Overview

In October 2025, global financial markets were shaped by an intersection of macroeconomic pressures, renewing tariff tensions, and heightened geopolitical anxieties. Slowing growth and sticky core inflation in major economies prompted cautious monetary policy signals, while the International Monetary Fund raised its global growth forecast but warned of looming trade-risks. On the trade front, the spectre of expanded tariffs, especially between the United States and China, and broader supply-chain disruption worries weighed on investor sentiment. Geopolitical flashpoints added further uncertainty, elevating safe-haven flows into precious metals, bonds, and the dollar, while equity markets exhibited increased volatility as risk-premiums widened. Together, these elements signalled a shift from the earlier summer optimism toward a more guarded stance by investors, who weighed the prospects for growth against a heightened backdrop of trade friction and geopolitical risk.

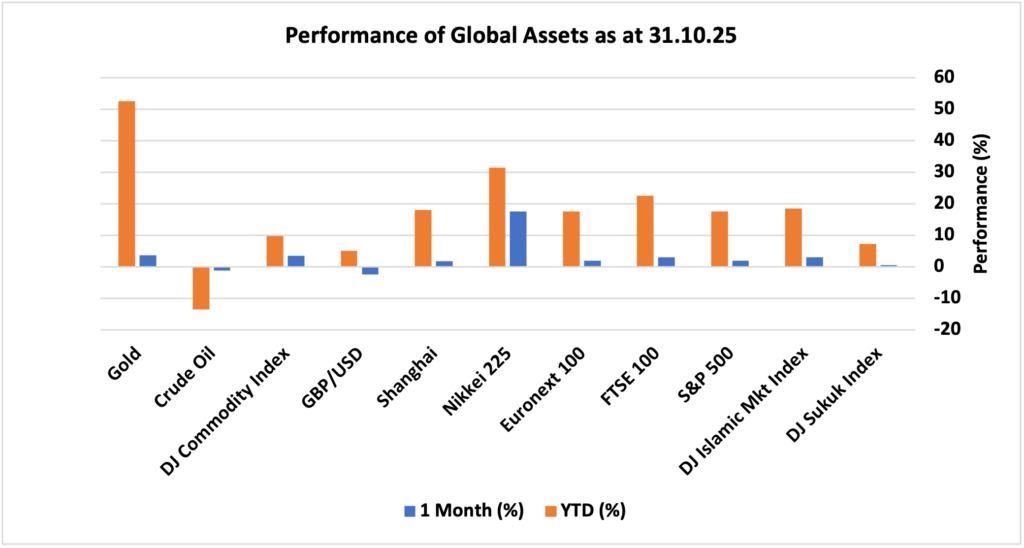

Looking at the performance of major asset classes in October 2025, global financial markets continued a robust rally, with leading asset classes posting positve gains and ending the month on solid ground, despite rising concerns over macroeconomic factors and technology sector valuations. Equities across major regions posted positive gains in October, led especially by the Japan Nikkei 225 index (+17.6%), UK FTSE 200 +3%, US S&P 500 index (+2%), and Europe (Euronext 100 index +2%), while China Shanghai index rose more modestly with +1.85%. On the Islamic investment front, the Dow Jones Islamic Market Index recorded a gain of +3.05% in October. This mirrored the broader global equity trend and was buoyed by risk-on sentiment, albeit tempered by credit concerns. The huge surge in Japanese equities reflected investor optimism around pro-growth policies under the newly ascendant government, a weaker yen and expectations of fiscal stimulus. DJ sukuk index gained +0.61% amid lowering interest rates/softening yields. Commodities also advanced as gold added another 3.6% while crude oil dipped slightly (-1.15%), and the U.K. pound remained under pressure, which lost 2.42% to U.S. Dollar. The backdrop was one of improving risk sentiment thanks to trade-talks optimism and changing monetary policy stances as focus shifting towards employment outlook despite inflation being a concern to many market participants. Furthermore, the positive performance across financial assets was driven by the hopes of rate cuts by the U.S. Federal Reserve and by strong earnings in tech/AI-linked firms.

The following snapshot provides a detailed breakdown of the performance of different asset classes in October 2025, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in October

UK

• The annual inflation rate in the UK held firm at 3.8% in September 2025, remaining unchanged for the third consecutive month and coming in slightly below market forecasts of 4%. This stability in consumer prices suggests that underlying inflationary pressures may be easing, despite ongoing concerns about cost-of-living increases and the impact on household budgets. The data indicates a degree of resilience in the face of global volatility, although persistent inflation remains a key consideration for policymakers and businesses alike.

• At its latest meeting, the Bank of England’s Monetary Policy Committee (MPC) voted seven to two to maintain the Bank Rate at 4%. While a majority of members supported holding rates steady, two members advocated for a 25 basis point cut to 3.75%, signalling some divergence in views about the appropriate path for monetary policy given the current economic landscape. The committee also voted by the same margin to slow the pace of quantitative tightening, opting to reduce gilt holdings by £70 billion over the next twelve months, which would bring the total down to £488 billion. This decision reflects a cautious approach, balancing the need to manage inflation expectations with supporting economic growth and financial stability.

• Meanwhile, the UK’s labour market showed signs of softening, as the unemployment rate rose to 4.8% in the three months to August 2025. This was higher than both the market expectation of 4.7% and the previous month’s reading in July, marking the highest level since the three months to June 2021. The increase in joblessness could signal emerging challenges in the employment landscape, potentially influencing future policy decisions as the Bank of England weighs the trade-offs between inflation control and supporting the jobs market.

US

• The annual inflation rate in the United States climbed to 3% in September 2025, marking the highest reading since January of the same year. This uptick represents a slight acceleration from the 2.9% recorded in August and came in just below market forecasts of 3.1%. The rise in consumer prices signals ongoing inflationary pressures, which have persisted despite efforts by policymakers to stabilise costs. Factors such as resilient consumer demand and elevated energy prices have contributed to the upward movement in inflation, leaving households and businesses facing increased costs across a range of goods and services.

• In response to these economic conditions, the Federal Reserve took further action at its October 2025 meeting, lowering the federal funds rate by 25 basis points to a target range of 3.75%–4.00%. This decision was widely anticipated by market participants and followed a similar rate cut implemented in September, thereby reducing borrowing costs to their lowest level since 2022. The consecutive rate reductions reflect the Fed’s ongoing commitment to supporting the economy amid persistent inflation and signs of softening in the labour market. By making borrowing cheaper, the central bank aims to encourage investment and spending, while also monitoring the risk of reigniting inflation.

• Labour market data showed some signs of strain, as the US unemployment rate increased to 4.3% in August 2025, up from 4.2% in the prior month. This change is in line with market expectations and represents the highest proportion of joblessness since October 2021. The rising unemployment rate suggests that businesses may be exercising greater caution in hiring decisions amid economic uncertainty, potentially reflecting the impact of tighter monetary policy and evolving demand conditions. As policymakers weigh the trade-offs between maintaining price stability and supporting employment, the interplay between inflation and joblessness will remain a central consideration in shaping future monetary policy decisions.

Europe

• Euro area consumer price inflation eased to 2.1% in October 2025, aligning with market expectations and marking a slight decline from the 2.2% recorded in September. This downward movement brings inflation closer to the European Central Bank’s (ECB) official target of 2%, according to preliminary figures. The moderation in inflation suggests that price pressures across the eurozone are gradually subsiding, likely reflecting fading effects of previous supply chain disruptions and stabilising energy prices. Such developments are positive for households and businesses, as they may help alleviate concerns about rising living costs and support consumer confidence.

• In response to these trends, the European Central Bank opted to maintain interest rates at their current levels for the third consecutive meeting in October. This decision signals the ECB’s confidence in the resilience of the eurozone economy and its assessment that inflation is moving in the right direction. The main refinancing rate remained at 2.15%, while the deposit facility rate was held steady at 2.0%. By keeping rates unchanged, the ECB is aiming to support ongoing economic growth while ensuring that inflation continues its gradual return towards target. The central bank also indicated that it would closely monitor incoming data to assess whether further adjustments are needed in the future.

• Economic growth in the eurozone showed modest improvement, with the region’s economy expanding by 0.2% quarter-on-quarter in the third quarter of 2025. This marks an acceleration from the 0.1% growth reported in the previous quarter and slightly exceeds market expectations of a 0.1% rise, according to a flash estimate. The uptick in growth reflects a degree of resilience in euro area activity, supported by steady consumer spending and improving business sentiment, despite ongoing global uncertainties and geopolitical tensions.

• Labour market conditions remained stable, as the seasonally adjusted unemployment rate in the Euro Area held at 6.3% in September 2025—unchanged from both August and July and in line with market forecasts. This steadiness suggests that the jobs market is maintaining its footing, with no significant increase in joblessness despite the broader economic challenges. The stable unemployment rate, alongside easing inflation and slightly stronger growth, provides policymakers with some reassurance as they navigate the complex balance between supporting recovery and managing inflation risks.

China

• China’s consumer prices declined by 0.3% year-on-year in September 2025, representing a more pronounced drop than market expectations, which had forecast a 0.1% decrease. However, this fall was slightly less severe than the 0.4% contraction recorded in August. The ongoing decline in consumer prices highlights lingering deflationary pressures in the Chinese economy, with weak consumer demand and subdued spending continuing to weigh on price growth across key sectors.

• In response to these economic conditions, the People’s Bank of China (PBoC) opted to maintain key lending rates at record lows for the fifth consecutive month in October, a move that aligned with widespread market expectations. This decision followed the PBoC’s choice to leave the seven-day reverse repo rate unchanged the previous week, which now serves as the central bank’s primary policy tool. The monetary stance comes amid the U.S. Federal Reserve’s renewed shift towards monetary easing in September and persistent Sino-US trade tensions, both of which have influenced China’s policy approach. As a result, the one-year Loan Prime Rate (LPR)—used as a benchmark for most corporate and household borrowing—remained steady at 3.0%. Similarly, the five-year LPR, which underpins mortgage rates, was held at 3.5%, providing continued support to the property market and broader credit conditions.

• China’s economy demonstrated resilience in the third quarter of 2025, with GDP increasing by 1.1% quarter-on-quarter. This growth surpassed market expectations of a 0.8% rise and followed a marginally revised 1.0% gain in the second quarter. The stronger-than-anticipated performance can be attributed to a range of policy measures implemented by Beijing, including targeted liquidity injections aimed at stabilising credit markets and mitigating the impact of deflation. These efforts have helped bolster economic activity despite ongoing challenges, such as sluggish domestic demand and uncertainties in the global economic environment.

• Labour market conditions also showed improvement, as China’s surveyed unemployment rate edged down to 5.2% in September 2025. This figure was in line with market expectations and marked a decrease from August’s six-month high of 5.3%. The modest reduction in unemployment suggests that policy support and stabilising economic growth are beginning to have a positive effect on job creation and employment prospects within the country.

Others

• Japan’s annual inflation rate rose to 2.9% in September 2025, up from August’s ten-month low of 2.7%. This uptick signals a re-acceleration in consumer prices, reflecting ongoing cost pressures in key sectors such as energy, food, and services. Despite this renewed rise in inflation, the Bank of Japan (BoJ) opted to keep its benchmark short-term rate unchanged at 0.5% during its October 2025 policy meeting, maintaining borrowing costs at their highest level since 2008. The decision to extend the pause in its monetary tightening—unchanged since the last rate hike in January—suggests the BoJ remains cautious, aiming to balance the need to support economic recovery with concerns about persistent price increases. Policymakers indicated they would continue to monitor both domestic wage growth and global economic trends before considering any further adjustments to their interest rate stance.

• Turning to North America, the annual inflation rate in Canada climbed to 2.4% in September 2025, rising from 1.9% in August and surpassing market expectations of a 2.3% increase. This marked the highest inflation reading since February, driven mainly by higher costs in housing, transport, and food. Responding to these developments and ongoing economic uncertainties, the Bank of Canada decided to lower its benchmark overnight rate by 25 basis points to 2.25% during its October 2025 meeting, a move widely anticipated by financial markets. The central bank signalled that it is likely finished with its current rate-cutting cycle, provided that its baseline economic projections remain intact amid the prevailing uncertainty. This cautious stance reflects the bank’s effort to strike a balance between supporting economic growth and preventing inflation from accelerating beyond target levels.

• Elsewhere, the Bank of Russia made a notable policy move by cutting its benchmark interest rate by 50 basis points to 16.5% on 24 October 2025, marking the fourth consecutive rate cut. This decision diverged from market expectations, which had anticipated rates to remain on hold. The central bank’s continued easing reflects efforts to stimulate economic activity in the face of slowing growth and moderating inflationary pressures, though it also highlights ongoing challenges in managing the country’s monetary environment.

• In the cryptocurrency markets, volatility remained a defining feature throughout October. Bitcoin, the world’s largest digital currency, experienced significant price swings over the month. It began October trading at $114,600, surged to an all-time high of $124,900 during the first half of the month, and ultimately ended October at approximately $109,500 per token. These sharp fluctuations underscore the continued uncertainty and speculative activity within the digital asset space, with market sentiment driven by shifting regulatory developments, changing investor appetite, and broader macroeconomic factors.

• A ceasefire in Middle East came into effect in October after Israel and Hamas agreed to phase one of a US-backed peace plan.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.