Economic and Market Overview

In Q4 2025, global economies and financial markets were primarily shaped by shifting expectations around monetary policy, slowing growth momentum, and persistent inflation risks. Central banks in major economies signalled a cautious stance, balancing early discussions of rate cuts against concerns over sticky services inflation and elevated wage pressures. Fixed income markets were volatile as yields responded to changing growth and policy outlooks, while equity markets saw increased dispersion between AI-led growth stocks and more cyclical sectors. A stronger US dollar for much of the quarter tightened global financial conditions, particularly for emerging markets. Meanwhile, softer global trade and investment flows reflected the lagged impact of restrictive financial conditions earlier in the year. Overall, Q4 was characterised by heightened uncertainty as markets positioned for a macroeconomic inflection heading into 2026.

On 26 November 2025, the UK government under Chancellor Rachel Reeves unveiled its Autumn Budget Statement, aiming to tackle persistent fiscal challenges while supporting growth and public services. The Budget focused heavily on generating additional revenue through extended freezes on personal tax thresholds and reforms to pension and savings tax reliefs, alongside structural changes to business and investment taxation. It also outlined plans to cut the cost of living, for example by reducing energy costs for households, and committed funding to public services such as the NHS and infrastructure. The Office for Budget Responsibility published updated economic forecasts alongside the Statement, underscoring the delicate balance between fiscal consolidation and economic support. These measures reflected the government’s priorities of stabilising the economy, strengthening public finances, and addressing long-standing social needs amid a challenging economic backdrop.

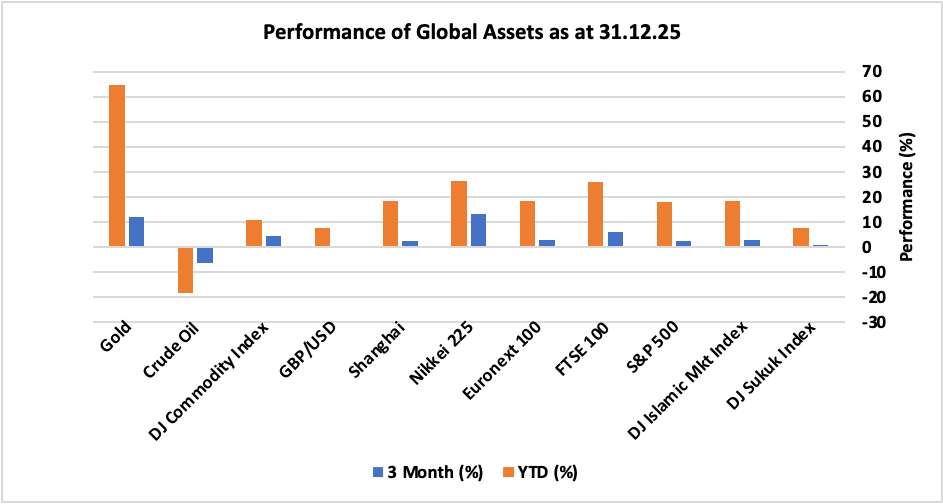

In Q4 2025, global equity markets showed modest gains overall, with developed market indices finishing the quarter on a positive footing as investors looked past mid-quarter volatility and priced in expectations of easing monetary policy. The US S&P 500 posted slight positive 2.3% returns for the quarter as strong earnings and AI-led optimism countered late-year profit-taking, helping it extends its 2025 gain to roughly high‐teens percentage (+17.9%). The UK FTSE 100 continued its strong year-end momentum with a solid Q4 rise of 5.78% contributing to one of the best annual performances globally (+25.8%), driven by mining and safe-haven inflows with gold strength boosting resources stocks. EU Euronext 100 also broadly rose in Q4 (+2.71%) in line with pan-European equities, supported by fiscal optimism and rate-cut prospects.

Asian markets were mixed: Japan’s Nikkei 225 maintained above-average returns of 13% through the quarter, while China’s Shanghai index saw 2.22% positive performance amid supporting policies despite ongoing structural economic challenges and sentiment headwinds. Emerging and alternative indices like the DJ Islamic Markets Index showed relative resilience 2.8% positive performance, while the DJ Sukuk Index posted modest gains of about 0.97%, reflecting stable yields. In FX markets, GBP/USD softened moderately as dollar showed strength during the quarter. In commodities, gold surged significantly, up 12%, (continuing its strong up-trend on geopolitical and inflation hedging) while the DJ Commodity Index rose 4.2%, weighed down by weaker energy prices. These patterns reflected a backdrop of cautious risk appetite, interest rate pivot pricing and persistent macro/geopolitical uncertainty.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q4 2025, as well as the full year performance.

Performance of global assets Q4 2025

Portfolio Commentary

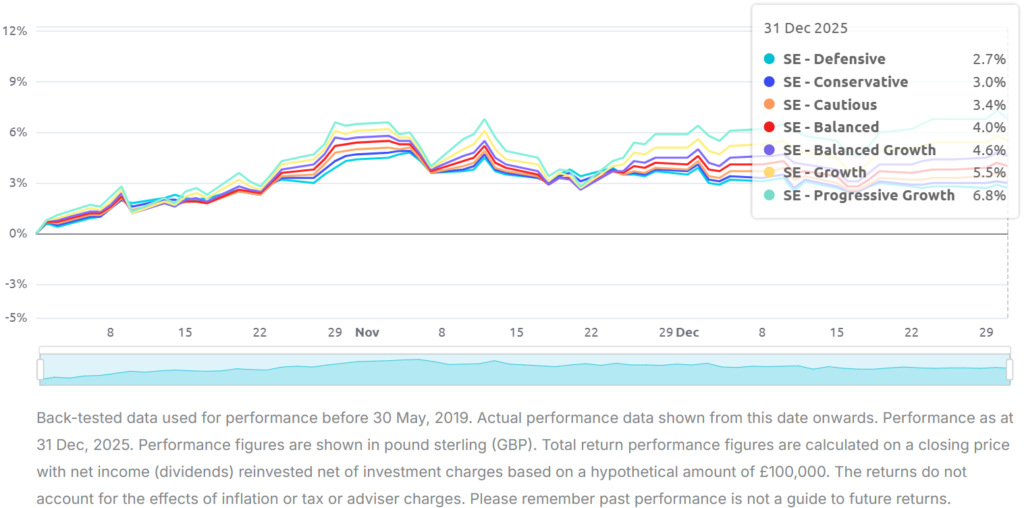

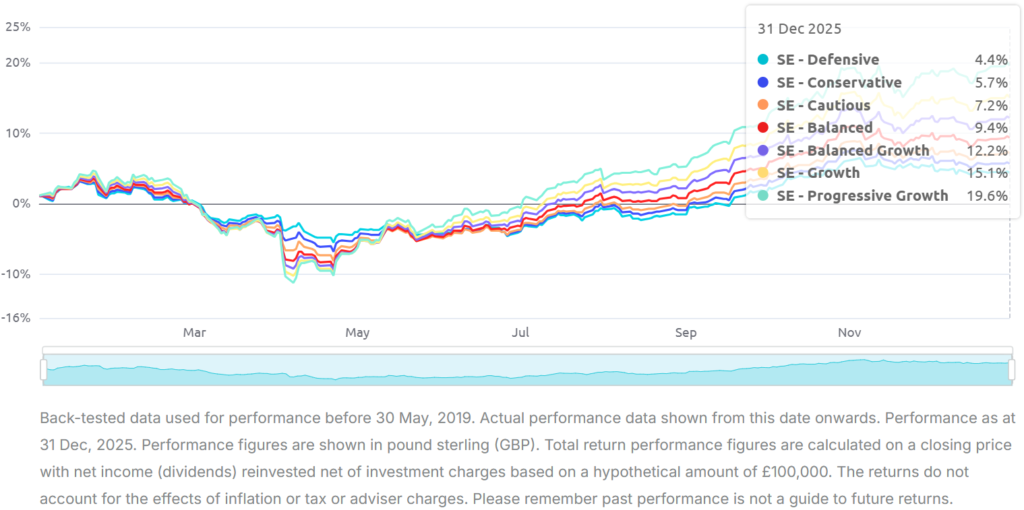

During the Fourth quarter, all investment portfolios performed positively as markets rallied. Progressive Growth portfolio appreciated the most, with a 6.8% rise in value during the period, with a full year performance of 19.6%. Overall, the performance of equity markets in general and precious metals exposure in both gold and silver in particular enhanced the annual returns for all our investment portfolios. Our brave call on silver paid off!

Performance of Simply Ethical Online Portfolios in Q4 (01 October 2025 – 31 December 2025)

Full Year 2025 performance of Simply Ethical Online Portfolios (01 January 2025 – 31 December 2025)

During the quarter, there were no changes made to the investment allocation for any portfolios. We continue to maintain a cautious view on investments, given current market valuations particularly for some US big techs along with macroeconomic concerns including sticky inflation, fiscal strains in the US, Japan, and UK, policy uncertainties and geopolitical risks amongst other factors pose a possible downside risk to the markets.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.