Overview

In February 2026, global financial markets were shaped by a delicate balance between moderating inflation trends, persistent trade frictions, and heightened geopolitical uncertainty. Mixed macroeconomic data from the US, Europe, and China fuelled debate over the timing and pace of interest rate cuts, keeping bond yields and equity markets volatile. Ongoing tariff discussions and selective trade restrictions among major economies added pressure to export-oriented sectors and global supply chains. Geopolitical tensions, including developments in Eastern Europe and the Middle East, supported safe-haven flows into gold and defensive currencies. Equity performance was uneven, with AI-driven technology stocks outperforming while cyclicals lagged amid growth concerns. Overall, investor sentiment remained cautious, highly sensitive to policy signals and global risk developments.

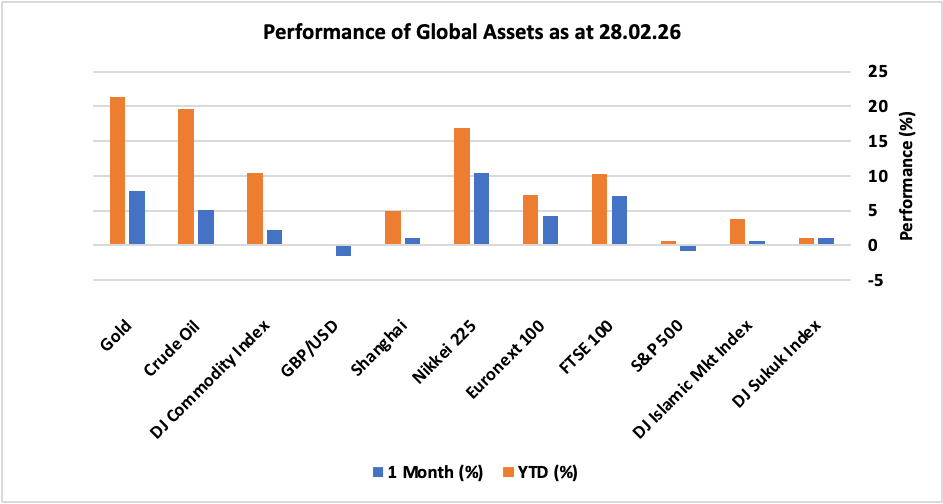

Looking at the performance, major global financial assets showed mixed but generally positive momentum amid macroeconomic recalibration, earnings news, and geopolitical influences. In Asia, Japan’s Nikkei 225 led the gains with positive returns of 10.4%, while in Europe, UK FTSE 100 and EU Euronext 100 surged 7.04% and 4.15%, respectively, driven by rotation strategies. China’s Shanghai Index was up 1.09% supported by favourable policies. US S&P 500 declined by 0.76% amid sell-US sentiment while DJ Islamic Markets Index booked positive 0.6% returns during the month. DJ Sukuk Index ended the month up 1% amid softening yields. In commodities, gold surged strongly with 7.9% gains on safe-haven flows, while Crude oil saw 5% upside as energy prices rose on geopolitical risk premiums. Lastly, GBP depreciated by 1.5% against the U.S. dollar as relatively sticky US inflation and resilient labour market data reinforced the Federal Reserve’s “higher for longer” stance, boosting the US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in February 2026, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in February:

UK

• UK consumer price inflation eased to 3.0% in January 2026, falling from 3.4% in December and aligning with analysts’ forecasts. This represents the lowest annual inflation rate since March 2025. The moderation was largely attributed to slower increases in transport and food prices, reflecting the impact of lower fuel costs and subdued grocery inflation. The easing in inflation provided some relief for households and raised hopes that the Bank of England might consider rate cuts in the coming months if the trend persists.

• The Bank of England decided to keep its Bank Rate unchanged at 3.75% during its February meeting, with a narrow 5 to 4 split among policymakers. This decision came as the Monetary Policy Committee weighed the benefits of easing inflation pressures against the risks posed by a slowing economy. Notably, four committee members voted for a 25 basis point cut, signalling increasing divergence within the group and reflecting concerns over economic growth and the need to support activity. The close vote highlighted the growing debate over the appropriate timing for monetary easing.

• The UK economy expanded by 0.1% in the fourth quarter of 2025, maintaining the same growth rate as in the previous three-month period. This performance was marginally below market expectations, which had anticipated a 0.2% increase. The preliminary estimates suggest that the economy remains sluggish, with modest gains driven by resilient consumer spending and stabilising business investment, despite ongoing challenges such as higher borrowing costs and global uncertainty. The data indicate that the UK continues to face headwinds, including weak productivity growth and cautious sentiment among businesses.

• The UK unemployment rate increased to 5.2% in the three months ending December 2025, slightly surpassing market expectations, which had forecast stability at 5.1% from the previous period. This rise hints at softening labour market conditions, possibly reflecting business caution amid economic uncertainty and subdued growth. The uptick in unemployment may suggest that employers are scaling back hiring or making adjustments in response to slower economic activity and persistent challenges in key industries such as retail and manufacturing.

US

• The annual inflation rate in the United States eased to 2.4% in January 2026, marking its lowest point since May of the previous year. This moderation in inflation follows two consecutive months where the rate stood at 2.7%, and it is also slightly better than market forecasts, which had anticipated a 2.5% rate. The decline suggests that price pressures are gradually subsiding, possibly as a result of tighter monetary policies and cooling consumer demand. Lower inflation may provide some relief for households and businesses, potentially influencing the Federal Reserve’s future decisions regarding interest rates. This trend could signal a stabilisation in the cost of living after a period of elevated inflation across the US economy.

• The US economy grew at an annualised rate of 1.4% in the fourth quarter of 2025, which represents the slowest pace of expansion since the first quarter of the year. This slowdown comes after a robust 4.4% growth rate recorded in the third quarter, and it is notably below the market’s advance estimate of 3%. The weaker growth figure may reflect softer consumer spending, reduced business investment, or the lagged effects of higher interest rates. Such a deceleration could prompt policymakers and investors to reassess the outlook for economic momentum in 2026, as the economy appears to be losing some of its previous vigour.

• The US unemployment rate edged down to 4.3% in January 2026, a slight improvement from 4.4% in December and marginally better than analysts’ expectations of 4.4%. This modest decline in unemployment suggests a relatively resilient labour market, even as economic growth has moderated. The improvement may be attributed to ongoing job creation in certain sectors or a stabilisation in workforce participation. Nevertheless, the overall level remains higher compared to earlier in the recovery, indicating that challenges persist for some workers and that the broader employment picture is still somewhat mixed.

Europe

• Annual inflation in the Euro Area climbed to 1.9% in February 2026, marking a notable increase from January’s 16-month low of 1.7%. This uptick exceeded market forecasts, which had anticipated inflation to remain steady at 1.7%. The rise suggests renewed price pressures, possibly driven by factors such as higher energy costs or supply chain disruptions. Economists will be watching closely to see if this marks the start of a sustained upward trend or merely a short-term fluctuation.

• At its first policy meeting of 2026, the European Central Bank (ECB) opted to keep interest rates unchanged, maintaining a cautious stance in light of ongoing inflation dynamics. The ECB reiterated its expectation that inflation will settle at its 2% target over the medium term, signalling confidence in its current monetary policy approach. The main refinancing rate was held at 2.15%, while both the deposit facility and marginal lending rates remained at 2.0% and 2.4%, respectively. This stable rate environment is intended to foster economic resilience while keeping inflation under control.

• The euro area economy grew by 0.3% in the fourth quarter of 2025, confirming earlier estimates and matching performance in the previous quarter. This steady expansion demonstrates the bloc’s ability to withstand external challenges, such as easing inflation and lower borrowing costs. However, growth came despite persistent headwinds, including US trade tariffs imposed on EU imports, which have the potential to dampen export activity and overall economic momentum. Nevertheless, the data highlight the euro area’s resilience and adaptability in a shifting global landscape.

• The Euro Area’s seasonally adjusted unemployment rate fell to a historic low of 6.1% in January 2026, down from 6.2% in December and surpassing analysts’ expectations. This improvement reflects robust labour market conditions and suggests that businesses are continuing to hire despite broader economic uncertainties. The sustained low unemployment rate is a positive signal for household incomes and consumer spending, underpinning further economic stability in the region.

China

• China’s annual inflation rate slowed markedly to 0.2% in January 2026, a significant drop from the 0.8% recorded in December. This figure not only represents the lowest inflation print since October but also came in below market forecasts, which had anticipated a rise of 0.4%. The sharp easing highlights subdued consumer demand and ongoing deflationary pressures within the Chinese economy, raising concerns about the sustainability of domestic recovery.

• In monetary policy, the People’s Bank of China (PBoC) opted to keep its key benchmark lending rates unchanged for a ninth straight month in February. This decision was widely expected by market participants and indicates that policymakers are adopting a cautious approach, refraining from broad-based monetary stimulus despite the recent introduction of targeted support measures. The PBoC’s stance suggests confidence in the effectiveness of these targeted interventions and a desire to avoid fuelling financial risks through excessive easing.

• On the economic growth front, China’s gross domestic product (GDP) expanded by 1.2% quarter-on-quarter in the fourth quarter of 2025. This pace exceeded market expectations of a 1.0% increase and followed a 1.1% gain in the previous quarter, marking the most robust quarterly growth rate in the past three quarters. The acceleration in GDP growth signals a strengthening in economic activity towards the end of the year, supported by resilient exports, government investment, and a gradual improvement in consumer spending.

• Meanwhile, China’s surveyed urban unemployment rate remained steady at 5.1% in December 2025, unchanged for three consecutive months and marginally better than market expectations of 5.2%. This stability in the labour market suggests that employment conditions are holding up despite moderate economic challenges, providing some reassurance about the resilience of the broader economy.

Others

• Japan’s annual inflation eased to 1.5% in January 2026, down from 2.1% in the prior month, marking the lowest rate since March 2022. This decline reflects subdued price pressures across key sectors, possibly influenced by weaker consumer demand and falling international commodity prices. Despite the moderation in inflation, the Bank of Japan chose to keep its key short-term interest rate steady at 0.75% during its first policy meeting of 2026. This decision maintains borrowing costs at their highest level since September 1995, signalling a cautious approach as policymakers await further clarity, particularly with the upcoming snap election in February. The central bank’s stance suggests a commitment to stability amid ongoing economic uncertainties and political developments.

• Canada saw its headline inflation rate ease to 2.3% in January 2026, down from a three-month high of 2.4% in the previous period. This marginal decrease was just below market expectations, which had anticipated inflation to remain at 2.4%. The slight cooling in consumer prices may be attributed to stabilising energy costs and moderating price increases in food and housing. Although inflation remains above the Bank of Canada’s target, the recent figures suggest that upward price momentum is waning, providing policymakers with breathing room to assess future rate decisions and the broader economic outlook.

• In Russia, the annual inflation rate ticked up to 6% in January 2026, rising from an over two-year low of 5.6% in the prior month. This uptick highlights emerging price pressures, potentially driven by currency movements, increased government spending, or supply chain challenges. In response, the Bank of Russia cut its benchmark interest rate by 50 basis points to 15.5% at its first meeting of the year, diverging from the median market expectation which had projected rates to remain unchanged. The central bank’s move aims to support economic growth and counteract slowing activity, reflecting concerns about the trajectory of the Russian economy amid persistent inflation and external headwinds.

• Turning to digital assets, Bitcoin, recognised as the world’s largest cryptocurrency, began February trading at approximately $76,000 per token. The month was characterised by intense volatility, with the price experiencing sharp upward and downward movements amid shifting investor sentiment, regulatory developments, and macroeconomic news. By the end of February, Bitcoin closed around $67,000, reflecting a significant drop. This fluctuation underscores the sensitivity of the cryptocurrency market to both global events and market speculation, highlighting the ongoing challenges and opportunities for digital asset investors.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.