2022 has been a difficult year for investors as all major asset classes posted negative returns (except energy). The performance of assets in 2023 will mainly depend on how macroeconomic conditions evolve and its impact on individuals, businesses, governments and the broader financial system.

The UK and Europe are more likely to see a recession in 2023 while US could possibly avoid a deep recession depending on the Fed’s monetary tightening stance and whether they end up with ‘soft’ or ‘hard’ landing. The current narrative is ‘bad news is good’ as the Fed is fighting to bring the inflation back to their 2% target level. However, the potential risk is the narrative could change to ‘bad news is bad’ in 2023, where high interest rates, recession, significant contraction in corporate profitability, and high unemployment could lead financial markets to a further slump.

The situation in Japan is completely different as they have witnessed inflation creeping up, but interest rate still remains low at -0.1%. However, the Bank of Japan shocked markets on December 20th by increasing the upper limit of its tolerance band on 10-year government bonds to 0.5% from 0.25%, raising speculation of a shift in monetary policy from April when Governor Haruhiko Kuroda will retire. A change in monetary shift will be important to watch out, given its government debt levels. China is an interesting case as it is the second largest economy and a key player in global supply chain, however, it is still struggling with covid-19 lockdowns. Any positive news in China will be welcomed globally and vice versa.

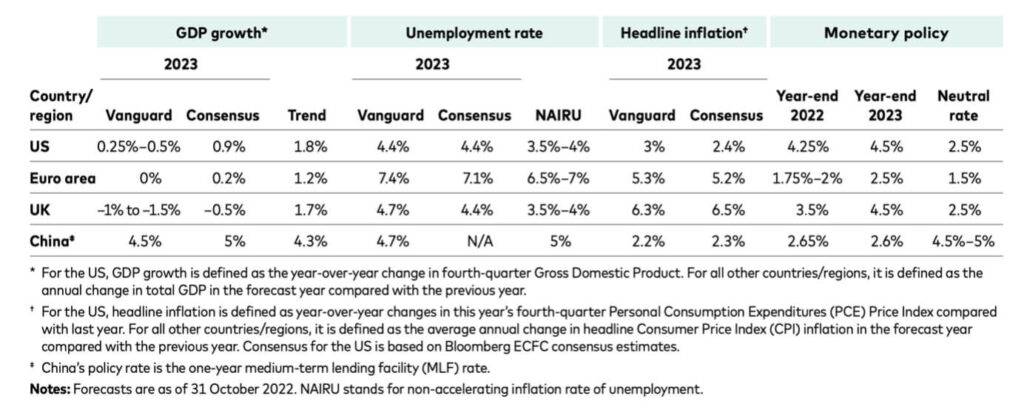

The table below shows macroeconomic forecasts for 2023 where inflation will follow a downtrend, however, it is expected to remain higher than the target level. As per the consensus forecasts, 2023 will end up with 5%+ inflation in EU and UK but will come down to less than 3% in the US. This inflationary pressure will keep the interest rates at elevated levels in 2023, which is not a positive news for the markets.

The key factors that may keep inflation high include Russia-Ukraine war and global supply chain disruptions that could push the energy and commodity prices at high levels. According to Deloitte, “the crystal ball for the global economy is murky. No matter when and how the war in Ukraine ends, the ramifications for energy production, global trade, capital flows, cross-border payments, and supply chain finance are expected to be enormous. These dynamics will likely affect how and what banks do to collectively support and engage with economic agents globally”. Interest rate is a tool that central banks use to control money supply and employment, therefore, expect the rates to remain high until inflation is under control.

Click here to learn how to invest during periods of high inflation.

Economic growth and likelihood of a US recession

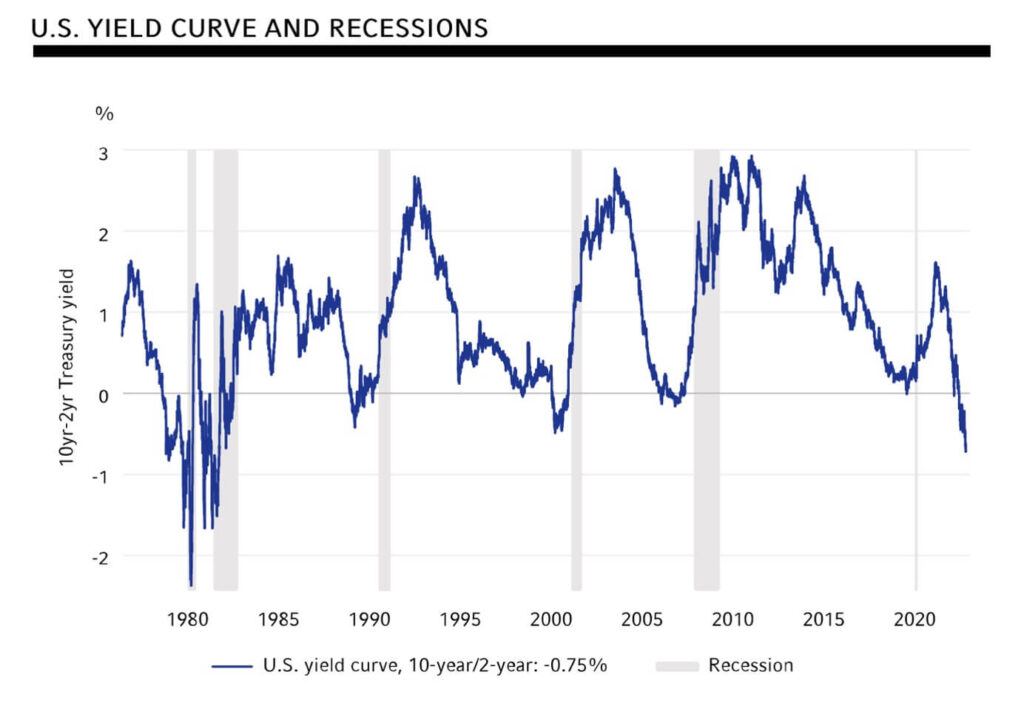

Economic growth is forecasted to remain low (significantly below the trend) as a result of high interest rates. The risk of potential recession is high, and the extent of recession is difficult to estimate as macro environment is highly uncertain. Yield curve is commonly used as a tool to forecast recessions. Yield curves are inverted (when interest rates on long-term bonds fall lower than those of short-term bonds), a fact that requires attention. Yield curves are not very good at predicting when a slowdown occurs, only that it will occur at some point in the future. Historically, when yield curve becomes inverted (short-term rates higher than long-term rates), recession follows in the next 12-18 months. As at 30th Dec 2022, the 2y year US note yields around 4.42%, whilst the 10yr yields around 3.87% as demonstrated in the graph below.

In other words, when yield spread (10y treasury yield – 2y treasury yield) is negative as shown in graph below, recession follows between 1-2 years. The current yield curve is inverted, and yield spread is negative (see graph below) that indicates the recession is possibly on the horizon.

Watch out for the banking sector – Correlation between economic growth and banking sector

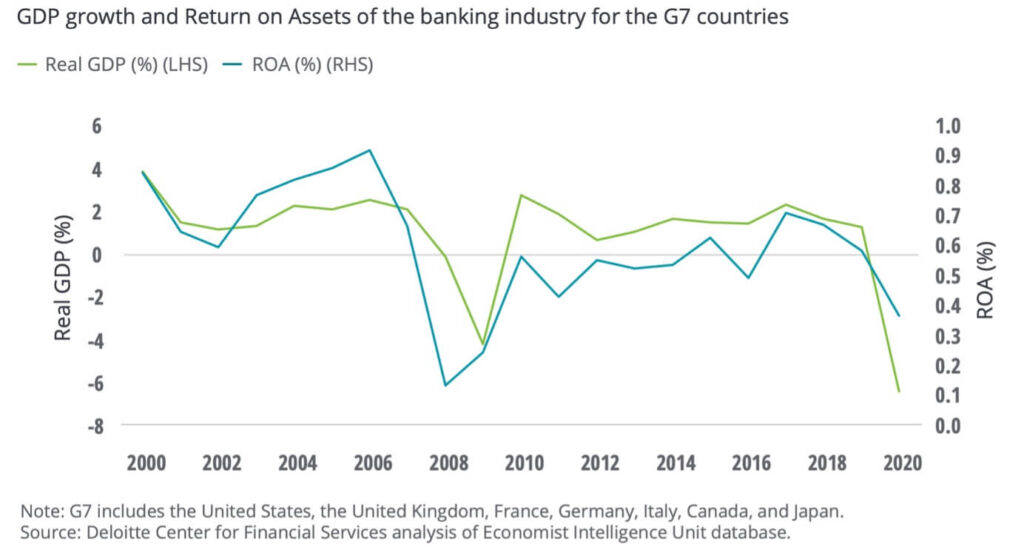

Banking sector is, no doubt, the engine of economic machine. Every sector of the economy is directly or indirectly linked with banking system. Banks act as an intermediary to provide capital to businesses and households among other activities. Slow economic growth or a deep recession can adversely impact banks performance – this could be a red signal for the financial system that eventually impacts the wider economy. This strong positive correlation between economic growth and banks profitability in G7 countries is clearly depicted in the chart below.

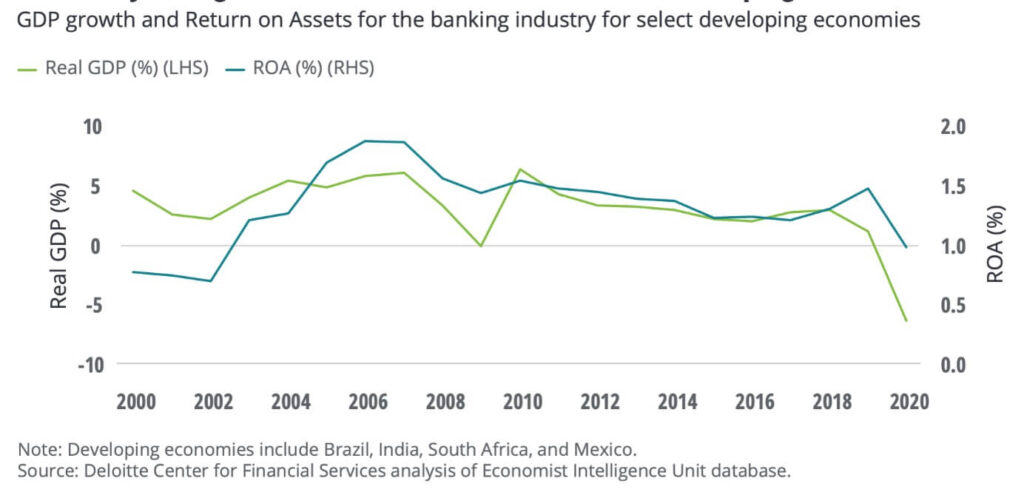

It is worth noting that this relationship is not just a phenomenon of developed economies, but a very similar correlation can also be observed in developing economies as highlighted in the chart below. So, any upcoming recession could have adverse impact on the banking sector and ultimately on the financial stability if recession gets deeper.

TINA to TARA, what are the prospects

The traditional 60/40 portfolio (60% equity, 40% bonds) has been a preferred choice in the last decade, which is sometimes referred as ‘TINA – there is no alternative’. Interest rates were low, equities were booming, especially US equities, and there were choices for yield seekers in fixed income investment. The next decade may be different as interest rates are high and equity markets outlook is not very promising, at least for the near term. Now the term ‘TARA – there are reasonable alternatives’ is becoming more relevant. As rates are high, bonds could offer good returns in coming years. Although, US equities outlook is dim due to recession fears, however, international equities including EU, Japan, China, and other emerging markets seem to offer better risk-reward trade-offs as their valuations are relatively more attractive than US equities. Alternative investment assets (gold, precious metals, commodities, etc.) have made their space in global portfolios as investors are looking for better diversified portfolios as compared to 60/40 counterparts. Click here (link to ‘Benefits of diversifying your investments’ – coming soon) to read about benefits of investment portfolio diversification.

Year 2022 has been an eventful year with a lot of negative economic news, particularly the rapid interest rate hikes that are yet to show its full impact on growth, employment, housing market, corporate earnings and other key indicators. Year 2023 is expected to be a challenging year as economies shift towards a higher rate environment after a period of relaxed monetary policy and fiscal stimulus, especially during covid-19. Staying nimble and adjusting investment positions as events unfold will remain key to maintaining portfolio value and growth overtime.

You can book a free consultation with one of our Financial Advisers to learn more about our investment approach and how we can help you.

Disclaimer

Past performance is not a reliable indicator of current or future returns. This overview contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation