In the Autumn Budget delivered by Chancellor Rachel Reeves on 26 November 2025, one of the most significant reforms affecting everyday savers was a change to ISA (Individual Savings Account) rules.

Cash ISA annual limit reduced

- From 6 April 2027, for most adults under the age of 65, the annual tax-free Cash ISA allowance will fall from £20,000 to £12,000.

- The overall ISA allowance remains £20,000 per year — but under-65s must now put at least £8,000 into a Stocks & Shares ISA (or another ISA type) if they want to use the full £20,000.

- People aged 65 and over are exempt from this change and may still save up to £20,000 in a Cash ISA each year.

- This is one of the biggest changes to the UK ISA system since ISAs were introduced in 1999.

Why has the Government cut the Cash ISA limit?

The government says the aim is to encourage savers to invest more, rather than hold large cash balances. The UK traditionally has low levels of retail investment compared with other developed countries, and directing more money into Stocks & Shares ISAs could, in theory, boost capital formation and economic growth.

Supporters of the change argue that:

- Stocks & Shares ISAs generally offer higher potential returns over the long term than cash, helping savers beat inflation.

- Channelling capital toward investment markets could support business growth and broader economic activity.

Critics, however, caution that not all savers want or need investment risk, especially those nearing retirement or saving for short-term goals. Some voices in finance have described the policy as potentially punishing cautious savers.

What it means for Cash ISA Savers?

Under-65 Savers:

- If you are under 65, you can only put £12,000 a year into a Cash ISA from April 2027.

- To use the full £20,000 annual ISA allowance, you’ll need to direct the remaining £8,000 into a Stocks & Shares ISA or another ISA type.

- This change may encourage some savers to rethink the role of cash savings versus investment. It could be sensible to review whether holding cash or investing part of your ISA allowance better fits your goals and risk tolerance.

Over-65 Savers:

- Savers aged 65 and over can continue to put up to £20,000 per year into Cash ISAs, with no new restriction.

- This exemption recognises that older savers often prioritise security and liquidity over investment risk.

Transitional planning:

- If you want to take advantage of the current £20,000 cash allowance, you have until April 2027 to make deposits under the old rules.

- For savers holding large cash balances outside ISAs, it may be worth looking at ISA opportunities before the change to protect tax-free growth.

What it means for Stocks & Shares ISA Investors?

Opportunity and Considerations:

- Stocks & Shares ISAs still carry the full £20,000 annual allowance.

- Under the new regime, most adults will need to allocate at least £8,000 annually to investments if they want to maximise their tax-free ISA space.

For investors, this could mean:

- A boost to acquisition of equities or funds: More flows into markets could support investment returns over time.

- Greater focus on long-term performance: Stocks & Shares ISAs are designed for medium to long-term investment and holding them appropriately can help weather market volatility.

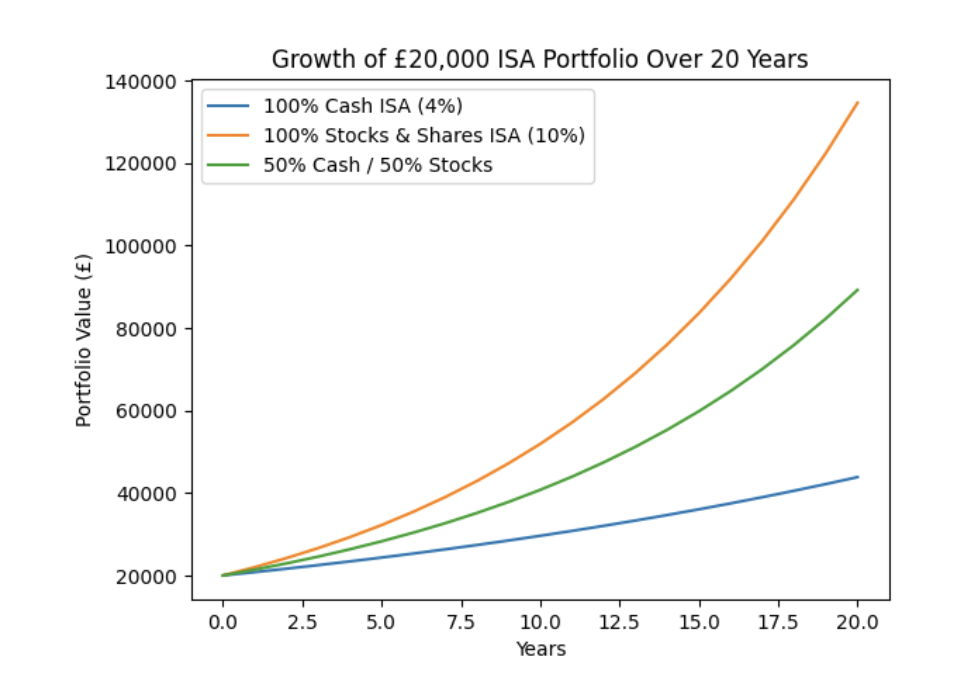

Let’s consider a hypothetical example. Assume 4% return on Cash ISA and 10% long-term average return on stocks (The MSCI World Islamic Index or DJ Dow Jones Islamic Market World Index). Below is a performance comparison table showing how a £20,000 ISA portfolio could grow over 5, 10, and 20 years under three scenarios, assuming annual compounding and no taxes (as per ISA rules).

End Portfolio value comparison (£)

| Time Horizon | 100% Cash ISA (4%) | 100% Stocks & Shares ISA (10%) | 50% Cash / 50% Stocks |

| 5 years | £24,333 | £32,210 | £28,272 |

| 10 years | £29,605 | £51,875 | £40,740 |

| 20 years | £43,822 | £134,550 | £89,186 |

What this example shows?

- Cash ISA (4%) delivers steady, low-risk growth, strong capital protection, but limited inflation-beating power over long periods.

- Stocks & Shares ISA (10%) – significantly higher long-term growth potential, however, comes with short-term volatility, but long-term compounding dominates.

- 50/50 Split (Cash + Stocks) – a balanced middle ground, captures a large part of equity upside while reducing overall volatility.

- Forced diversification (post-Budget rules) may actually improve long-term wealth outcomes for many savers.

New rules on cash within Investment ISAs

Alongside the Cash ISA limit change, HMRC is planning measures to prevent people from circumventing the new cap, including blocking transfers from Stocks & Shares ISAs back into cash ISAs and potentially charging tax on cash held within investment ISA accounts, depending on final legislation.

Pros and Cons for different Savers

| Saver Type | Potential Benefits | Potential Concerns |

| Young or long-term savers | Encouraged to invest early for growth | Must take on investment risk |

| Cautious cash savers | Still have some tax-free shelter | Reduced tax-free cash allowance |

| Retirees (65+) | No change to full cash allowance | Fewer impacts |

| ISA maximiser | Encourages balanced ISA use | Must plan mix of cash & investments |

Practical tips for Savers & Investors

- Review your savings goals: Decide whether you need cash for emergencies or can invest for longer horizons.

- Consider diversification: Even within Stocks & Shares ISAs, a mix of assets (e.g. equities, sukuks, commodities) can help manage risk.

- Act before April 2027: If you rely heavily on Cash ISAs, you might want to utilise the current higher allowance before the change.

Bottom line

The Autumn Budget 2025 Cash ISA cut marks a major shift in how tax-free savings work in the UK. By reducing the Cash ISA limit for under-65s to £12,000 and encouraging greater allocation into stocks and shares, the government is nudging savers toward investing.

For cash savers, this may prompt reassessment of savings strategies. For investors, it could be an opportunity to build long-term wealth, provided the risks and personal circumstances are carefully considered. As with all financial planning, individual needs vary, and professional advice can help tailor the best approach.

To explore our range of tax-efficient investing solutions (ISAs, JISAs, SIPPs), visit our website here.

To learn more about how we can help you and our investment approach, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.