Overview

In November 2025, global financial markets have been buffeted by a complex interplay of macroeconomic pressures, trade-policy shifts and geopolitical risk. Slowing growth, with inflation still sticky in many economies, has dampened investor confidence, while renewed tariff measures and trade-policy uncertainty have disrupted supply-chains and raised cost pressures. At the same time, lingering geopolitical tensions and policy ambiguity have heightened volatility, prompting many investors to reappraise risk and shift toward safer assets or cut exposure. Meanwhile, some pockets of the market, particularly sectors positioned to benefit from structural trends such as AI, infrastructure and fiscal stimulus in major economies have held up better, offering a counterweight to the broader uncertainty. The result is a choppy, uneven market landscape, gains in some regions and assets, but broad undercurrents of caution and volatility.

On 26 November 2025, Chancellor Rachel Reeves delivered the UK Autumn Budget to MPs, unveiling a sweeping fiscal package aimed at raising roughly £26 billion by the end of the decade, pushing the UK’s tax burden to a post-war high. Key measures include a freeze on income-tax and National Insurance thresholds (extending until 2030–31), new levies on dividends, savings and property income, and an annual “mansion tax” on homes worth over £2 million. At the same time, Reeves pledged to ease cost-of-living pressures by cutting average household energy bills by around £150 annually, lifting the two-child benefit cap, increasing the minimum wage, and boosting State Pension, a mixture of fiscal tightening and social support. The Budget reflects a clear strategy as to consolidate public finances while protecting vulnerable households, but it also signals tougher times ahead for savers, middle-income earners and property owners.

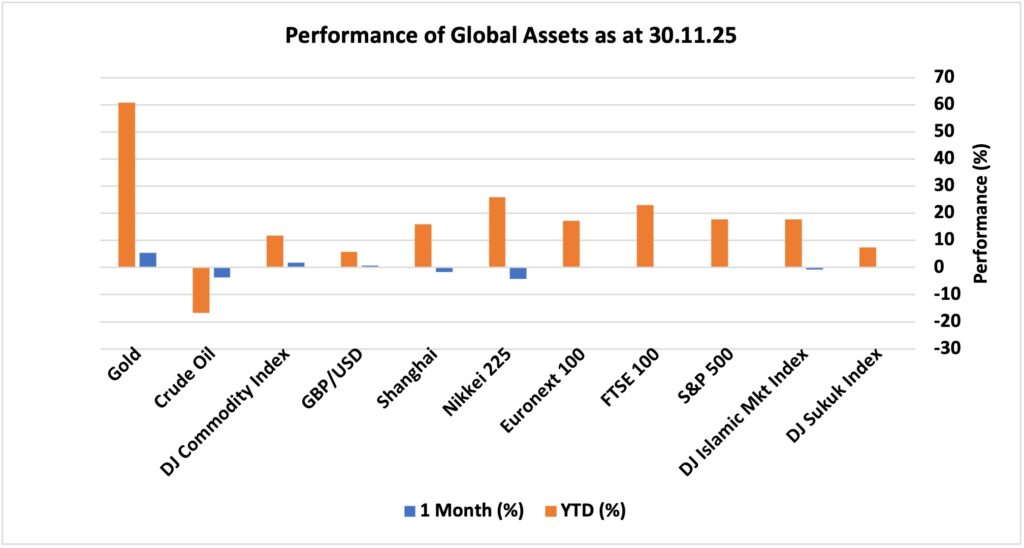

Looking at the performance of major asset classes, most of them ended the month flat or down amid U.S govt shutdown and AI driven tech sector valuation concerns. The U.S. equity market benchmark S&P 500, UK FTSE 100 index, and European equity market Euronext 100 all ended the month largely flat. The benchmark for shariah-compliant investments, DJ Islamic market index, fell by 0.67% while Chinese Shanghai index dropped by 1.67% in the month despite a series of stimulus packages announced by the authorities, but investors still want more from the government on fiscal and structural side of things as fundamentals need to improve to support a sustained growth in the financial markets. Japan Nikkei 225 index plunged over 4% amid rising tensions between China and Japan over Taiwan issue. Amid uncertainties around monetary policies, yields moved little and DJ Sukuk Index end the month with 0.16% upside. Gold continued to shine as a strong bet for safe haven 5.4% surge. Lastly, UK pound gained 0.69% against US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in November 2025, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in November:

UK

• The UK’s annual inflation rate moderated to 3.6% in October 2025, marking its lowest point in four months and declining from the 3.8% rate that persisted throughout the previous quarter. This easing of inflation suggests a gradual unwinding of price pressures, potentially reflecting stabilisation in energy costs, improved supply chain conditions, and a slight shift in consumer demand. However, while the reduction offers some relief to households and businesses, it remains above the Bank of England’s long-term target, indicating that inflationary challenges are not yet fully resolved.

• At its meeting on 5 November, the Bank of England’s Monetary Policy Committee (MPC) opted to maintain the Bank Rate at 4%, with a narrow 5–4 vote. This outcome was largely anticipated by financial markets, yet the split decision reveals a growing divergence within the committee regarding the appropriate policy response. Notably, four members advocated for a 25 basis point cut to 3.75%, signalling an increasing appetite for monetary easing amid signs of economic softness. The close vote underscores the balancing act faced by policymakers: weighing persistent inflation against the need to support growth and employment, as well as managing expectations in a climate of heightened uncertainty.

• Economic growth in the UK remained subdued during the third quarter of 2025, with GDP expanding by just 0.1%, according to preliminary estimates. This represents a slowdown from the 0.3% growth recorded in the second quarter and falls short of market expectations of 0.2%. The sluggish pace of expansion points to underlying weaknesses in key sectors, including manufacturing and retail, possibly exacerbated by ongoing global trade disruptions and cautious business investment. The marginal growth also suggests that the UK economy is struggling to gain momentum, with consumer confidence and spending likely constrained by cost-of-living concerns and rising borrowing costs.

• Labour market conditions in the UK showed signs of strain, as the unemployment rate edged up to 5.0% in the third quarter of 2025. This marks the highest level since the three months to May 2021 and slightly exceeds market forecasts of 4.9%. The increase in unemployment may be attributed to a combination of slower economic activity, corporate restructuring, and lingering effects from earlier shocks. Although the labour market has displayed resilience in recent years, the uptick highlights emerging vulnerabilities, particularly for younger workers and those in sectors undergoing transition. Policymakers may need to consider targeted support measures to prevent further deterioration and to encourage job creation as the economic recovery remains fragile.

US

• Latest inflation data not available for the U.S. due to govt shutdown.

• The Fed had no meeting in November to decide on interest rates.

• Latest GDP data not available for the U.S. due to govt shutdown.

• Latest unemployment data not available for the U.S. due to govt shutdown.

Europe

• Euro area consumer price inflation increased to 2.2% in November 2025, edging up from 2.1% in October and surpassing market expectations, which had anticipated a repeat of the previous month’s rate at 2.1%. This modest acceleration in inflation suggests that price pressures remain persistent across the region, likely driven by factors such as energy costs, supply chain adjustments, and resilient demand in certain sectors. The uptick marks the highest inflation reading in recent months, indicating that the Eurozone is still contending with the after-effects of earlier price surges and ongoing economic uncertainties.

• In response to these conditions, policymakers at the European Central Bank (ECB) maintained their stance on interest rates, agreeing that keeping rates unchanged was the most prudent course of action given the elevated levels of uncertainty in the economic outlook. According to the minutes of the October 29–30 meeting, the majority of ECB members felt that no further policy easing was required at this time, with some even suggesting that the current interest rate environment could be sustained for longer than previously anticipated. This cautious approach highlights the ECB’s commitment to balancing price stability with the need to support growth, while remaining vigilant to any signs of renewed inflationary pressure or shifts in economic momentum.

• The Eurozone economy demonstrated modest growth in the third quarter of 2025, expanding by 0.2% on a quarter-on-quarter basis, as revealed in the second estimate. This was an improvement compared to the 0.1% growth recorded in the preceding quarter, and it reflects a gradual recovery despite the challenging backdrop of global uncertainties and mixed performance among member states. The slight uptick in GDP growth was underpinned by improvements in industrial output, increased consumer spending, and supportive fiscal measures in some countries. However, the pace of expansion remains subdued, underscoring the fragility of the recovery and the need for continued policy support.

• Labour market conditions in the Euro Area remained relatively stable, with the seasonally adjusted unemployment rate holding steady at 6.4% in October 2025, identical to September’s revised figure. Although this reading was marginally above market forecasts of 6.3%, it points to a labour market that is showing resilience in the face of ongoing economic headwinds. The stability in unemployment suggests that businesses have largely maintained staffing levels, even as growth remains moderate. Nevertheless, pockets of weakness persist, particularly in sectors still recovering from the pandemic and among younger workers, highlighting areas where targeted policy interventions may be required to foster more inclusive labour market improvements.

China

• China’s consumer prices increased by 0.2% year-on-year in October 2025, surpassing market expectations, which had anticipated no change following a 0.3% decline in the previous month. This marks the first rise in consumer inflation since June, and the quickest pace recorded since January. The upturn in inflation was largely driven by higher food and energy prices, as well as a gradual recovery in domestic demand. The rebound signals a potential shift in price dynamics after a period of disinflation, reflecting tentative stabilisation in consumer spending and underlying economic activity.

• Against this backdrop, the People’s Bank of China (PBoC) maintained its key lending rates at record lows for the sixth month running in November, as widely expected by market participants. By keeping rates unchanged, the central bank aims to support economic growth without fuelling excessive inflation, balancing the need for stimulus with concerns about financial stability. The decision suggests that policymakers remain cautious, preferring to observe further economic developments before adjusting monetary policy.

• On the growth front, China’s gross domestic product (GDP) expanded by 1.1% quarter-on-quarter in the third quarter of 2025, exceeding forecasts of a 0.8% increase. This stronger-than-anticipated performance builds on a slightly revised 1.0% gain in the second quarter, indicating that the economy is gaining momentum despite global uncertainties and ongoing challenges within the property and export sectors. The positive GDP reading reflects improvements in industrial production, retail sales, and government-led infrastructure investment, all of which have contributed to the recent uplift.

• Meanwhile, the country’s surveyed urban unemployment rate fell to 5.1% in October 2025, contrary to expectations that it would remain unchanged at September’s 5.2%. While the decrease points to a strengthening labour market and ongoing job creation in the urban sector, it also highlights the uneven nature of the recovery, with youth unemployment and underemployment remaining areas of concern. Continued efforts to boost employment opportunities and support vulnerable groups will be critical as China navigates its post-pandemic economic transition.

Others

• Japan’s annual inflation rate edged up to 3.0% in October 2025, rising marginally from 2.9% in September. This marks the highest inflation reading for the country since July, highlighting persistent upward pressure on consumer prices. The increase may be attributed to factors such as higher energy costs, currency movements, and ongoing supply chain disruptions. Policymakers are likely to monitor these trends closely, as sustained elevation in inflation could influence decisions on monetary policy and interest rates going forward.

• Meanwhile, the headline inflation rate in Canada fell to 2.2% in October 2025, down from 2.4% in September. This gradual decline suggests that price pressures are easing, with inflation loosely converging towards the Bank of Canada’s 2% target over the near term, as projected in its baseline scenario. The downward movement in inflation may reflect moderating energy prices, stabilising food costs, and the impact of tighter monetary policy. This trend provides the central bank with more flexibility to manage interest rates and support economic stability, while remaining vigilant to any renewed inflationary pressures.

• In Russia, inflation continued its downward trajectory, decreasing to 7.70% in October 2025 from 8.0% in September. This notable reduction reflects the effect of recent monetary tightening measures and possibly improved supply conditions. Despite the decrease, inflation remains elevated compared to pre-pandemic levels, suggesting that the Russian central bank may maintain a cautious approach to policy adjustments until further stabilisation is achieved.

• Turning to digital assets, Bitcoin, the world’s largest cryptocurrency, experienced a significant decline in value over the course of November 2025. The token started the month trading at around $109,500 and ended November at approximately $90,000 per token, representing a substantial drop. This volatility could be attributed to a range of factors, including shifting investor sentiment, regulatory developments, and broader market uncertainty. The pronounced fall in Bitcoin’s price underscores the risks associated with investing in digital currencies and the importance of closely monitoring market conditions.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.