Overview

In January 2026, global financial markets were shaped by a renewed reassessment of macroeconomic conditions, trade policy risks, and ongoing geopolitical tensions. Sticky inflation prints in several major economies tempered expectations of near-term interest rate cuts, reinforcing central banks’ cautious “higher for longer” policy stance despite signs of slowing growth, influencing equities while keeping bond yields volatile. At the same time, lingering uncertainty around tariffs and trade restrictions, particularly involving the US, China, and key emerging markets, continued to cloud the outlook for global manufacturing and supply chains. Geopolitical risks, including the Russia-Ukraine war and instability in the Middle East, sustained demand for safe-haven assets such as gold and defensive currencies. Equity markets showed positive performance while fixed income assets made little moves. Overall, investor sentiment in January remained cautiously optimistic but highly sensitive to policy signals and geopolitical headlines.

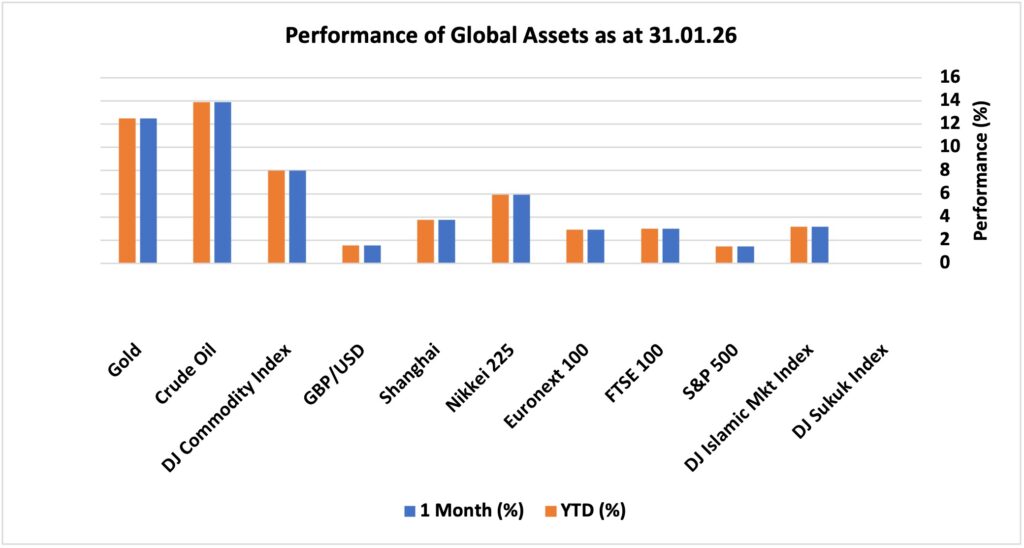

Looking at the performance, major global financial assets showed mixed but generally positive momentum amid macroeconomic recalibration, earnings news, and geopolitical influences. The UK FTSE 100 climbed about 3% for the month as large exporters and commodity-linked stocks benefited from a softer U.S. dollar and positive sentiment around global growth. The EU Euronext 100 surged 2.93% and US S&P 500 also advanced modestly, up 1.45% as strong corporate earnings and the so-called “January effect” supported equities. In Asia, Japan’s Nikkei 225 posted solid gains of around 5.9%, while China’s Shanghai Index was up 3.76% supported by favourable policies. The DJ Islamic Markets Index booked 3.16% whereas DJ Sukuk Index ended the month flat. In commodities, gold surged strongly with 12.5% gains on safe-haven flows and inflation concerns, while the DJ Commodity Index saw 8% returns as energy prices rose on geopolitical risk premiums. Crude oil finished the month near multi-month highs, nearly 14% up, as supply risk fears supported Brent, and GBP/USD strengthened by 1.55% against the U.S. dollar as sterling benefited from relative rate expectations and risk positioning.

The following snapshot provides a detailed breakdown of the performance of different asset classes in January 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in January:

UK

• UK consumer price inflation climbed to 3.4% in December 2025, rising from November’s eight-month low of 3.2% and slightly surpassing market expectations of 3.3%. This uptick at the end of the year marked the first acceleration in inflation since July, raising concerns about the Bank of England’s ability to steer inflation back towards its official 2% target. The increase was largely attributed to seasonal factors and certain volatile components, such as energy and food prices, which experienced short-term spikes. However, government interventions—such as temporary subsidies and energy price caps—are anticipated to help contain further upward pressure, suggesting that this inflation surge may be short-lived rather than a sign of a more persistent trend.

• The UK unemployment rate held steady at 5.1% in the three months to November 2025, unchanged from the previous period and slightly exceeding market expectations of 5.0%. This stability suggests that, despite the challenging economic backdrop and ongoing cost-of-living pressures, the labour market remains relatively resilient. Nevertheless, the unemployment rate remains above pre-pandemic averages, reflecting the impact of higher borrowing costs and weaker demand in some sectors. Policymakers and analysts will be closely monitoring employment data in the coming months for signs of further softening or recovery.

US

• The annual inflation rate in the United States held steady at 2.7% in December 2025, unchanged from November. This stability suggests that price increases for goods and services have levelled off, providing some reassurance for consumers and businesses. The figure also matched market forecasts, indicating that there were no unexpected shifts in inflationary pressures at the end of the year.

• At its January 2026 meeting, the Federal Reserve decided to maintain the federal funds rate at the target range of 3.5% to 3.75%. This decision was widely anticipated by financial markets, particularly following three consecutive rate cuts in the previous year. Those reductions had brought borrowing costs down to their lowest levels since 2022, aiming to support economic growth amid changing conditions. The Fed’s choice to pause signals a cautious approach as policymakers monitor the effects of previous rate cuts.

• The unemployment rate in the US dipped slightly to 4.4% in December 2025, down from a revised 4.5% in November. November’s rate had represented the highest unemployment level seen since October 2021. This modest improvement in December may indicate some recovery in the labour market, although the overall rate remains elevated compared to previous years.

Europe

• Eurozone consumer price inflation eased to 1.9% in December 2025, down from 2.1% in November and slightly under the preliminary estimate of 2.0%. It marked the first time since May that inflation has come in below the European Central Bank’s 2% target, reinforcing expectations that interest rates will remain on hold for an extended period.

• ECB policymakers noted that the central bank could afford to be patient, but stressed that this should not be interpreted as hesitancy to act or an asymmetric approach. According to the accounts from the December 2025 meeting, the ECB currently viewed its monetary policy stance as appropriate, though not static.

• The Gross Domestic Product (GDP) In the Euro Area expanded 0.30 percent in the fourth quarter of 2025 over the previous quarter.

• Unemployment Rate In the Euro Area decreased to 6.20 percent in December from 6.30 percent in November of 2025.

China

• China’s annual inflation rate edged higher to 0.8% in December 2025 from 0.7% in the prior month, marking the highest level since February 2023 but falling short of market forecasts for 0.9%.

• The People’s Bank of China (PBoC) kept key lending rates at record lows for an eighth consecutive month in January, in line with market expectations, after earlier reductions to the central bank’s relending and rediscount facility rates had already taken effect. Last Thursday, the PBoC announced cuts to sector-specific interest rates of 25 bps, effective January 19, to provide an early boost to the economy.

• China’s GDP grew 1.2% quarter-on-quarter in Q4 2025, beating market expectations of 1.0% and following a 1.1% increase in Q3 and logging the fastest expansion in three quarters. The latest reading reflected sustained policy support from Beijing alongside efforts to curb excess industrial capacity and rein in aggressive price competition.

• China’s surveyed urban unemployment rate stood at 5.1% in December 2025, unchanged from the previous two months and slightly below market expectations of 5.2%.

Others

• Japan’s annual inflation eased to 2.1% in December 2025 from 2.9% in the prior month, the lowest since March 2022. The Bank of Japan kept its key short-term interest rate unchanged at 0.75% at its first policy meeting of 2026, maintaining borrowing costs at their highest level since September 1995, ahead of February’s snap election.

• The headline inflation rate in Canada rose to 2.4% in December of 2025 from 2.2% in the previous month, the highest in three months, and firmly above market expectations that the rate would remain unchanged. The result contrasted slightly with the Bank of Canada’s expectations that CPI inflation would remain around the 2% threshold in the near-term. The Bank of Canada held its overnight target rate unchanged at 2.25% in its January 2026 meeting, aligned with market expectations and its earlier guidance, and noted that the current policy remains appropriate given the Bank’s baseline economic outlook.

• Inflation Rate in Russia decreased to 5.60 percent in December from 6.60 percent in November of 2025.

• Turning to digital assets, Bitcoin, recognised as the world’s largest cryptocurrency, began the month trading at approximately $89,000 per token. Throughout January, the cryptocurrency experienced high fluctuations, ultimately closing out the month just above $76,000.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.