Overview

In July 2025, global financial markets were shaped by a complex mix of macroeconomic trends, geopolitical developments, and rising tariff tensions. The reintroduction of targeted tariffs, especially between the U.S., China, and parts of the EU, sparked volatility in trade-sensitive sectors. Geopolitical tensions in the Middle East pushed oil prices sharply higher, adding inflationary pressure globally. Meanwhile, improving economic data from China and easing U.S.–China tech export restrictions provided a lift to technology sectors and Asian markets. Currency markets saw the U.S. dollar strengthen, partly due to safe haven flows and diverging monetary policy signals. Overall, global financial markets in July 2025 exhibited significant movement, shaped by inflation trends, central bank decisions, geopolitical tensions, and evolving economic data across regions. Investors remain alert to shifting monetary policies, the potential for further trade disruptions, and the broader impacts of international conflicts.

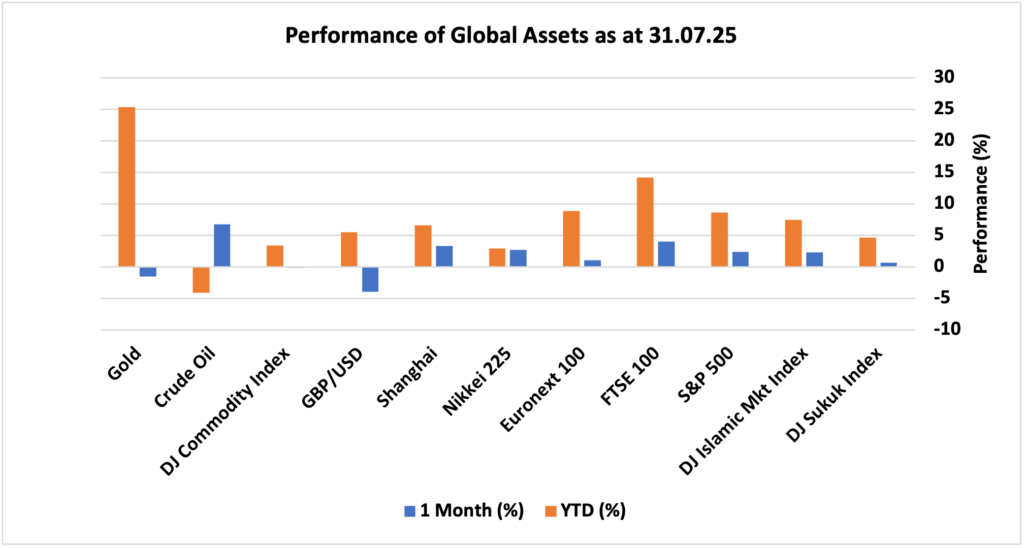

Looking at the performance of major asset classes in July 2025, global financial markets rallied broadly as major U.S. stock indices, including the S&P 500 and Nasdaq, hit fresh all time highs, led by tech and AI related earnings from giants like Microsoft and Meta. The US S&P 500 index gained 2.36% in July. The DJ Islamic markets index also returned 2.33%. Equities surged not only in the U.S. but also in Europe, Asia, and emerging markets, with Asia-Pacific and Eurozone equities outperforming on renewed trade optimism and Chinese economic resilience. A U.S.–EU trade deal and eased U.S.–China tensions lifted investor sentiment, even as new tariff measures weighed on parts of Europe. FTSE 100 and Euronext 100 ended the month with 4.03% and 1.09%, respectively. In Asia, China’s Shanghai index increased 3.34% while Japan’s Nikkei index gained 2.71% in July. Fixed income delivered modest gains amid cooling long term yields, with DJ sukuk index returned 0.65%. And commodities saw a sharp spike in oil (up 6.72% for the month) due to Middle East geopolitical tensions as gold fell 1.5%. Meanwhile, the dollar strengthened, leading to outflows from European equity funds and a renewed preference among investors for U.S.-dollar exposed assets. GBP lost 3.91% against USD. The following snapshot provides a detailed breakdown of the performance of different asset classes in July 2025 and year-to-date.

Market Snapshot

News & Key Events in July

UK

• The United Kingdom experienced a noticeable increase in the annual inflation rate, rising to 3.6% in June 2025. This figure is not only higher than the previous month’s rate of 3.4% but also represents the highest inflation recorded since January 2024. Analysts had generally expected inflation to remain unchanged, so this uptick suggests that price pressures are persisting, possibly driven by factors such as higher energy costs, ongoing supply chain disruptions, or the impact of earlier monetary policy decisions.

• Additionally, the UK’s unemployment rate rose to 4.7% during the three months leading up to May 2025. This increase was unexpected; forecasters had predicted that unemployment would remain steady at April’s 2.6%. The new rate marks the highest level of joblessness seen since the three months ending July 2021, signalling potential challenges in the UK labour market. However, economic growth data presented a more positive note: the British economy expanded by 0.7% in the first quarter of 2025. This result matches the preliminary estimate and is the strongest quarterly growth recorded in a year, reflecting underlying resilience in certain sectors despite the headwinds.

US

• In the United States, the annual inflation rate accelerated for the second month in a row, reaching 2.7% in June 2025. This is the highest level of inflation since February and represents an increase from the 2.4% recorded in May. The reading matched market expectations, indicating that price pressures are in line with forecasts, but the upward trend may keep policymakers cautious.

• The US Federal Reserve (Fed) maintained its benchmark interest rates at 4.25%–4.50% for the fifth consecutive meeting. However, two members of the Federal Open Market Committee dissented, advocating for a rate cut. This marks the first instance of such a dual dissent since 1993, highlighting division within the central bank about the direction of monetary policy.

• The broader US economy showed strong momentum, rebounding with an annualised growth rate of 3% in the second quarter of 2025. This turnaround comes after a 0.5% contraction in the first quarter and surpassed market expectations of a 2.4% increase. The data, drawn from the advance estimate, suggests that the US economy is regaining strength, possibly due to resilient consumer spending or improved export figures.

• In the labour market, the US unemployment rate edged up slightly to 4.2% in July 2025 from 4.1% in June, closely matching market consensus. Meanwhile, payroll growth disappointed: nonfarm payrolls increased by just 73,000 in July, falling short of the 110,000 jobs expected. Furthermore, the previous month’s figure was sharply revised down from an initial 147,000 to just 14,000 jobs, and May’s number was also revised lower by 125,000. These downward revisions suggest labour market momentum may be weakening.

• Consumer confidence, as measured by the University of Michigan’s sentiment index, held steady at 61.7 in July, only marginally different from the preliminary reading of 61.8. This marks the second consecutive monthly increase, bringing sentiment to its highest level since February 2025, which may signal a modest improvement in public outlook.

Europe

• The Eurozone’s annual consumer price inflation was stable at 2.0% year-on-year in July 2025—unchanged from June and slightly above expectations of 1.9%, according to preliminary data. This indicates that inflationary pressures remain present but are not accelerating unexpectedly.

• The European Central Bank (ECB) left interest rates unchanged in July, effectively concluding its recent cycle of monetary easing. Over the past year, the ECB had enacted eight rate cuts, bringing borrowing costs down to their lowest levels since November 2022. The main refinancing rate remains at 2.15%, while the deposit facility rate is at 2.0%. This steady policy stance suggests the ECB believes that current financial conditions are supportive enough for economic activity.

• Economic growth in the Eurozone slowed sharply, with GDP expanding by just 0.1% quarter-on-quarter in the second quarter of 2025, down from 0.6% growth in the previous quarter. Although this pace was slightly better than market expectations of no growth at all, it is the weakest expansion since late 2023 and raises questions about the sustainability of the recovery. The region’s unemployment rate remained unchanged at 6.20% in June.

China

• In China, consumer prices increased by 0.1% year-on-year in June 2025, reversing the 0.1% decline seen in the preceding three months and outperforming expectations for a flat reading. This mild inflation is a sign that consumer demand may be stabilising after a period of weakness.

• The People’s Bank of China (PBOC) kept key lending rates at record lows during its July meeting, which was widely anticipated by markets. The central bank’s decision comes amid growing evidence of slowing economic momentum. China’s growth is being hampered by new US tariffs, subdued domestic demand, and continued problems in the property sector.

• Despite these challenges, China’s GDP grew by 1.1% on a seasonally adjusted basis in the second quarter of 2025, outpacing market expectations of 0.9%. This performance, though slightly slower than the 1.2% growth posted in the first quarter, reflects the impact of government support measures such as interest rate cuts and increased liquidity injections, aimed at offsetting tariff-related headwinds. The country’s surveyed unemployment rate held steady at 5.0% in June, matching both the previous month and market forecasts.

Others

• In Japan, the annual inflation rate declined to 3.3% in June 2025 from 3.5% a month earlier, reaching its lowest level since November 2024. The Bank of Japan opted to keep its short-term policy rate unchanged at 0.5% during its July meeting—the highest it has been since 2008. This decision was unanimous, underscoring the central bank’s cautious approach to gradually normalising policy while monitoring inflation trends.

• Canada’s annual inflation rate rose to 1.9% in June 2025 from 1.7% in May, in line with expectations. While inflation is ticking up, it remains below the Bank of Canada’s mid-point target of 2% for a third consecutive month. The central bank held its benchmark interest rate steady at 2.75% in July, following a total of 2.25 percentage points of rate cuts across seven consecutive meetings. The bank’s guidance suggests that price growth could rise if tariffs and ongoing supply disruptions worsen.

• Russia’s inflation rate continued to moderate, falling for the third month in a row to 9.4% in June 2025—the lowest since November 2024, down from 9.9% in May.

• In the sphere of international relations, former US President Donald Trump, speaking in late July, abruptly reduced the deadline for Russian President Vladimir Putin to agree to a ceasefire in Ukraine from 50 days to “10 or 12 days.” Trump warned that failure to comply by around August 8 would result in harsh new tariffs and sanctions that target Russia and its energy trade partners. Expressing clear frustration with Kremlin actions, Trump called Russia’s military attacks “disgusting” and signalled a willingness to significantly escalate economic pressure if Moscow does not respond swiftly.

• Cryptocurrency markets also saw notable moves. Bitcoin’s price rose over July, ending the month at $116,500 per token—reflecting a broader rally in global risk markets. However, it remains slightly below its early-July peak of $120,000, indicating ongoing volatility and sensitivity to shifts in investor sentiment.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.