People work hard to earn money to provide them and their family with a good lifestyle. In general, most individuals tend to save a portion of their earnings for emergency funds, kids’ education, housing, holidays and/or retirement. Savings can be utilised for different purposes depending on individual’s objectives, risk profile and the time horizon. One may place funds in a bank account or simply invest in various investment solutions available out there in the capital markets. Investment activities provide a unique way where money works for you to build wealth over time through earnings on invested funds. Compounding is a powerful tool in investing where income from investments is re-invested to earn greater return over the years.

Investing is a good way of building wealth over time to become financially better off, however, there are countless examples out there where people started with little savings but remained steady in their investing habits and became rich. For example, Warren Buffett (who is now over 90 years old) is considered a great investor of our time. He started investing at the age of 13 and is now in the top 10 of the richest people in the world. Even if your ultimate goal is not to become rich, still investing provides a way to enhance your financial well-being.

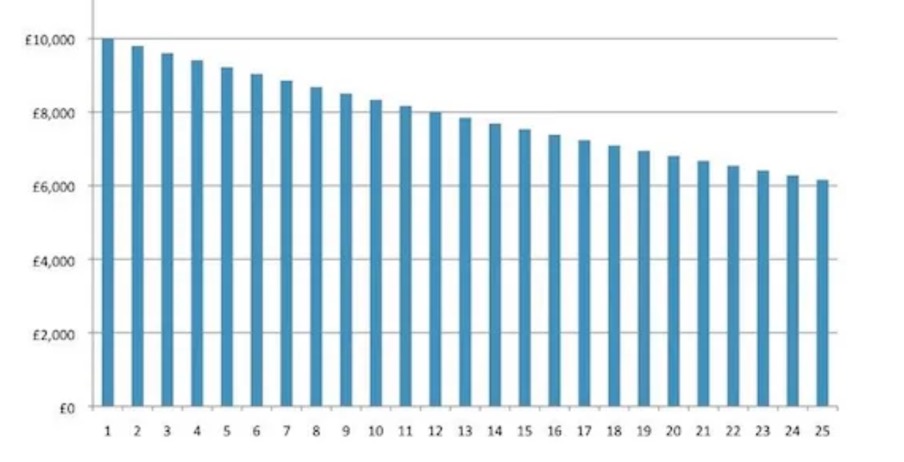

The world has seen multi-decade high inflation, currently, over 8% in the UK and around 5% in the US. The savings simply left in bank accounts would have lost its real value. Figure 1 below demonstrates how inflation eats up your savings (this graph assumes pre-covid 2% inflation, but think about today’s inflation – 8%+ in the UK, can you imagine how rapidly purchasing power of your money has diminished and is still diminishing?). The key message from this graph is that the longer you hold your savings as cash earning no return, the lower would be the end value of the funds, on inflation-adjusted basis.

Figure 1: Loss of purchasing power over time (assuming 2% inflation)

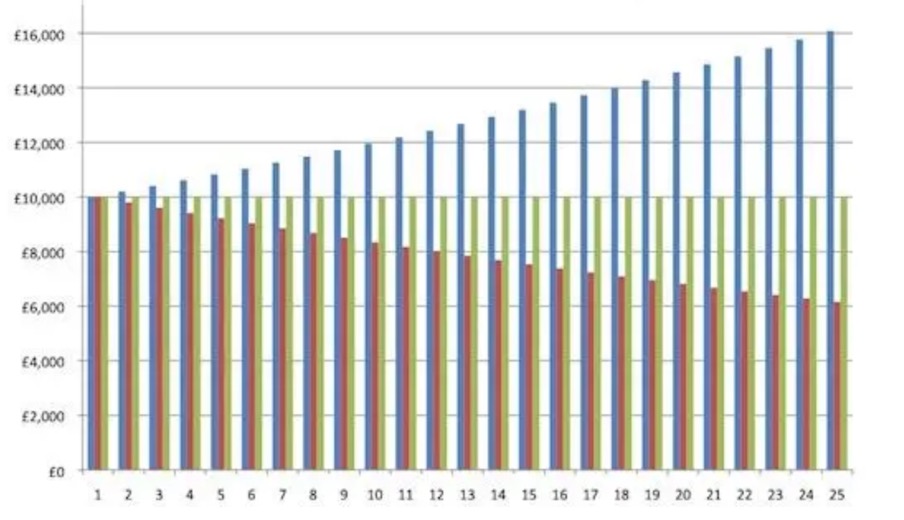

Figure 2 below shows, in addition to the impact of inflation on savings (red bars), the growth of savings if they are put in a 2% return earning account (blue bars). The longer you hold your savings in the return earning account, the higher would be the end value of the funds, on nominal terms. However, the impact of 2% inflation will cancel out this growth in funds so the real impact would be the net-net basis (indicated by green bars), ignoring other factors to keep things simple/understandable. This way, you are not growing your wealth. This further reinforces the need to invest your savings in investment assets that offer higher returns, at least due to two reasons. 1) you want to grow your investment funds, 2) the inflation is much higher than the rates you can get from saving accounts offered by the banks and other similar saving schemes.

Figure 2: The impact of 2% inflation and 2% return on your savings.

Investing helps build wealth over time by beating inflation with a considerable margin. However, different asset classes offer different risk-return profiles, and it totally depends on the individual investor’s preferences and circumstances. Your investment objectives, risk profile and other key investment constraints (time horizon, liquidity needs, tax concerns, legal and regulatory factors, unique circumstances, etc.) will determine what is appropriate for you.

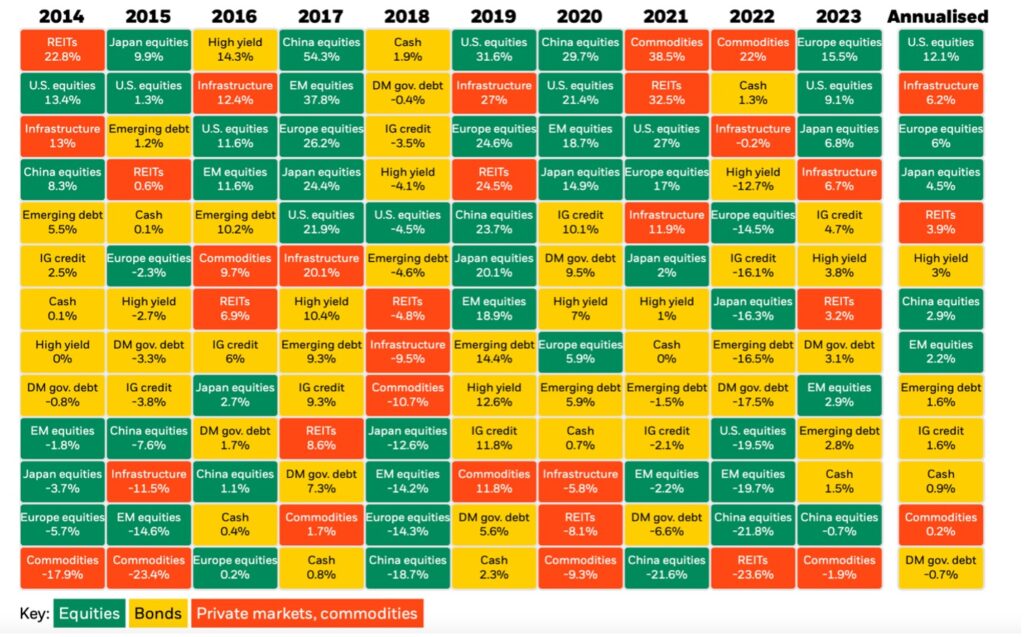

Although equities offer the best returns over the long-term, however, they bear more risk and are highly volatile over the short term. On the other hand, bonds or sukuks are less risky (remember, they are not risk-free), therefore, offer lower returns compared to equities, as highlighted in figure 3 below. Over the last 10 years, US equities provided 12.1% annualised average returns whereas bonds of different categories provided less attractive returns. Alternative investments (real estate, commodities, metals, infrastructure, etc.) also provide decent returns and are good portfolio diversifiers. A balanced portfolio may be a good solution for many investors who are risk-conscious whereas a growth portfolio investing mainly in equities are for those who possess profiles of enterprising investors.

Figure 3: Investment asset classes’ returns compared.

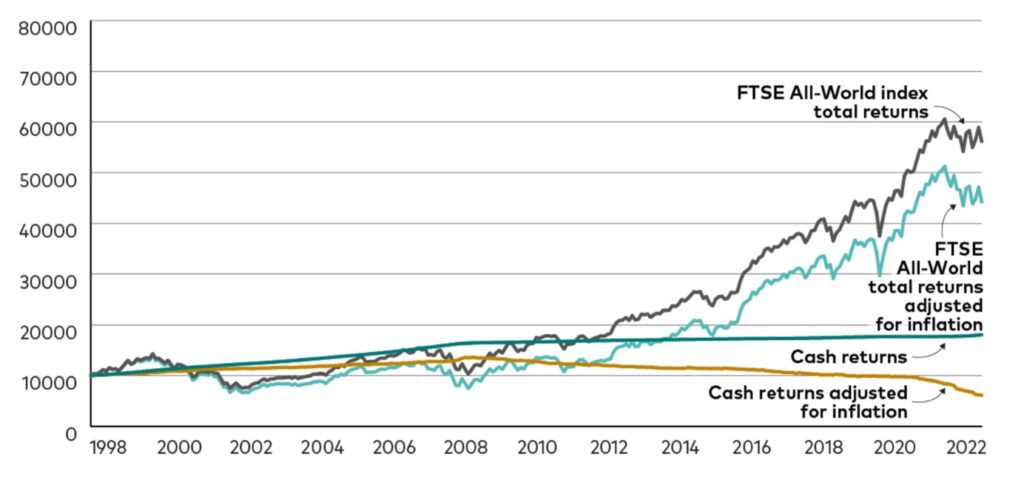

During 1998 to 2022, cash generated negative real returns. Figure 4 below shows a comparison of cash returns with equities’ returns, both on nominal and real (inflation-adjusted) basis. $10,000 invested in cash (interest-bearing bank accounts) in 1998 increased to about $18,000 in 2022 in nominal terms, however, decreased to about $6,000 in real terms. That is actually a loss, through the loss of purchasing power of money (inflation). On the other hand, the same $10,000 invested in equities (stocks) increased to almost $56,000 in nominal terms and about $45,000 in real terms. Therefore, equities are mostly the best choice out there in the capital markets. However, the required investment time horizon is fairly long enough to ride-off extreme market volatilities.

Figure 4: Cash returns vs Equity returns (nominal and real)

One statement nicely concludes this article: “Investing is NOT risky, not investing is”. This is true when you have a long-term view. Remember, do not forget the hard reality – inflation – the killer of purchasing power of money.

To learn more about how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.