Gold is both a physical commodity and a financial asset. It underpins jewellery and technology, anchors central‑bank reserves, and increasingly serves as a strategic hedge in investment portfolios. Its recent price surge has been driven mainly by safe‑haven demand, central‑bank buying, and expectations of lower interest rates amid persistent geopolitical and macroeconomic uncertainty. The following sections highlight each of these areas in more detail.

What gold is and why it matters

Gold is a scarce metal with high durability, divisibility and recognisability, which is why it has been used as a store of value and medium of exchange for millennia. It does not decay, is easily shaped, and has relatively predictable supply growth via mining, making it attractive as a monetary asset in contrast to fiat currencies that can be expanded quickly.

Modern monetary systems are no longer backed by gold, but central banks still hold large gold reserves for diversification and confidence in their balance sheets. Surveys of central banks highlight gold’s perceived role as a long‑term store of value; crisis hedge and portfolio diversifier in official reserves.

Main uses of gold today

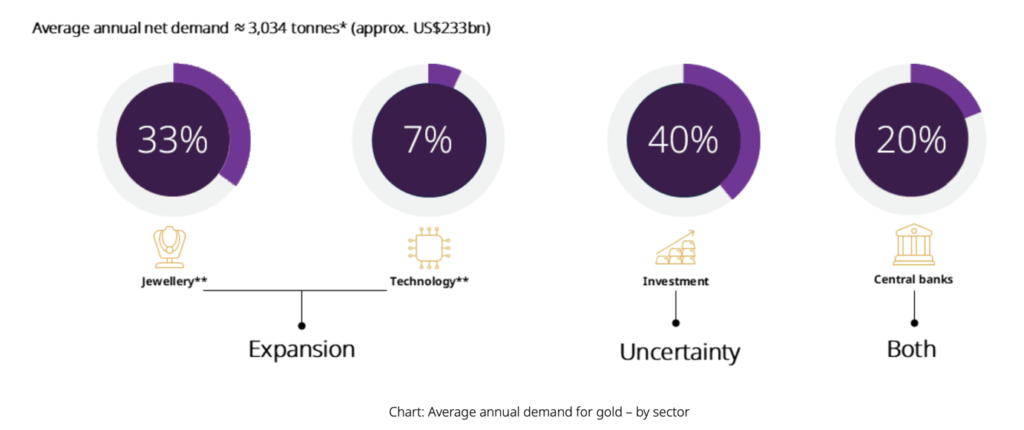

The demand for gold comes from four broad sectors: jewellery, investment, central banks and technology. Historically jewellery has represented the largest share; it still accounts for around half of annual demand over long periods, though its share has declined as investment and central‑bank demand have risen.

In 2025, investment overtook jewellery as the leading demand category, with total gold investment demand rising 84% year‑on‑year to a record 2,175 tonnes, largely via exchange‑traded funds (ETFs). Jewellery production fell by about 19% in 2025 and is expected to stay subdued as high prices make jewellery less affordable, especially in price‑sensitive markets like India.

Central banks have become a structurally important source of demand, particularly since the global financial crisis and Russia’s reserve freeze in 2022. Central‑bank purchases accounted for more than 20% of global demand in 2024, up from roughly 10% in earlier years, and emerging‑market institutions are increasing gold as a share of reserves for diversification and geopolitical hedging.

Gold also has industrial and technological uses, particularly in electronics and specialist applications, because of its conductivity and corrosion resistance, though this is a relatively small share of total demand compared with jewellery and investment.

Source: World Gold Council

Recent return performance

Gold has delivered notably strong performance in both 2024 and 2025. An annual review of 2024 performance notes that gold produced 27% returns and outpaced the S&P 500, supported by geopolitical tensions, expectations of rate cuts, and robust central‑bank buying.

In 2025, gold’s rally accelerated, with over 64% price increase over the year as it surged toward and then through the 4,000‑dollar level. And just in January 2026 (as of 29 Jan 2026), gold price is up exceptional 27% from the close of 31 Dec 2025. The World Gold Council records that 2025 investment demand reached a record high, underscoring the strength of the price move. From 2024 through early 2026, gold thus delivered very strong cumulative gains, especially in dollar terms, making it one of the better‑performing major asset classes over that period. In summary:

- 2024: Elevated central‑bank purchases (over 20% of global demand) and rising investment demand offset weaker jewellery consumption.

- 2025: Investment demand jumped 84% to 2,175 tonnes, jewellery fell 19%, and prices reached record highs above 4,000 dollars per ounce.

- Early 2026: Continued investment demand along with central banks purchases pushed gold prices above 5,500 dollars per ounce.

These patterns show a shift from traditional jewellery‑driven demand toward an investment‑ and reserve‑driven bull cycle.

Key price drivers in recent years

Gold’s rally into late 2024 and especially 2025 has been unusually strong by historical standards. The metal broke above 4,000 US dollars per ounce in October 2025, with the World Gold Council noting that 2025 is on course to be its strongest calendar‑year performance since 1979. Further, it was last seen being traded above 5,500 US dollars per ounce in late January 2026. The main drivers of this move include:

- Safe‑haven demand from geopolitical risk: Ongoing conflicts (including the Russia‑Ukraine war and Middle East tensions) and broader security concerns have pushed investors toward gold as a crisis hedge.

- Expectations of monetary easing: Anticipation of, and then actual, interest‑rate cuts by major central banks increased gold’s appeal, because the opportunity cost of holding a non‑yielding asset falls when real and nominal yields decline.

- Central‑bank buying: Central‑bank purchases have remained elevated, supporting prices directly via offtake and indirectly by reinforcing gold’s narrative as a strategic reserve asset.

- ETF and retail investment flows: Strong inflows into gold ETFs and bar/coin demand, especially in Western markets and parts of Asia, have amplified price gains.

- Dollar dynamics and macro policy concerns: Episodes of US dollar weakness, worries about US fiscal sustainability, and debates over Federal Reserve independence have all tended to support gold prices.

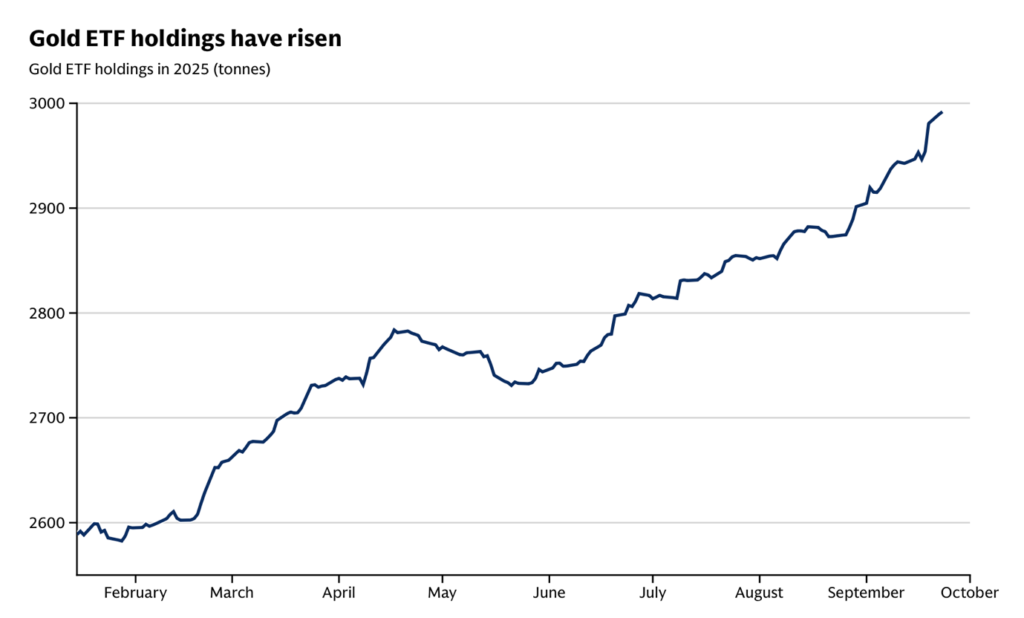

The following graph highlights the pattern of Gold ETF holdings during 2025, which was a major contributor to the gold price upside.

Source: Goldman Sachs

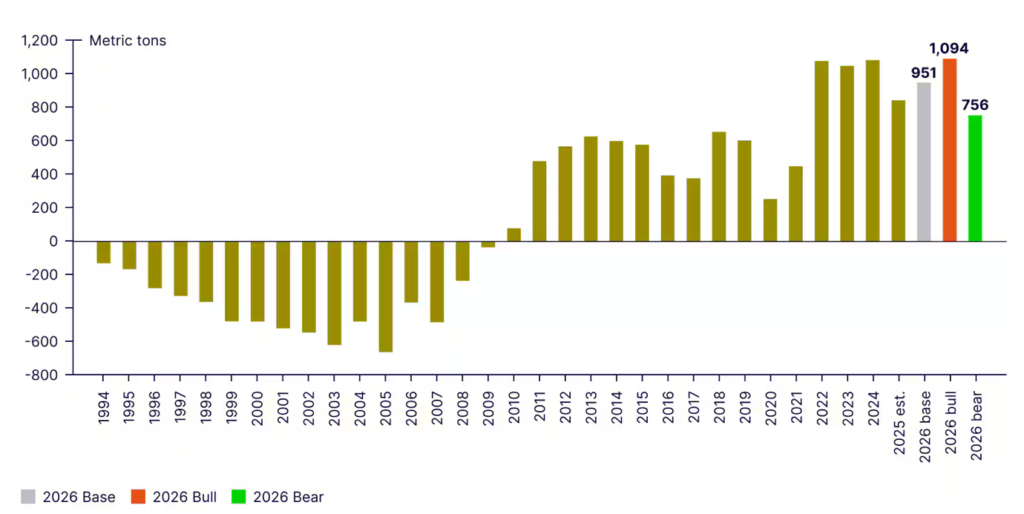

Central banks buying, started from 2010 and is continued, was one of the key factors behind gold price rally in last few years. The following graph provides the history of Central banks buying patterns and the outlook for 2026.

Source: State Street Investment Management

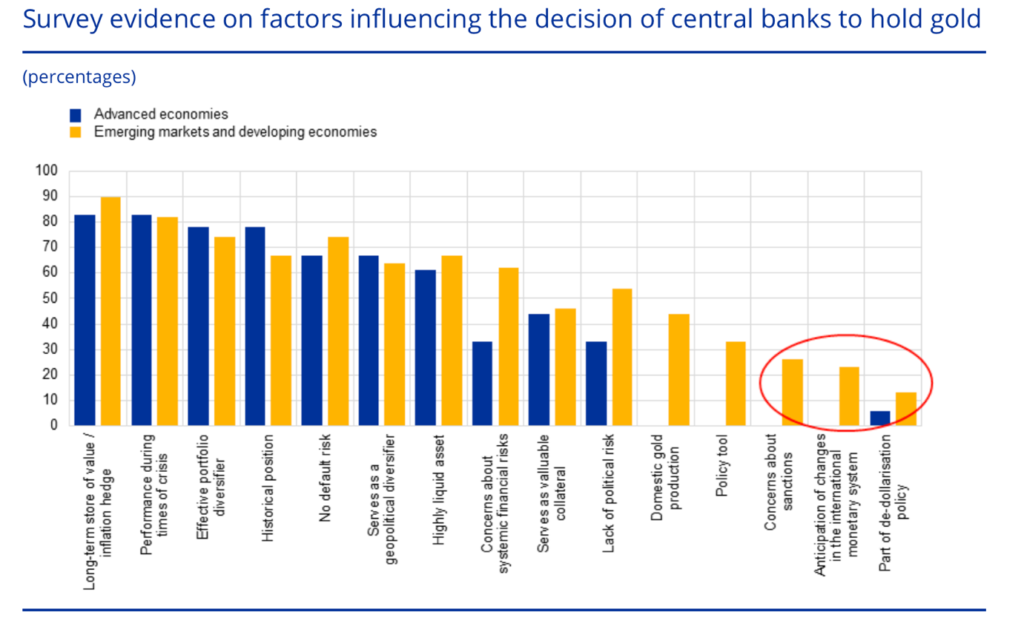

Some central banks in emerging and developing economies have cited sanctions and declining major currency roles as reasons for their gold investments. About a quarter of these banks noted such concerns when determining gold exposure. Recent increases in official gold reserves are mainly concentrated in a few countries, with Turkey, India, and China jointly acquiring over 600 tonnes since late 2021.

Source: European Central Bank

At the same time, supply growth has been constrained by permitting and regulatory hurdles that slow mine expansion, which analysts argue has limited the ability of higher prices to elicit rapid supply responses. High prices have, however, weighed on price‑sensitive jewellery demand, especially in emerging markets, partially offsetting some investment‑driven strength.

Role in investment portfolios

As 60/40 portfolios are not perfect solutions for today’s changing investment landscape, alternative assets making their appeal. Gold plays several roles in diversified portfolios, especially for long‑term investors and institutions.

- Hedge against extreme risk: Gold has a history of performing relatively well during major crises, such as financial stress, wars, or sharp equity market drawdowns, making it a potential tail‑risk hedge.

- Inflation and currency hedge: Central banks and private investors often view gold as a partial hedge against high inflation or loss of confidence in fiat currencies, although the relationship is stronger over long horizons than year‑to‑year.

- Portfolio diversifier: Gold’s long‑run correlations with stocks and bonds tend to be low or even negative in periods of stress, so a modest allocation can improve risk‑adjusted returns, which is why many central banks and asset managers include it in strategic asset mixes.

- Return potential: Beyond risk management, the latest bull phase has delivered strong absolute returns relative to many major asset classes, which has attracted more tactical money into gold and gold‑linked instruments.

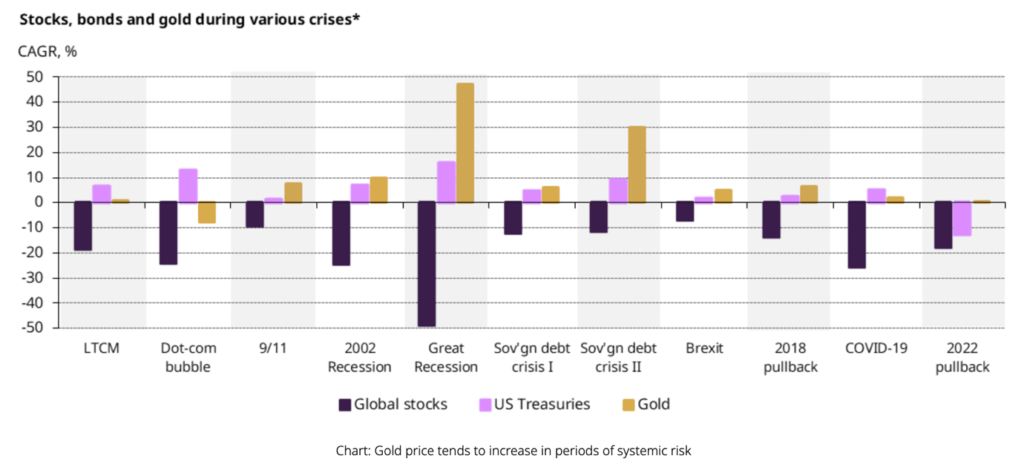

The following graph explains how gold has performed during periods of heightened uncertainty and financial markets stress.

Source: World Gold Council

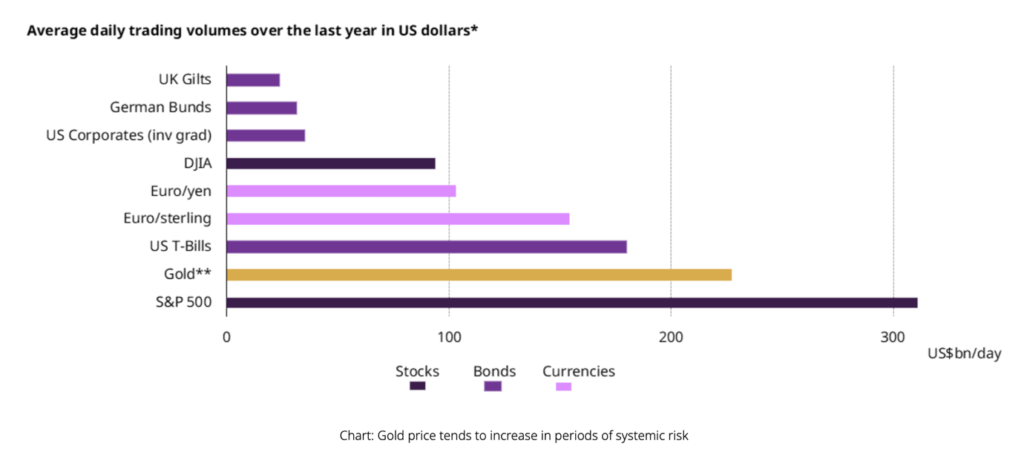

Last year (2025) saw a significant increase in trading volume for gold, second only to the S&P 500, driven by the factors mentioned above.

Source: World Gold Council

For individual investors, gold exposure can be obtained via physical bullion, coins, ETFs, gold‑mining equities, or structured products, each with different liquidity, cost and risk characteristics. Portfolio allocation guidelines vary, but many institutional discussions centre on a single‑digit to low‑double‑digit percentage allocation, adjusted for risk tolerance, time horizon and views on macro risk.

In practice, portfolio allocations that include precious metals often tilt more toward gold for stability, with a smaller allocation to silver to add cyclical and higher‑beta exposure. We at Simply Ethical gave a decent allocation to both gold and silver couple of years back purely for portfolios diversification and optimisation purposes, which helped to add in the return profile of different portfolio prepositions. We are still maintaining a sizeable allocation to them backed by the factors highlighted in this article. You can explore different investment portfolios here (including Personal Pensions, ISAs, and General Investment Accounts) that best describes your risk/return profile and investment objectives.

Outlook for gold

Most institutional outlooks going into 2026 see a constructive but uncertain environment for gold, with scenarios depending heavily on growth, inflation, geopolitics and central‑bank policy.

The World Gold Council frames 2026 as a year in which gold may trade in a broad range if current macro conditions persist, with upside if growth slows and rates fall, and downside if policy success delivers higher yields and a stronger dollar. Several banks also argue that structural central‑bank demand, especially from emerging markets that still hold a relatively small share of reserves in gold compared with developed economies, is likely to continue for at least the next few years, providing a supportive underlying bid.

For an investor building or reviewing a diversified portfolio, gold can thus be viewed as a strategic hedge against macro and geopolitical risks, but its current elevated price level and the possibility of higher volatility argue for measured allocations rather than aggressive concentration.

To explore our range of tax-efficient investing solutions (ISAs, JISAs, SIPPs) as well as other investment management products and financial advice service, visit our website here.

To learn more about how we can help you and our investment approach, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.