Overview

In March 2026, global financial markets were heavily influenced by a sharp escalation in geopolitical tensions, evolving trade policies, and shifting macroeconomic expectations. The outbreak and intensification of conflict in the Middle East triggered a surge in energy prices, with oil rising dramatically and fuelling renewed inflation concerns across major economies. This energy shock complicated the global disinflation narrative, prompting central banks to largely pause rate cuts and maintain cautious policy stances amid heightened uncertainty. At the same time, renewed trade frictions, particularly involving the US and key trading partners, added pressure to global manufacturing and supply chains, dampening business confidence. Equity markets experienced increased volatility and drawdowns, while safe-haven assets like the US dollar saw strong demand. Overall, March was characterised by rising stagflation risks, with markets balancing resilient growth signals against escalating geopolitical shocks and policy uncertainty.

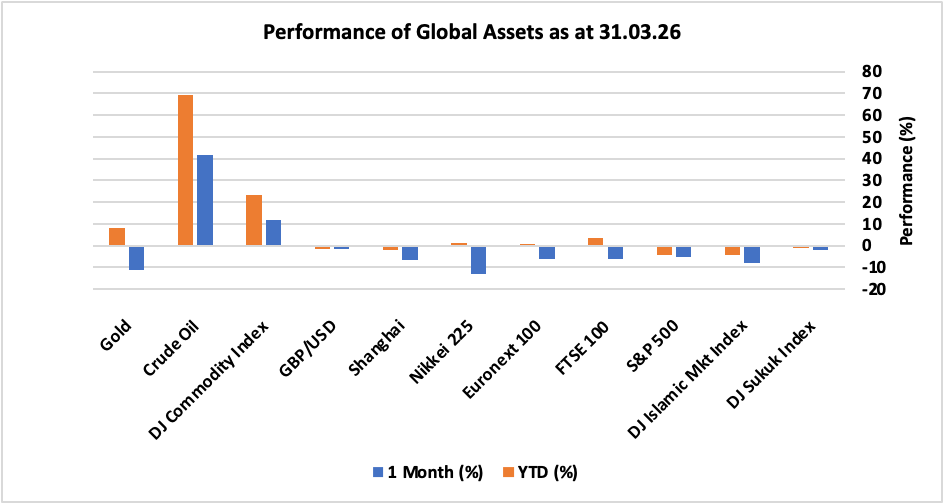

Looking at the performance, all major global financial assets, except crude oil, experienced drawdown and negative momentum amid geopolitical fears resulting from War in Middle East, despite resilient corporate earnings and positive developments in AI theme. Asian and European equity markets recorded significant losses as Japan’s Nikkei 225 led the fall-down with negative returns of over 13% followed by China’s Shanghai index that tumbled 6.5%. While in Europe, UK FTSE 100 and EU Euronext 100 plunged 6.20% and 6.10%, respectively, largely driven by higher energy prices and potential shocks. US S&P 500 declined by roughly 5% whereas DJ Islamic Markets Index booked negative 7.7% returns during the month. DJ Sukuk Index ended the month down 2.17% amid rising yields. In commodities, DJ Commodity index climbed nearly 12% driven by 41.5% surge in Crude oil prices, although gold plunged by 11% on US dollar strength, which appreciated 1.74% against UK pound.

The following snapshot provides a detailed breakdown of the performance of different asset classes in March 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in March:

UK

- The annual inflation rate in the UK held steady at 3% in February 2026, matching January’s figure and aligning with market forecasts. This stability suggests that price pressures have not intensified further, even as households continue to face elevated costs for essentials. The consistent inflation rate provides some reassurance to policymakers and investors, indicating that previous monetary policy measures may be helping to anchor expectations and prevent a resurgence in inflationary pressures.

- In its March 2026 meeting, the Bank of England’s Monetary Policy Committee unanimously decided to maintain the Bank Rate at 3.75%. This decision came against a backdrop of heightened global uncertainty, with the ongoing conflict in the Middle East causing significant volatility in energy and commodity markets. The resultant surge in fuel and utility prices has led to increased household expenses, while businesses are grappling with rising input costs, impacting profit margins and potentially influencing wage negotiations and investment decisions.

- The UK unemployment rate remained at 5.2% for the three months to January 2026, slightly better than the anticipated 5.3%. However, this figure still marks the highest unemployment level since the three months ending February 2021, reflecting ongoing challenges in the labour market. While the rate’s stability may indicate that job losses have slowed, persistent unemployment at this level could signal underlying structural issues, such as skills mismatches or sectoral weaknesses, which may require targeted policy responses to support job creation and economic resilience.

US

- The annual inflation rate in the US remained steady at 2.4% in February 2026, unchanged from the previous month and matching market expectations. This figure represents the lowest level seen since May 2025, indicating that price pressures have continued to moderate following earlier peaks. The stability in inflation suggests that earlier tightening measures by the Federal Reserve may be having the intended effect, helping to anchor expectations and maintain consumer purchasing power. While headline inflation has not accelerated, underlying factors such as housing and services continue to exert influence, keeping policymakers attentive to potential upside risks.

- At its March 2026 meeting, the Federal Reserve decided to leave the federal funds rate unchanged within the 3.5%–3.75% target range for a second consecutive session. This move was widely anticipated by markets and underscores the Fed’s cautious stance amid persistent economic uncertainties. Policymakers noted that economic activity continues to expand at a solid pace, despite job gains remaining subdued and inflation still somewhat elevated compared to target levels. The decision highlights the balancing act faced by the Fed, as it aims to support growth without reigniting inflation, especially against the backdrop of global volatility and mixed domestic data.

- The US economy expanded at an annualised rate of just 0.7% in the fourth quarter of 2025, marking the weakest quarterly performance since the contraction recorded in the first quarter of the same year. This result was notably below the advance estimate of 1.4%, reflecting downward revisions in several key areas including exports, consumer spending, government expenditure, and investment. The softening growth momentum signals that the US economy is facing headwinds such as tighter financial conditions, cooling domestic demand, and external pressures from global trade disruptions and persistent geopolitical uncertainty.

- The US unemployment rate edged higher to 4.4% in February 2026, up from 4.3% in January and slightly above market forecasts. This uptick brings the rate closer to the four-year high of 4.5% observed in November 2025. The increase in unemployment suggests ongoing challenges in the labour market, with job creation slowing in several sectors and more Americans seeking work. While the rise is not dramatic, it reflects underlying vulnerabilities that could impact wage growth, consumer confidence, and overall economic resilience if the trend persists over the coming months.

Europe

- Euro area annual inflation rose sharply to 2.5% in March 2026, up from 1.9% in February and just below market expectations of 2.6%, according to a preliminary estimate. This represents the highest inflation rate observed since January 2025, and notably pushes the figure above the European Central Bank’s (ECB) official 2% target. The surge was primarily driven by a significant increase in energy costs, which soared 4.9% year-on-year. This was the first annual rise in energy prices for nearly a year, and the sharpest since February 2023. The conflict in the Middle East has played a key role in this escalation, disrupting energy supply chains and contributing to price volatility across the region. Elevated energy prices have knock-on effects across the broader economy, increasing costs for businesses and households and feeding through into higher prices for goods and services.

- The European Central Bank (ECB) opted to keep interest rates unchanged at its March 2026 meeting, signalling its ongoing commitment to achieving price stability and returning inflation to its 2% medium-term target. The main refinancing rate remains at 2.15%, the deposit facility at 2.0%, and the marginal lending rate at 2.4%. Policymakers emphasised that the ongoing war in the Middle East has substantially increased uncertainty in the economic outlook, introducing upside risks to inflation and downside risks to growth. As a result, the ECB is maintaining a cautious stance, closely monitoring developments and remaining prepared to adjust its policy if necessary to safeguard both inflation targets and economic stability.

- The Euro Area economy expanded by just 0.2% in the fourth quarter of 2025, which was below the earlier estimate of 0.3% and represented a slowdown from the 0.3% growth recorded in the third quarter. This limited momentum is indicative of the region’s modest recovery, despite several supportive factors such as easing inflation and lower interest rates. The economy demonstrated resilience in the face of headwinds, including US trade tariffs imposed on EU imports, which have affected export volumes and business confidence. The subdued growth underscores ongoing challenges such as external trade pressures, geopolitical risks, and the need for continued structural reform within member states to bolster economic performance.

- The unemployment rate in the Euro Area edged up to 6.20 percent in February 2026, rising from 6.10 percent in January. This increase suggests persistent softness in the labour market, with job creation not keeping pace with the number of people seeking work. The rise may reflect challenges faced by certain sectors due to external shocks, ongoing adjustments in the economy, and lingering effects of trade disruptions. Elevated unemployment can weigh on consumer confidence and spending, which in turn may dampen broader economic growth unless addressed by targeted labour market policies and support measures.

China

- China’s annual inflation surged to 1.3% in February 2026, up sharply from just 0.2% in January. This marks the highest inflation rate recorded since January 2023 and notably exceeded market forecasts, which had anticipated a rise of only 0.8%. The significant increase was largely attributable to the Lunar New Year celebrations, which fell in mid-February this year. The holiday period typically sees heightened consumer spending and increased demand for goods and services, temporarily pushing prices upwards. This seasonal effect, combined with ongoing efforts by authorities to stimulate domestic consumption, contributed to the pronounced jump in inflation. Despite the uptick, inflation remains at relatively moderate levels compared to historical averages, reflecting broader trends of price stability within China’s economy.

- The People’s Bank of China (PBoC) opted to keep its key lending rates unchanged at record lows for the tenth consecutive month during its March 2026 meeting, in line with market expectations. This decision signals a commitment to maintaining monetary stability rather than pursuing aggressive stimulus measures. The one-year loan prime rate (LPR), which serves as the benchmark for most corporate and household borrowing, was held steady at 3.0%. Meanwhile, the five-year LPR, commonly used for mortgages, remained unchanged at 3.5%. By keeping rates at these historic lows, the PBoC aims to support economic growth and ensure favourable financing conditions for businesses and consumers, while also monitoring potential risks such as rising debt levels and property market imbalances. This cautious approach reflects a broader strategy to balance growth objectives with financial stability concerns.

- China’s gross domestic product (GDP) expanded by 1.2% quarter-on-quarter in the fourth quarter of 2025, surpassing market expectations of a 1.0% increase and following a 1.1% rise in the third quarter. This latest figure represents the fastest pace of quarterly growth in three quarters, underscoring the resilience of the Chinese economy amid global uncertainties. The robust performance was driven by sustained policy support from Beijing, including targeted fiscal and monetary measures designed to stimulate investment and consumption. Additionally, authorities continued efforts to address structural challenges such as excess industrial capacity and intense price competition in key sectors. These interventions helped foster a more stable environment for businesses and contributed to stronger economic momentum, positioning China favourably as it enters 2026.

- China’s surveyed urban unemployment rate edged up to 5.3% in February 2026, rising from 5.2% in January and exceeding market expectations, which had forecast a rate of 5.1%. This increase suggests some ongoing softness in the labour market, potentially linked to seasonal factors such as the post-Lunar New Year period when temporary jobs may conclude and workforce adjustments take place. The uptick may also reflect broader challenges including slowing job creation in certain sectors, structural shifts within the economy, and uncertainties stemming from global trade and geopolitical tensions. If the trend persists, elevated unemployment could weigh on consumer confidence and spending, highlighting the importance of targeted employment policies and support measures to bolster labour market resilience.

Others

- Japan’s annual inflation eased to 1.3% in February 2026, declining from 1.5% in the previous month and marking the lowest rate since March 2022. This moderation suggests a cooling in price pressures after a period of higher inflation, likely influenced by factors such as subdued consumer demand and stabilising energy costs. Despite persistent challenges—including global supply chain disruptions and fluctuating commodity prices—the Bank of Japan has opted to maintain its key short-term interest rate at 0.75% following its March 2026 policy meeting. Keeping borrowing costs at their highest level since September 1995, the central bank signalled a cautious approach, aiming to balance the need for price stability with support for economic recovery. The decision reflects ongoing uncertainty in global markets and Japan’s continued commitment to gradual monetary policy normalisation.

- The headline inflation rate in Canada fell to 1.8% in February 2026, down from 2.3% in January. This figure was just below market expectations of 1.9%, representing the softest inflation rate since July of the previous year. The decline indicates that price pressures are easing, possibly due to lower energy prices and a stabilising housing market. In response, the Bank of Canada decided to leave its overnight target rate unchanged at 2.25% during its March 2026 meeting, consistent with both market forecasts and the bank’s previous guidance. Policymakers highlighted that the current monetary policy stance remains appropriate given their baseline expectations for economic growth and inflation. The bank continues to monitor economic indicators closely, maintaining flexibility to adjust policy should conditions change, particularly in light of external risks and domestic economic developments.

- The headline inflation rate in Russia eased to 5.9% in February 2025, a slight drop from 6% in the prior month and ahead of market expectations, which had forecast a rate of 5.7%. This gradual reduction reflects ongoing inflationary pressures within the Russian economy, driven by factors such as currency volatility and changes in global commodity prices. The Central Bank of Russia responded by cutting its key policy rate by 50 basis points to 15% at its March 2026 meeting, aligning with median market estimates. This move marks the seventh consecutive rate cut since the policy rate had reached a record high of 21% last year. The central bank’s actions are aimed at supporting economic activity and managing inflation, while also considering risks stemming from geopolitical tensions and domestic fiscal challenges. Policymakers remain vigilant, prepared to adjust policy further to ensure macroeconomic stability and foster sustainable growth.

- Turning to digital assets, Bitcoin, recognised as the world’s largest cryptocurrency, began March trading at approximately $67,000 per token. The month was characterised by intense volatility, with the price experiencing sharp upward and downward movements amid shifting investor sentiment, regulatory developments, and macroeconomic news. By the end of March, Bitcoin closed around $67,500, essentially ending the month flat. This fluctuation underscores the sensitivity of the cryptocurrency market to both global events and market speculation, highlighting the ongoing challenges and opportunities for digital asset investors.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.