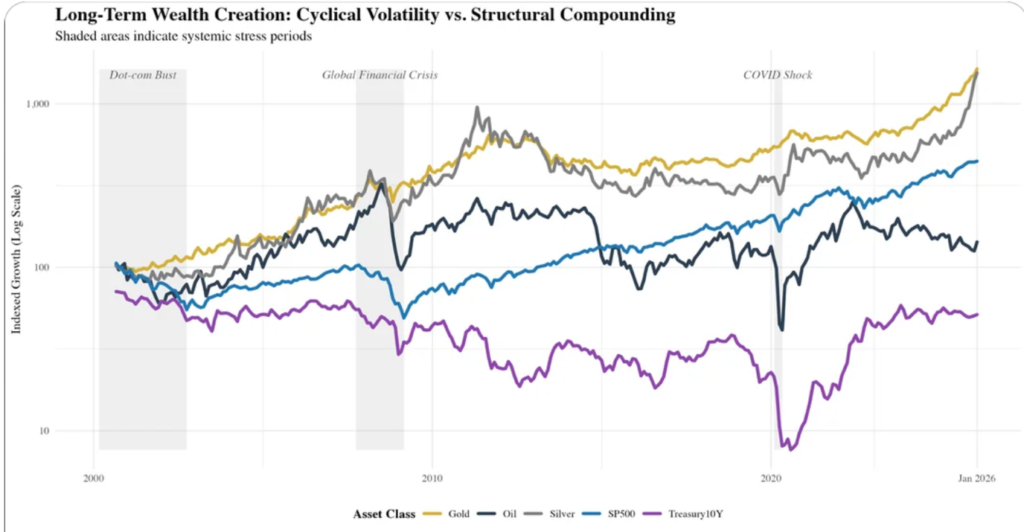

One of the strongest arguments for holding gold in ethical portfolios is its role as a diversifier. Traditional investment portfolios are heavily weighted toward equities and fixed income securities. During periods of market stress, these assets can sometimes become highly correlated, reducing the effectiveness of diversification. Gold has historically behaved differently from many conventional financial assets, particularly during inflationary periods or geopolitical crises. This characteristic can help reduce overall portfolio volatility and provide a degree of protection during difficult market conditions.

Source: reddit

The modern investment landscape has strengthened the case for diversification through alternative assets. Investors today face a range of macroeconomic challenges including elevated sovereign debt levels, persistent inflation concerns, geopolitical instability, and questions surrounding the long-term purchasing power of fiat currencies. These conditions have contributed to renewed interest in gold as a defensive asset. Supporters of gold argue that governments may increasingly rely on inflation and monetary expansion to manage large debt burdens, potentially weakening currencies over time. In such an environment, gold is often viewed as a store of value and a hedge against monetary debasement.

Why gold in ethical portfolios?

For ethical investors specifically, gold can serve an important risk-management role without requiring exposure to sectors that may conflict with ethical or faith-based principles. Many ethical portfolios avoid highly leveraged businesses, speculative industries, gambling, alcohol, tobacco, weapons manufacturers, or companies with poor environmental or social practices. Gold, particularly when accessed through responsibly sourced bullion or carefully screened investment vehicles, can provide exposure to a non-correlated asset without directly relying on such sectors.

That said, the ethical case for gold is not entirely straightforward. Critics argue that gold itself produces no economic output and generates no income. Unlike shares in productive businesses, gold relies primarily on price appreciation for returns. Sceptics also point out that holding physical gold carries storage costs and opportunity costs, especially when interest rates are high and cash savings offer attractive yields. Warren Buffett has famously criticised gold for these reasons, viewing productive businesses as superior long-term wealth creators.

There are also broader ethical considerations linked to mining practices. Gold extraction can involve environmental damage, water pollution, poor labour standards, and unsafe working conditions in certain parts of the world. As a result, ethical investors need to approach gold carefully and selectively. Responsible sourcing, transparency in supply chains, and exposure through regulated and sustainable investment products become particularly important. Investors seeking alignment with ethical or Shariah-compliant principles may therefore prefer physically backed products with strong governance standards or mining companies demonstrating robust environmental and social practices.

Despite these concerns, gold’s appeal has remained resilient because of its ability to preserve purchasing power during uncertain periods. Analysts often examine gold not through conventional valuation metrics such as earnings or cash flow, but through relative purchasing power comparisons. One approach compares gold prices to household disposable income, while another looks at how many ounces of gold are required to purchase a typical home. These measures attempt to assess whether gold appears historically expensive or inexpensive relative to broader economic conditions.

Another key factor supporting gold has been central bank demand and investor concern over the sustainability of government debt levels. In periods where confidence in monetary policy weakens or inflation expectations rise, gold often attracts renewed investor interest. Geopolitical tensions have further strengthened demand for perceived safe-haven assets. Even when gold prices experience temporary declines, underlying macroeconomic concerns frequently remain unresolved, which helps explain why many long-term investors continue to maintain allocations to precious metals.

However, investors should also recognise that gold is not immune to volatility. Recent years have shown that even safe-haven assets can experience sharp short-term corrections. Gold prices can be influenced by movements in interest rates, the strength of the US dollar, investor sentiment, and futures market positioning. At times, gold may even fall during geopolitical crises if rising interest rates or a stronger dollar outweigh safe-haven demand. This complexity highlights why gold should generally be viewed as a complementary asset rather than a standalone investment strategy.

For ethical portfolios, the most sensible role for gold is often as a modest strategic allocation rather than a dominant holding. A carefully measured exposure can enhance diversification, improve resilience during periods of stress, and provide protection against inflationary or monetary risks. At the same time, maintaining balance remains essential, as long-term portfolio growth is still primarily driven by productive assets such as equities, businesses, and real economic activity.

Ultimately, gold’s enduring appeal lies less in speculation and more in its historical role as financial insurance. Ethical investing is not only about aligning investments with values; it is also about building sustainable and resilient portfolios capable of navigating uncertainty. In that context, gold may continue to play a valuable supporting role alongside equities, sukuk, ethical funds, and other long-term investment assets. While it may never replace productive investments, its ability to provide diversification and stability during turbulent periods ensures that gold remains relevant in modern ethical portfolio construction.

Looking for Financial Advice?

Simply Ethical manages investment portfolios comprising Shariah-compliant Funds, ETFs, and direct Equities or Stocks, providing clients with diversified and ethically aligned investment solutions. Each portfolio is carefully designed to reflect varying risk appetites, return objectives, and long-term financial goals while adhering to Islamic investment principles. You can explore different investment portfolios here (including Personal Pensions, ISAs, and General Investment Accounts) that best describes your risk/return profile and investment objectives.

To learn more about how we can help you and our investment approach, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.