In Q4 2025, global economies and financial markets were primarily shaped by shifting expectations around monetary policy, slowing growth momentum, and persistent inflation risks. Central banks in major economies signalled a cautious stance, balancing early discussions of rate cuts against concerns over sticky services inflation and elevated wage pressures. Fixed income markets were volatile as yields responded to changing growth and policy outlooks, while equity markets saw increased dispersion between AI-led growth stocks and more cyclical sectors. A stronger US dollar for much of the quarter tightened global financial conditions, particularly for emerging markets. Meanwhile, softer global trade and investment flows reflected the lagged impact of restrictive financial conditions earlier in the year. Overall, Q4 was characterised by heightened uncertainty as markets positioned for a macroeconomic inflection heading into 2026.

On 26 November 2025, the UK government under Chancellor Rachel Reeves unveiled its Autumn Budget Statement, aiming to tackle persistent fiscal challenges while supporting growth and public services. The Budget focused heavily on generating additional revenue through extended freezes on personal tax thresholds and reforms to pension and savings tax reliefs, alongside structural changes to business and investment taxation. It also outlined plans to cut the cost of living, for example by reducing energy costs for households, and committed funding to public services such as the NHS and infrastructure. The Office for Budget Responsibility published updated economic forecasts alongside the Statement, underscoring the delicate balance between fiscal consolidation and economic support. These measures reflected the government’s priorities of stabilising the economy, strengthening public finances, and addressing long-standing social needs amid a challenging economic backdrop.

Macroeconomic picture

In Q4 2025, key macroeconomic indicators painted a nuanced picture across major economies. In the United States, inflation continued to moderate toward the Federal Reserve’s target, with cooling price pressures and labour markets supporting steady growth as GDP remained resilient, while wage growth eased and unemployment showed some weakness, pushing Fed to cut rates. In the Eurozone, inflation was close to target levels and real GDP growth showed modest expansion, although unemployment stayed elevated compared with pre-pandemic averages. The United Kingdom experienced slower growth with headline CPI still above target but gradually easing, and indicators pointed to weaker domestic demand amid persistent price pressures. China’s economy saw early signs of recovery late in the quarter, with manufacturing PMI rising above expansionary levels, yet consumer demand remained weak and structural challenges persisted, limiting robust inflationary pressure. In Japan, inflation remained modestly above target, with the Bank of Japan navigating persistent price pressures alongside subdued growth, while broader indicators suggested cautious consumption dynamics. Together, these trends reflected divergent regional dynamics as policymakers balanced growth support with inflation control.

The following table lists the latest key macroeconomic indicators across major economies.

Date: 05 Jan 2026

Financial markets performance

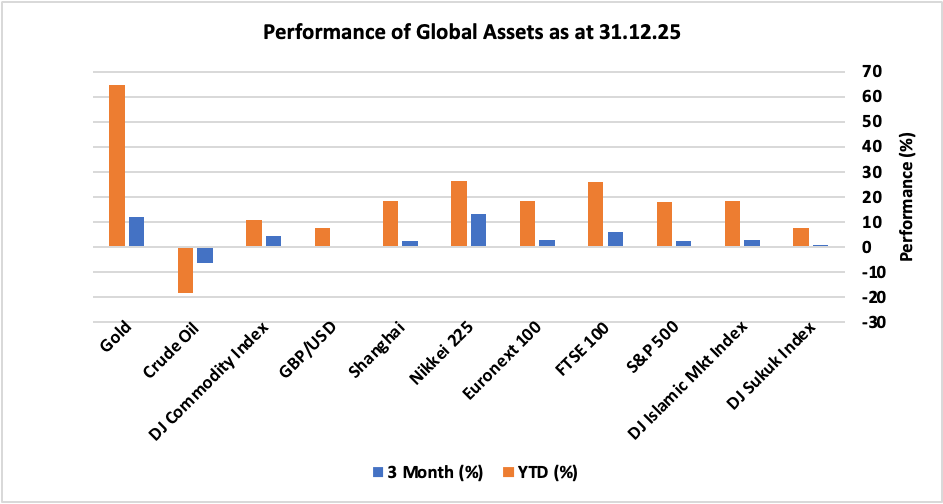

In Q4 2025, global equity markets showed modest gains overall, with developed market indices finishing the quarter on a positive footing as investors looked past mid-quarter volatility and priced in expectations of easing monetary policy. The US S&P 500 posted slight positive 2.3% returns for the quarter as strong earnings and AI-led optimism countered late-year profit-taking, helping it extends its 2025 gain to roughly high‐teens percentage (+17.9%). The UK FTSE 100 continued its strong year-end momentum with a solid Q4 rise of 5.78% contributing to one of the best annual performances globally (+25.8%), driven by mining and safe-haven inflows with gold strength boosting resources stocks. EU Euronext 100 also broadly rose in Q4 (+2.71%) in line with pan-European equities, supported by fiscal optimism and rate-cut prospects. Asian markets were mixed: Japan’s Nikkei 225 maintained above-average returns of 13% through the quarter, while China’s Shanghai index saw 2.22% positive performance amid supporting policies despite ongoing structural economic challenges and sentiment headwinds. Emerging and alternative indices like the DJ Islamic Markets Index showed relative resilience 2.8% positive performance, while the DJ Sukuk Index posted modest gains of about 0.97%, reflecting stable yields. In FX markets, GBP/USD softened moderately as dollar showed strength during the quarter. In commodities, gold surged significantly, up 12%, (continuing its strong up-trend on geopolitical and inflation hedging) while the DJ Commodity Index rose 4.2%, weighed down by weaker energy prices. These patterns reflected a backdrop of cautious risk appetite, interest rate pivot pricing and persistent macro/geopolitical uncertainty.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q4 2025, as well as their progress year-to-date.

Performance of global assets Q4 2025

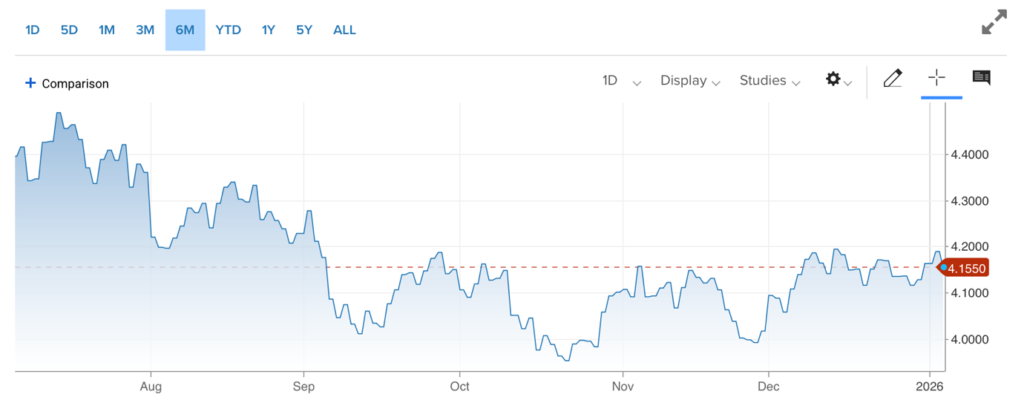

US Treasury Yields

In the fourth quarter of 2025, U.S. 10‑year Treasury yields did not experience significant volatility and ended the quarter flat, despite the rate cut during the period. The U.S. Fed cut interest rates twice in Q4. Additionally, the softer economic data, including signs of weakening U.S. labour reinforced bets on upcoming rate cuts. However, concerns over rising debt level, trade frictions, and geopolitical situation all added to the perceived risk levels that kept long dated yields elevated.

10-Year Treasury yields – US

Source: CNBC

Geopolitical situation

Throughout Q4 2025, geopolitics remained highly influential on global stability, particularly in the Russia-Ukraine and Israel-Hamas conflicts. On the Eastern European front, heavy Russian bombardments and drone strikes against Ukrainian infrastructure continued into winter, with significant military engagements around key fronts such as Donetsk and persistent pressure on Ukrainian cities and energy grids, even as diplomatic efforts toward formalized security guarantees gained traction among Western allies. In the Middle East, an earlier ceasefire between Israel and Hamas agreed in October under U.S. and regional mediation marked a pivotal shift after years of hostilities, though periodic violence and humanitarian strains persisted around Gaza. These overlapping conflicts in late 2025 heightened global risk perceptions, influencing commodity prices, safe-haven flows, and diplomatic realignments as the year closed.

Key News & Events in Q4 2025

UK

- The annual inflation rate in the UK decelerated to 3.2% in November 2025, marking the lowest level seen in eight months. This figure represented a notable reduction from the 3.6% recorded in October and was also below both market expectations of 3.5% and the Bank of England’s own forecast of 3.4%. The moderation in inflation suggests that price pressures are easing, possibly reflecting lower energy costs and a slowdown in consumer price increases across various sectors. The trend may indicate that the Bank of England’s earlier policy tightening has started to bear fruit, helping to bring inflation closer to its 2% target.

- In response to the softening inflation and mounting evidence of economic weakness, the Bank of England reduced the Bank Rate by 25 basis points to 3.75% in the fourth quarter of 2025, its lowest level since 2022. This decision, which marked the first rate cut since August, was motivated by policymakers’ concerns over persistent signs of economic strain, including sluggish growth and rising unemployment. The rate cut is intended to support economic activity by making borrowing more affordable for households and businesses, and it signals a shift towards a more accommodative monetary stance as inflationary pressures ease.

- The UK economy grew by a modest 0.1% in the third quarter of 2025, confirming earlier estimates and highlighting a loss of momentum compared to the 0.3% expansion seen in the previous quarter. This slowdown in economic growth reflects subdued consumer spending and weaker business investment, likely influenced by ongoing global uncertainties, higher borrowing costs earlier in the year, and the broader slowdown in international trade. The tepid growth rate underlines the challenges facing the UK economy as it navigates a period of heightened macroeconomic headwinds.

- The UK unemployment rate edged up to 5.1% in the three months to October 2025, meeting market expectations and rising from 5.0% in the previous quarter. This increase, though relatively moderate, points to some softening in the labour market as employers respond to slower economic growth and cost pressures. A higher jobless rate may weigh on consumer confidence and spending, further challenging the outlook for economic recovery in the coming months.

US

- In December 2025, the annual inflation rate in the United States declined to 2.7%, representing its lowest point since July of the same year. This outcome was notably below market forecasts, which had anticipated inflation to reach 3.1%, as well as the 3% rate recorded in September. The lower-than-expected inflation rate suggests that price growth is moderating more rapidly than analysts had predicted, which may reflect easing pressures from energy, housing, and core goods prices. This trend provides further evidence that the Federal Reserve’s previous tightening measures are having the intended effect, potentially paving the way for a more accommodative monetary policy stance in the coming year.

- According to the minutes from the Federal Reserve’s December 2025 meeting, the majority of the Federal Open Market Committee (FOMC) members indicated that further reductions in interest rates may be appropriate in 2026, provided inflation continues to ease. During this meeting, the Fed cut the federal funds rate by 25 basis points to a target range of 3.5%–3.75%, aligning with market consensus and marking the third rate reduction in 2025, and the second within the fourth quarter. This policy move reflects the central bank’s growing confidence that inflation is coming under control, while also aiming to support economic growth amid signs of cooling labour market conditions and softer consumer demand. The Fed’s communications suggest a cautious but flexible approach for the year ahead, dependent on incoming economic data.

- The United States economy posted an annualised growth rate of 4.3% in the third quarter of 2025, according to a delayed estimate, which marked the fastest pace in two years. This result surpassed both the 3.8% expansion achieved in the second quarter and market forecasts of 3.3%. The robust growth was primarily driven by strong consumer spending, increased exports, and higher government expenditure, highlighting the resilience of the US economy even as global headwinds persisted. The improved GDP figures suggest that domestic activity remained vibrant, with households and businesses continuing to spend and invest, despite some moderation in inflation and higher borrowing costs earlier in the year.

- The unemployment rate in the United States rose to 4.6% in November 2025, up from 4.4% in September, and exceeded market expectations of 4.4%. This increase brought the jobless rate to its highest level since September 2021, signalling some cooling in the labour market as hiring slowed and layoffs edged higher. The rise in unemployment may be a consequence of companies adjusting to slower economic momentum and managing costs amid uncertainties around consumer demand and global trade. The higher unemployment rate could weigh on household spending and confidence as 2026 begins, even as policymakers monitor the situation and consider further support for the economy.

Europe

- The annual inflation rate in the Eurozone was revised down to 2.1% in November 2025 from an initial estimate of 2.2%, bringing it in line with the figure recorded in October. This downward revision reflects a slight easing of price pressures across the single currency bloc, as energy costs remained subdued and core inflation components continued to moderate. The stability in inflation suggests that recent policy actions, along with external factors such as lower global commodity prices, may be helping to anchor inflation expectations near the European Central Bank’s target.

- The European Central Bank (ECB) opted to keep borrowing costs unchanged for the fourth consecutive meeting in December 2025, maintaining the main refinancing rate at 2.15% and the deposit facility rate at 2.0%. This decision was widely anticipated by markets, as policymakers continue to stress a cautious and data-driven stance in light of ongoing economic uncertainties. The ECB reiterated that any future changes to monetary policy will be guided by incoming economic data and taken on a meeting-by-meeting basis, signalling prudence as inflation shows signs of stabilising and growth remains subdued.

- Eurozone GDP growth for the third quarter of 2025 was revised slightly higher to 0.3%, up from the preliminary estimate of 0.2% and exceeding the modest 0.1% increase posted in the previous quarter. This upward revision points to a mild improvement in economic activity, driven by resilient domestic demand and a gradual recovery in business investment. Nonetheless, the overall pace of growth remains limited, as the region continues to grapple with external headwinds and lingering effects from higher interest rates earlier in the year.

- The unemployment rate in the Euro area held steady at 6.40 percent in October, reflecting ongoing stability in the labour market despite subdued economic growth. While joblessness remains relatively low compared to historical averages, the stagnant rate suggests that employment conditions have yet to show significant improvement. Policymakers and analysts continue to monitor labour market trends closely, as any persistent weakness could weigh on consumer confidence and pose challenges to the region’s recovery prospects.

China

- China’s annual inflation rate increased to 0.7% in November 2025, rising from 0.2% recorded in October. This acceleration brought inflation in line with market forecasts and represented the highest level since February 2024. The uptick in consumer prices suggests a gradual recovery in domestic demand and signals a possible easing of deflationary pressures that had concerned policymakers in previous months. The improvement in inflation may be attributed to higher food and energy prices as well as targeted government measures aimed at stimulating household consumption.

- The People’s Bank of China (PBoC) chose to maintain key lending rates at historic lows for the seventh consecutive month in December, a move widely anticipated by markets. Specifically, the central bank kept its seven-day reverse repo rate unchanged at 1.4%, which now serves as the primary policy rate. This decision reflects the PBoC’s assessment that further monetary stimulus is currently unnecessary, as the economy appears to be on course to meet its official growth targets for the year. By holding rates steady, the central bank aims to support credit conditions and financial stability while monitoring inflation and growth trends.

- China’s gross domestic product (GDP) expanded by 1.1% quarter-on-quarter in the third quarter of 2025, surpassing market expectations of 0.8% and following a slightly revised 1.0% increase in the second quarter. The stronger-than-expected economic performance was underpinned by decisive policy support from Beijing, including liquidity injections to stabilise financial markets and targeted measures to ease credit strains. These interventions helped counteract weak domestic demand and deflationary pressures, enabling the economy to maintain momentum despite global uncertainties and subdued external demand.

- China’s surveyed urban unemployment rate remained steady at 5.1% in November 2025, unchanged from the previous month and consistent with market expectations. This figure marks the lowest jobless rate since June and suggests that labour market conditions have stabilised, despite ongoing challenges in some sectors. The steady unemployment rate indicates resilience in the urban jobs market, supported by both government employment initiatives and gradual improvements in economic activity.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.