Financial markets ended 2023 on a positive note albeit being highly volatile and unpredictable. Now, it is the start of a new year, 2024, with fresh hopes and interesting predictions. In this article, we will review the key highlights of 2023 and try to understand how we can navigate through 2024 with the lessons learnt from the previous year.

• The year that proved most economists wrong

Broadly speaking, the consensus forecast for 2023 was that it will be another wicked year for financial markets because of very high inflation rates, ultra-high-speed increase in interest rates, wars, banking turmoil, and expectations for a deep recession. However, 2023 was recorded as one of the best years for markets. This reminds us that the future is uncertain and unpredictable. It also reinforces that being in the market with the right allocation is the way to go.

• Geo-political conflicts

Regional wars have been the top stories throughout the year. Russia-Ukraine war continued during the year 2023 with no significant progress to end this war. Later in the year, the conflict in Palestine emerged that put the whole Middle East region at risk. The conflict triggered wide-spread protests around the world against the war. Around 24,500 Palestinians have now been killed in Israeli attacks, with more than 61,500 injured. Millions more displaced people are living through what UN experts said is an “unfolding genocide,” warning that “Gazans now make up 80% of all people facing famine or catastrophic hunger worldwide.” This death and destruction inflicted on Gaza by Israel since October 7 is precisely what South Africa has asked the International Court of Justice (ICJ) to stop, putting in a special emergency request for provisional measures to halt Israeli aggression. Meanwhile, diplomacy continues in the background but to no avail.

• UK politics and year of strikes

In London, politics remained in the headlines where Prime Minister Rishi Sunak struggled to re-establish a sense of stability after a dramatic 2022, which saw his forerunners Boris Johnson and Liz Truss expelled from the office by their own MPs. Then in January, his party chairman Nadhim Zahawi was forced to resign for not declaring that HMRC was inspecting his tax matters on becoming Mr Johnson’s chancellor last year. Meanwhile, the cost of living crisis squeezed household finances amid high interest rates and sluggish GDP growth that put the nurses, ambulance workers and train drivers on strikes at the start of the year then teachers joined them for industrial action later in January. However, there was some relief towards the end of year as inflation continued to fall from 10.1% at the start of year to 4% in December.

• US banking crisis

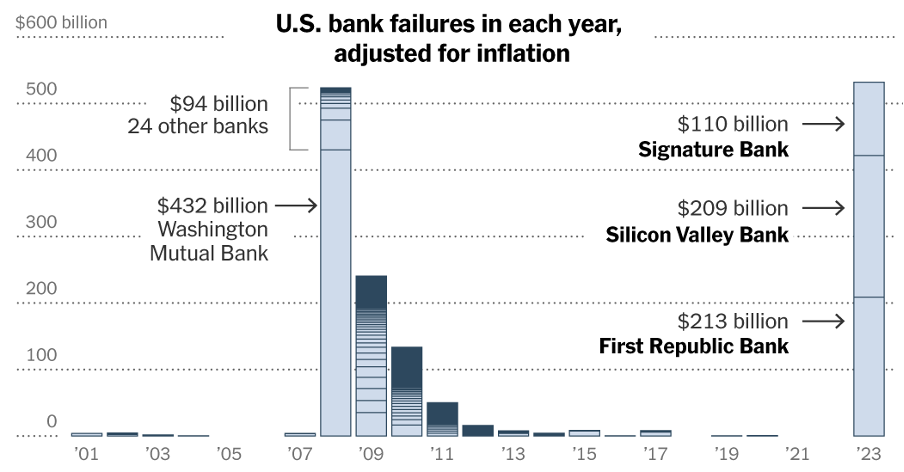

In march, the news from the US banking sector came to fore when a number of banks failed. The first bank to fail was cryptocurrency focused Silvergate Bank as it announced to wind down on March 8, 2023 due to losses suffered in its loan portfolio. Silvergate was hit with a bank run in the wake of the bankruptcy of FTX; deposits from cryptocurrency-related firms dropped by 68% at the bank. Two days later, upon announcement of an attempt to raise capital, a bank run occurred at Silicon Valley Bank (SVB), causing it to collapse. SVB was the 16th largest US bank and was known as the banker for Venture Capitalists (VC funds) and technology start-ups. SVB failed when a bank run was triggered after it sold its treasury bond portfolio at a large loss, causing depositor concerns about the bank’s liquidity. The bonds had lost significant value as market interest rates rose after the bank had shifted its portfolio to longer-maturity bonds. Signature Bank, a bank that frequently did business with cryptocurrency firms, was closed by regulators two days later on March 12, with regulators citing systematic risks.

Largest US bank failures

Soon after the bank run at SVB, depositors quickly began withdrawing cash from First Republic Bank (FRB), which focused on wealthy clients. Like SVB, FRB had substantial uninsured deposits exceeding $250,000; such deposits constituted 68% of the bank’s total at year-end 2022, declining to 27% by the end of March, as $100 billion in uninsured deposits were withdrawn. On May 1, the Federal Deposit Insurance Corporation (FDIC) announced that First Republic had been closed and sold to JP Morgan Chase. The collapse of First Republic Bank, Silicon Valley Bank and Signature Bank were the second, third and fourth largest in the history of US, respectively, smaller only than the collapse of Washington Mutual during 2007-08 financial crisis. To prevent the situation from affecting more banks, global industry regulators, including the Federal Reserve, Bank of Japan, Bank of Canada, the Bank of England, ECB and Swiss National Bank intervened to provide extraordinary liquidity.

• US debt ceiling and downgrade

In second quarter, we saw debates over raising the debt ceiling from all sides. Republicans had refused to raise the country’s borrowing limit unless Democrats agreed to cut spending, leading to a standoff that was not resolved until weeks of intense negotiations between the White House and House Speaker Kevin McCarthy. The final agreement, passed by the House on Wednesday, 31st May and the Senate on Thursday, 1st June suspended the debt limit until 2025 – after the next presidential election – and restricted government spending. It gives lawmakers budget targets for the next two years in hopes of assuring fiscal stability. On 3rd June, President Biden signed into law bipartisan legislation that suspends the $31.4 trillion debt ceiling, narrowly avoiding an unprecedented U.S. default that could have pushed the economy into a recession and financial crisis. Historically, the debt ceiling has been raised every time the US borrowings reached to that level. Congress has always acted when called upon to raise the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognised that this is necessary.

In August, Fitch Ratings downgraded the US Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘AA+’ from ‘AAA’. According to Fitch, the rating downgrade of the US reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden. In Fitch’s view, there has been a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters, notwithstanding the June bipartisan agreement to suspend the debt limit until January 2025. The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management. Even after the downgrade, the US once again averted a government shutdown after a bill ensuring funding until November 17th was signed into law by President Joe Biden minutes before October 1st deadline. While the US federal debt has risen faster in recent years, higher interest rates pose the added challenge of sharply higher annual interest payments. However, when rates begin to ease, this will relieve some pressure, but mounting government debt remains a broader-term risk.

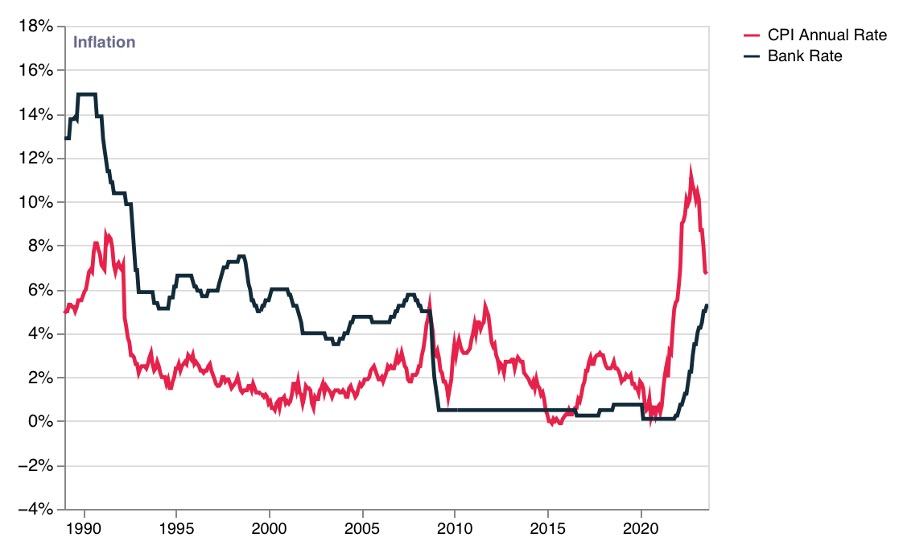

• High interest rates but moderating inflation

Throughout the year the interest rates kept ticking up at a historic high speed to bring inflation down to central banks target level. The US Fed increased rates to 5.25%-5.50% last time in July 2023, significantly up from 4.25%-4.5% at the start of the year, making this tightening cycle, which now appears to be over, the fastest in four decades. This monetary tightening cycle helped the Fed to bring inflation down from 6.4% at the start of the year to 3.1% in November 2023. Following similar path, the European Central Bank (ECB) increased rates to 4.5% in September 2023 from 2.5% at the start of 2023. The ECB successfully reduced inflation from 8.6% to 2.9% in 2023. Meanwhile, the Bank of England (BoE) raised interest rates to 5.25% in its August 2023 meeting. The move brings the main cost of borrowing for commercial banks in the UK to 5.25%, which is the highest level since February 2008. BoE’s monetary tightening moves reduced inflation significantly from 10.1% at the start of 2023 to 3.9% in November 2023. Resembling with the US Fed and ECB, the BoE hinted that it may be about to pause its rate hikes. Now, the consensus is shifting towards monetary easing cycle starting from 2024 onwards.

UK inflation and interest rates 1989-2023

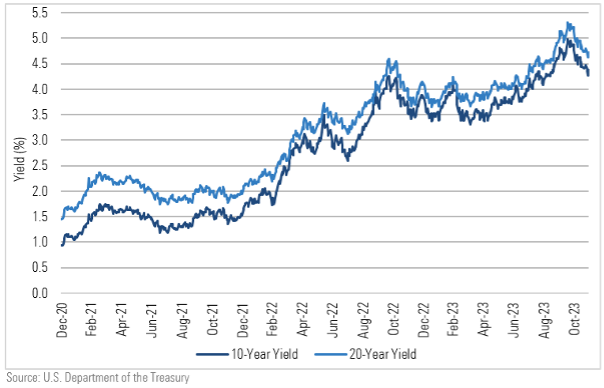

• Falling bond yields relieved fixed income investors

One of the fastest moving rate hike cycles in the recent history posed a challenge for fixed income investors. Bonds yields went up significantly (near 5% level) that resulted in a drop in bond values. Bond values fall when yields rise and vice versa. However, when central banks signalled in the latter half of the year that interest rates are at their peak levels and they might start cutting rates next year, bonds yields started falling sharply from 5% towards 4% in a matter of weeks. This reversal in yields helped bonds values to start recovering. Many asset managers preferred to lock-in the high yield for years to come to boost portfolio returns through high yields and capital gains in the falling rates environment in the years to come.

10-Year and 20-Year Treasury yields

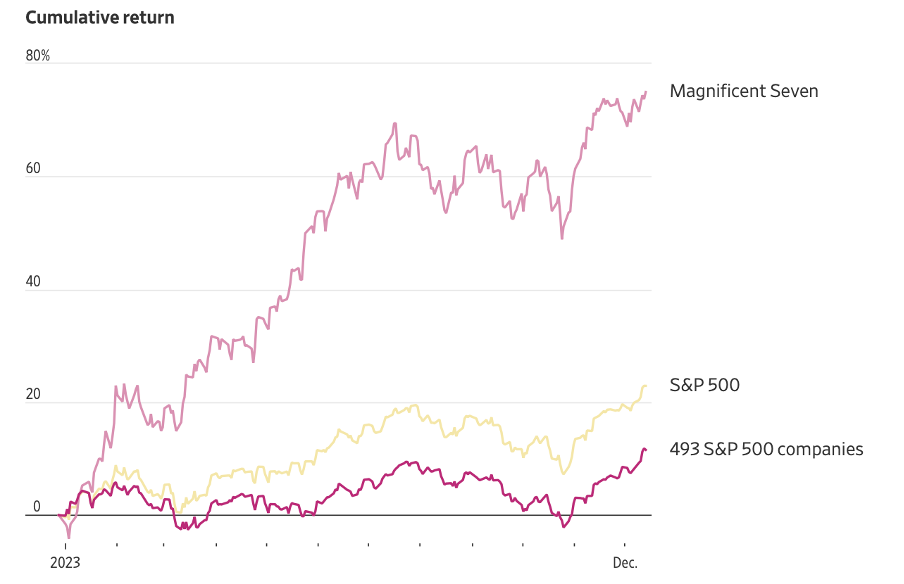

• Markets amused investors – AI driven boom boosted the ‘Big 7’

Looking at the performance of major asset classes in 2023, equity markets rebounded strongly after devastating performance in 2022. Most of the performance of equity markets in 2023 was driven by enthusiasm over development around artificial intelligence (AI) that helped big technology stocks, magnificent 7 companies (Apple, Amazon, Alphabet Inc. (Google), Meta Platforms, Microsoft, NVIDIA and Tesla), to book over 70% return collectively. Moreover, the highly anticipated recession did not happen, economies proved to be resilient, falling inflation levels in all major economies and the signals from central banks that interest rates might have peaked. All these factors pushed asset prices higher, and equities took the lead.

Performance of Magnificent 7 stocks and S&P 500 index 2023

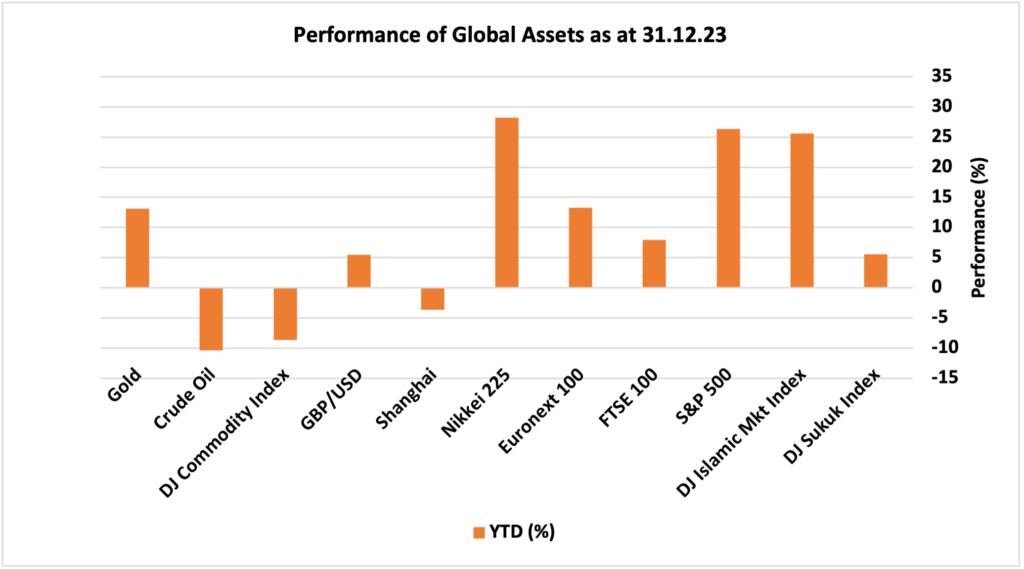

Equity markets booked 2023 as one of the best performing years in the equity markets recent history. Nikkei 225 index was the leader with 28.24% annual return followed by US S&P 500 index and DJ Islamic markets index with 26.3% and 25.6%, respectively. Europe’s Euronext 100 got the next spot with 13.3% return in 2023. UK FTSE recorded 7.93% upside while China’s Shanghai Index fell 3.7% as concerns of deflation and troubling property sector despite Beijing’s efforts to stimulate the economy through monetary easing kept the investors sentiment down.

The next best asset class in terms of performance was the fixed income where DJ Sukuk Index returned 5.53% amid expectations that rates might have peaked and then later in the year falling yields as market consensus shifted towards interest rates cut in the first half of 2024. Commodities remained under pressure where crude oil fell over 10% amid concerns over slowing global economy after historic speed of rates hike and struggling world’s second largest economy. Overall, DJ Commodity Index dropped by 8.67% while Gold booked 13.1% upside, proving as a go-to-asset-class when things become more uncertain. UK pound appreciated against US dollar by 5.5% in 2023 after a dramatic drop in late 2022 as markets had become disenchanted with the new administration under the newly appointed prime minister, Liz Truss, who motioned an expansive economic policy based on wide-ranging tax cuts.

Global assets performance 2023

You can book a free consultation with one of our Financial Advisers to learn more about our investment approach and how we can help you.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.