Global economies and financial markets in Q3 2025 were shaped by a delicate balance between sticky inflation, uneven growth, lingering policy uncertainty, and heightened geopolitical risks. While headline inflation fluctuated in most advanced economies, sticky core prices and cautious central banks kept interest rates elevated, restraining business investment and consumer confidence to some extent. The U.S. economy showed relative resilience, but Europe and the UK struggled with weak demand and fiscal constraints, while China’s slowdown and trade tensions dampened global trade momentum. Currency markets reflected diverging growth paths, with the U.S. dollar strengthening and emerging-market currencies under pressure. Equity markets traded strong, driven by AI and resilient earnings across tech sector, while bond yields softened amid shifting expectations for rate cuts. Overall, Q3 2025 highlighted the global economy’s fragile transition from inflation management to growth stabilisation.

Macroeconomic picture

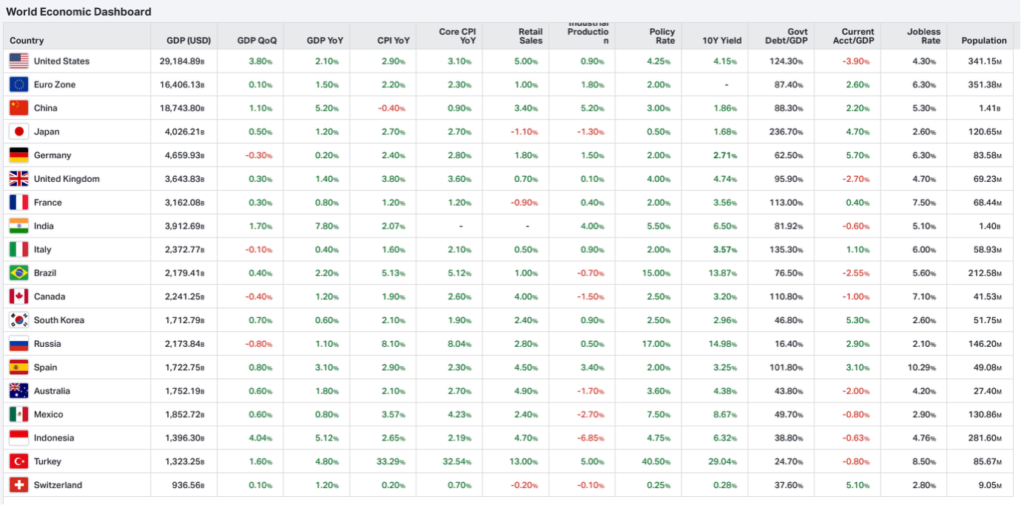

In Q3 2025, macroeconomic data across major economies painted a picture of persistent inflationary pressures and softening monetary policies albeit with uneven momentum. In the UK, growth was sluggish amid cooling demand while inflation hovered near 3.8% (CPI) and the Bank of England held rates steady in their latest policy meeting. The euro area saw growth slow sharply, from mid-year gains to around 0.1% quarterly expansion, even as inflation rebounded modestly to 2.2%, driven by stickier services and energy prices. In the United States, output held up more robustly, though deceleration was evident as GDP was expected to grow around 1.8% in 2025 (Q3 3.8%), and labour markets began to soften, headline and core PCE inflation remained elevated in the 2.9–3.1% range. In Japan, growth surprised slightly on domestic stimulus and wage pressures (via strong “Shunto” wage negotiations), but export headwinds and structural constraints limited its pace, inflation stayed above its low base, reinforcing the central bank’s cautious posture.

Meanwhile, China continued its post-COVID rebalancing where official growth held near target (4-4.5%), but underlying activity cooled, with weak industrial output, soft export demand (especially at the backdrop of U.S. tariffs), and inflation remaining subdued, giving Beijing room (albeit limited) for targeted support. Across these regions, the common thread was that inflation proved more persistent than expected, central banks step carefully between tightening and easing, and growth faces mounting headwinds from trade frictions and weakening demand.

The following table lists the latest key macroeconomic indicators across major economies.

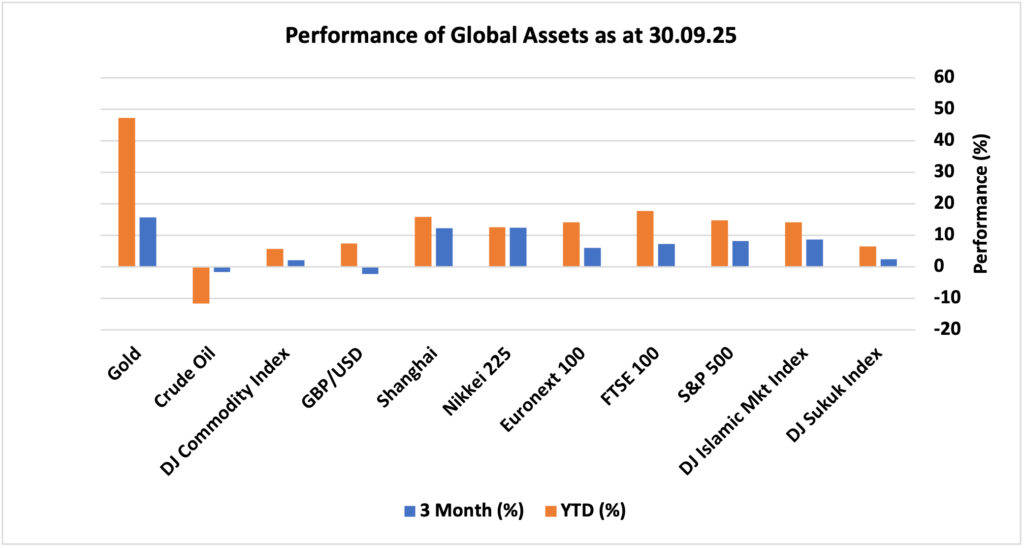

Looking at the performance of major asset classes in Q3 2025 (1 July – 30 September), global financial markets demonstrated a robust and broad-based rally, with nearly all sectors benefiting from improved investor sentiment and shifting macroeconomic dynamics. The quarter was marked by heightened geopolitical risk and persistent concerns around global security, which fuelled a strong flight to safety. This was particularly evident in the gold market, where prices soared, delivering an impressive 15.7% return for the quarter. Investors sought refuge in the precious metal as tensions escalated in the Middle East and other flashpoints, underscoring gold’s traditional role as a safe-haven asset during times of uncertainty.

Equity markets also experienced notable gains. In Asia, both the Japanese Nikkei 225 and China’s Shanghai Composite Index surged by more than 12%, reflecting renewed optimism amid ongoing tariff negotiations, resilient corporate earnings, and the accelerating momentum of the artificial intelligence (AI) sector. North American equities followed suit, with the U.S. S&P 500 Index and the Dow Jones Islamic Markets Index each advancing just over 8%. These gains were attributed to a combination of resumed trade talks, strong quarterly results from leading technology firms, and growing investor confidence in the sector’s long-term prospects.

European equities were similarly buoyant, with the Euronext 100 Index climbing 6% and the UK’s FTSE 100 Index rising by a more pronounced 7.2%. This performance was underpinned by improved economic data and renewed fiscal stimulus measures in key economies, which helped support risk appetite across the continent. However, currency markets told a different story, where sterling (GBP) depreciated by 2.2% against the US dollar, reflecting ongoing concerns about the UK’s economic outlook and diverging monetary policy expectations between the Bank of England and the US Federal Reserve.

The fixed-income space also posted positive returns in Q3, as central banks in major economies signalled a shift towards more accommodative monetary policy. The Dow Jones Sukuk Index, representing Islamic fixed-income securities, returned 2.5% as bond yields trended lower in response to anticipated interest rate cuts. This environment proved favourable for fixed-income investors, who benefited from both price appreciation and a more supportive policy backdrop.

Apart from precious metals, other commodities showed mixed results, with crude oil prices declining by roughly 1.7% during the quarter. This downward movement was largely attributed to increasing production levels from OPEC+ countries, which outweighed persistent geopolitical risks and contributed to a moderate supply surplus. As a result, energy markets lagged other asset classes, even as the broader commodities complex remained sensitive to ongoing global developments.

The following snapshot provides a comprehensive breakdown of the performance of different asset classes in Q3 2025, as well as their progress year-to-date.

Performance of Global Assets Q3 2025

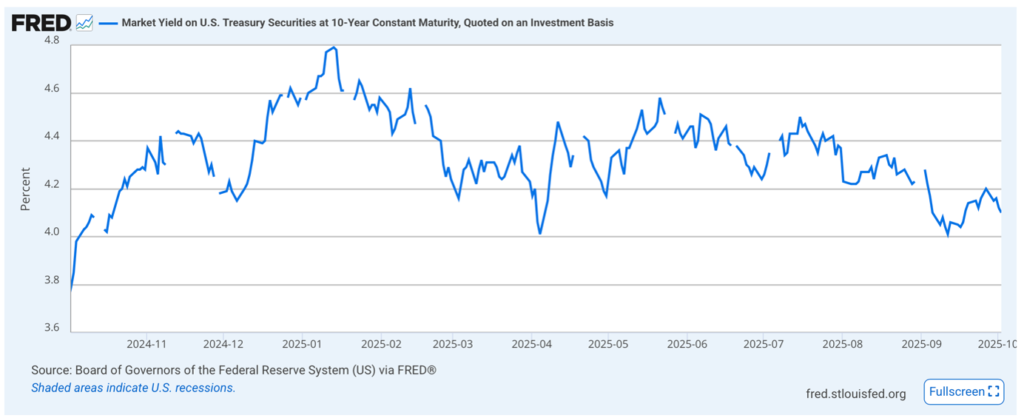

US Treasury Yields – US

In the third quarter of 2025, U.S. 10 year Treasury yields softened by around 15 basis points, sliding from approximately 4.3% in early July to roughly 4.15% by the end of September amid rate cut expectations. The U.S. Fed cut interest rates once in September. Additionally, the softer economic data, including signs of weakening U.S. labour reinforced bets on upcoming rate cuts, pushing yields lower.

10-Year Treasury Yields – US

Bitcoin performance

During the third quarter of 2025, Bitcoin delivered a notably strong performance, appreciating by over 8% and ending September at more than $114,600, having started the quarter at $106,000. This impressive rally was largely fuelled by a significant uptick in institutional investment, alongside the growing popularity and adoption of exchange-traded funds (ETFs) centred on digital assets. The increased demand from large-scale investors provided considerable upward momentum, as more traditional financial players sought exposure to Bitcoin within regulated investment vehicles. This trend was complemented by a broader movement within the crypto sector towards mainstream financial integration, with ETFs acting as a bridge for investors previously hesitant about direct cryptocurrency ownership.

Analysts observed a marked evolution in the perception of Bitcoin, with its reputation shifting from that of a highly speculative asset to a “digital gold”, a reliable store of value during periods of economic and geopolitical uncertainty. This transition was bolstered by the introduction of pro-crypto policies under the Trump administration, which fostered a more favourable regulatory environment and enhanced confidence in the sector. As a result, Q3 highlighted Bitcoin’s growing safe-haven appeal, its entry into the financial mainstream, and the increased clarity and security offered by evolving regulations and widespread adoption by both institutional and retail investors.

Geopolitical situation

In Q3 2025, the Israel–Hamas conflict saw a dramatic escalation in both tactics and geography. Notably, in early September Israel launched its first known airstrike inside Qatar, targeting a residential compound in Doha where senior Hamas figures were reportedly meeting, drawing international condemnation for breaching Gulf sovereignty. Diplomacy attempted a comeback too, at the end of July, an international conference on the two-state solution was held in New York, focusing on disarmament, hostages, Palestinian governance, and reconstruction planning. Meanwhile, on the Eastern European front, Russia made progress to capture more Ukrainian territory. Frequent drone and missile attacks persisted across frontline regions, with Russian strikes targeting Ukrainian infrastructure and towns while Ukraine countered with raids deep into Russian-held areas. The cumulative effect of the conflict was extended volatility in global security dynamics and significant strain on diplomatic and humanitarian channels across continents.

Key News & Events in Q3 2025

UK

• The UK’s annual inflation rate remained steady at 3.8% in August 2025, unchanged from July and still hovering around levels last seen in January 2024. This outcome was broadly anticipated by market participants, suggesting that price pressures are persisting but have not accelerated further in recent months. The stability in inflation reflects a balance between rising costs in sectors such as food and services and moderating pressures elsewhere, helping to anchor expectations for future price developments.

• At its September meeting, the Bank of England’s Monetary Policy Committee voted 7–2 to keep the Bank Rate unchanged at 4%. Most members supported maintaining the current rate, citing ongoing uncertainties in the economic outlook and the importance of consolidating recent gains in price stability. However, two members favoured a 25-basis points reduction to 3.75%, indicating some divergence in views regarding the urgency of monetary easing. Notably, the Bank of England did implement a single rate cut during the third quarter, lowering the Bank Rate to 4% on 07 August, as part of its ongoing efforts to support economic growth while addressing inflation risks.

• Economic growth in Britain continued at a moderate pace, with gross domestic product expanding by 0.3% quarter-on-quarter in the second quarter of 2025, matching the preliminary estimate. This followed a stronger 0.7% increase in the first quarter, suggesting that growth momentum has softened but remains positive. The performance was underpinned by resilience in key sectors such as services and manufacturing, although headwinds from global uncertainties and higher borrowing costs have weighed on overall activity.

• The United Kingdom’s labour market remained stable, with the unemployment rate holding at 4.7% in the three months to July 2025. This figure was unchanged from the previous period and aligned with market expectations, signalling that employment conditions have not deteriorated despite the challenges from elevated inflation and slower economic growth. The steadiness in the job market reflects a degree of resilience among businesses and workers, although policymakers continue to monitor for any signs of slack or increased joblessness as economic conditions evolve.

US

• The US annual inflation rate accelerated to 2.9% in August 2025, representing the highest level recorded since January of the same year. This uptick followed a period of relative stability, with inflation holding steady at 2.7% in both June and July, and was broadly anticipated by market participants. The increase in price pressures was largely attributed to rising costs in key categories such as housing, services, and energy, which offset more moderate gains or declines elsewhere in the consumption basket. Persistent inflation, even at these modestly elevated levels, continues to influence both consumer sentiment and monetary policy decisions.

• In response, the Federal Reserve took action at its September 2025 policy meeting, opting to reduce the federal funds rate by 25 basis points. This move brought the target range down to 4.00%–4.25%, a decision that was widely expected by analysts and financial markets. Notably, this was the first rate cut since December 2024, signalling a shift towards more accommodative policy as the central bank seeks to support sustained economic growth while keeping inflation anchored near its target. The Fed’s decision reflects a nuanced balance between controlling inflation and providing relief to borrowers amid changing economic conditions.

• On the growth front, the US economy posted an impressive annualised expansion of 3.8% in the second quarter of 2025. This figure exceeded the previous second estimate of 3.3% and marked the strongest quarterly performance since the third quarter of 2023. The upward revision was primarily attributed to robust consumer spending, which remained a key driver of economic activity despite persistent cost-of-living pressures. This resilience in household demand highlights the ongoing strength of the US consumer sector and, in some segments, wage growth.

• However, the labour market showed signs of softening, with the national unemployment rate edging up to 4.3% in August 2025, compared to 4.2% in July. This represented the highest rate of joblessness since October 2021, although it remained within the range anticipated by economists. The slight increase suggests that while employment conditions remain broadly favourable, there are emerging signs of slack, particularly in sectors sensitive to interest rate changes and global economic shifts. Policymakers and market observers continue to monitor these trends closely, as any sustained rise in unemployment could pose challenges to ongoing economic momentum.

Europe

• Euro area consumer price inflation increased to 2.2% in September 2025, marking a rise from the steady 2.0% rate observed over the preceding three months. This latest figure takes inflation slightly above the European Central Bank’s (ECB) 2.0% mid-point target, as per preliminary estimates. The uptick in inflation suggests that price pressures within the eurozone are persisting, despite recent efforts by policymakers to maintain stability. The modest acceleration in consumer prices can be attributed to higher costs in sectors such as energy and services, which have offset softer trends in other categories. The move above the ECB’s target underscores ongoing challenges in containing inflationary pressures, particularly at a time when other advanced economies are also grappling with similar issues.

• After a series of rate cuts over the previous few quarters, the European Central Bank opted to keep its three key interest rates unchanged in Q3, maintaining the deposit facility at 2.00%, the main refinancing rate at 2.15%, and the marginal lending rate at 2.40%. This decision, which was in line with market expectations, reflects the ECB’s cautious approach as it seeks to strike a balance between controlling inflation and supporting economic growth. By holding rates steady, the ECB aims to provide stability for financial markets and households, while continuing to monitor the evolving inflation landscape across member states.

• Turning to economic activity, the Gross Domestic Product (GDP) in the Euro Area expanded by just 0.10% in the second quarter of 2025 compared to the previous quarter. This marginal increase highlights the subdued pace of economic growth across the region, as lingering uncertainty and external headwinds continue to weigh on business investment and consumer spending. The modest expansion suggests that while the eurozone economy has avoided contraction, momentum remains fragile, and policymakers may need to consider additional measures should growth continue to stagnate.

• The labour market also showed signs of softening, as the Euro Area’s seasonally adjusted unemployment rate edged up to 6.3% in August 2025, rising from an all-time low of 6.2% recorded in July. This slight increase ran counter to forecasts that expected unemployment to remain steady, indicating a potential turning point in labour market dynamics. The uptick in joblessness could reflect a combination of slower job creation and greater caution among employers amid an uncertain economic outlook. Nevertheless, the unemployment rate remains historically low by eurozone standards, suggesting that, for now, the region’s labour market is still relatively resilient, albeit facing new pressures as growth moderates.

China

• China’s consumer prices registered a year-on-year decline of 0.4% in August 2025, marking a notable drop following a flat reading in July. This decrease was sharper than market expectations, which had anticipated a milder 0.2% fall. The August figure represents the fifth occurrence of consumer price deflation in China so far this year, and it is the most pronounced decline since February 2025. The ongoing pattern of deflation points to continued weakness in domestic demand, with falling prices exerting downward pressure on profit margins for producers and retailers alike. It also underscores the challenges facing policymakers as they attempt to revive consumption and restore price stability amidst a sluggish recovery environment.

• In response to these persistent deflationary pressures, the People’s Bank of China (PBOC) opted to maintain its key lending rates at record lows for the fourth consecutive month in September 2025, a move that was widely anticipated by market participants. By keeping borrowing costs at historically low levels, the PBOC aims to encourage lending and investment activity, while also supporting households and businesses struggling with subdued price growth. This ongoing accommodative stance reflects the central bank’s commitment to sustaining economic momentum and countering the risks posed by weak consumer and producer prices.

• Despite a challenging price environment, China’s economy demonstrated resilience in the second quarter of 2025. Gross Domestic Product (GDP) expanded by a seasonally adjusted 1.1% compared to the previous quarter, outperforming market forecasts of 0.9%. Although this represented a modest slowdown from the 1.2% growth recorded in the first quarter, the result highlights the effectiveness of a series of policy support measures rolled out by Beijing. These included interest rate reductions and increased liquidity injections, both intended to offset the negative impact of trade tariffs and to stimulate economic activity. The stronger-than-expected GDP growth suggests that these interventions have provided a meaningful boost to output, even as broader structural headwinds persist.

• However, not all economic indicators were positive. China’s surveyed unemployment rate ticked up to 5.3% in August 2025, compared to both the previous month’s reading and market expectations of 5.2%. This increase brought the joblessness rate to its highest level since February, signalling some ongoing softness in the labour market. The rise in unemployment may reflect continued uncertainty in the economic outlook, with employers remaining cautious about expanding their workforce amid an uneven recovery. Together, these trends illustrate the complex landscape confronting Chinese policymakers as they seek to balance growth, employment, and price stability in the months ahead.

To learn more about our investment approach and how we can help you, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.