Economic and Market Overview

Global economies and financial markets in Q3 2025 were shaped by a delicate balance between sticky inflation, uneven growth, lingering policy uncertainty, and heightened geopolitical risks. While headline inflation fluctuated in most advanced economies, sticky core prices and cautious central banks kept interest rates elevated, restraining business investment and consumer confidence to some extent. The U.S. economy showed relative resilience, but Europe and the UK struggled with weak demand and fiscal constraints, while China’s slowdown and trade tensions dampened global trade momentum. Currency markets reflected diverging growth paths, with the U.S. dollar strengthening and emerging-market currencies under pressure. Equity markets traded strong, driven by AI and resilient earnings across tech sector, while bond yields softened amid shifting expectations for rate cuts. Overall, Q3 2025 highlighted the global economy’s fragile transition from inflation management to growth stabilization.

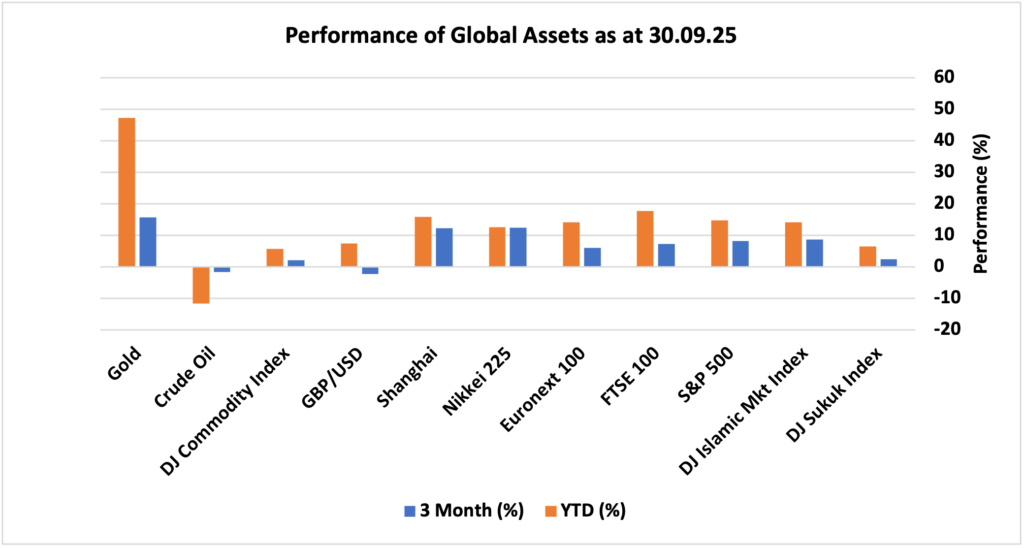

Looking at the performance of major asset classes in Q3 2025 (1 July – 30 September), global financial markets demonstrated a robust and broad-based rally, with nearly all sectors benefiting from improved investor sentiment and shifting macroeconomic dynamics. The quarter was marked by heightened geopolitical risk and persistent concerns around global security, which fuelled a strong flight to safety. This was particularly evident in the gold market, where prices soared, delivering an impressive 15.7% return for the quarter. Investors sought refuge in the precious metal as tensions escalated in the Middle East and other flashpoints, underscoring gold’s traditional role as a safe-haven asset during times of uncertainty.

Equity markets also experienced notable gains. In Asia, both the Japanese Nikkei 225 and China’s Shanghai Composite Index surged by more than 12%, reflecting renewed optimism amid ongoing tariff negotiations, resilient corporate earnings, and the accelerating momentum of the artificial intelligence (AI) sector. North American equities followed suit, with the U.S. S&P 500 Index and the Dow Jones Islamic Markets Index each advancing just over 8%. These gains were attributed to a combination of resumed trade talks, strong quarterly results from leading technology firms, and growing investor confidence in the sector’s long-term prospects.

European equities were similarly buoyant, with the Euronext 100 Index climbing 6% and the UK’s FTSE 100 Index rising by a more pronounced 7.2%. This performance was underpinned by improved economic data and renewed fiscal stimulus measures in key economies, which helped support risk appetite across the continent. However, currency markets told a different story, where sterling (GBP) depreciated by 2.2% against the US dollar, reflecting ongoing concerns about the UK’s economic outlook and diverging monetary policy expectations between the Bank of England and the US Federal Reserve.

The fixed-income space also posted positive returns in Q3, as central banks in major economies signalled a shift towards more accommodative monetary policy. The Dow Jones Sukuk Index, representing Islamic fixed-income securities, returned 2.5% as bond yields trended lower in response to anticipated interest rate cuts. This environment proved favourable for fixed-income investors, who benefited from both price appreciation and a more supportive policy backdrop.

Apart from precious metals, other commodities showed mixed results, with crude oil prices declining by roughly 1.7% during the quarter. This downward movement was largely attributed to increasing production levels from OPEC+ countries, which outweighed persistent geopolitical risks and contributed to a moderate supply surplus. As a result, energy markets lagged other asset classes, even as the broader commodities complex remained sensitive to ongoing global developments.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q3 2025, as well as their progress year-to-date.

Performance of Global Assets Q3 2025

Portfolio Commentary

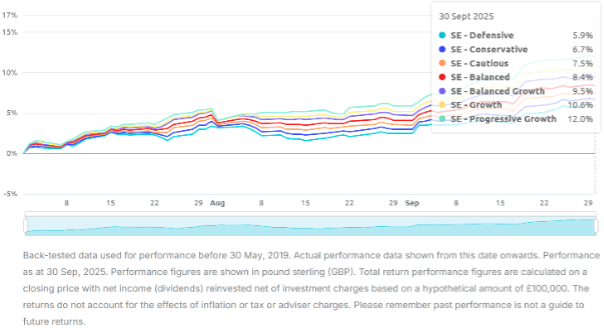

During the third quarter, all investment portfolios performed positively as markets rallied. Progressive Growth portfolio appreciated the most, with a 12% rise in value during the period. The lowest risk portfolios, namely, Defensive, Conservative and Cautious portfolios appreciated in value after a negative second quarter. The depreciation of GBP/USD (2.21%) enhanced the performance of lowest risk portfolios along with broader rise in all asset classes.

Performance of Simply Ethical Online Portfolios in Q1 (01 July 2025 – 30 September 2025)

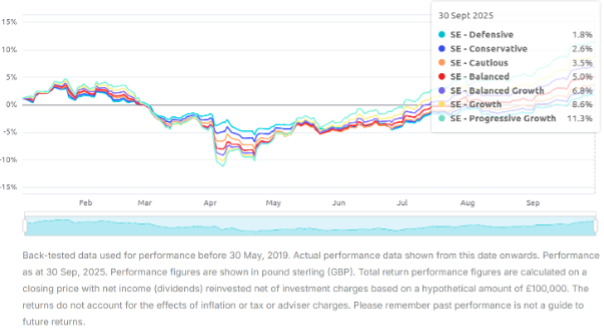

Year to Date Performance of Simply Ethical Online Portfolios (01 January 2025 – 30 September 2025)

During the quarter, there were no changes made to the investment allocation for any portfolios. The world’s largest equity market, the US advanced over 8% during the quarter, supported by resilient earnings and optimism around AI-driven productivity gains, however, we continue to maintain a cautious view on investments, given current market valuations particularly for some US big techs along with macroeconomic concerns including sticky inflation, fiscal strains in the US and UK, policy uncertainties and geopolitical risks amongst other factors pose a possible downside risk to the markets.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.