Overview

In December 2025, global financial markets were shaped by a complex interplay of macroeconomic signals, trade policies, and geopolitical risks. Sticky inflation in major economies and the growing conviction that interest rates would remain “higher for longer” influenced equity valuations and kept bond yields volatile. Renewed tariff rhetoric and selective trade restrictions between major economies added uncertainty to global supply chains, weighing on export-oriented sectors. Geopolitical tensions, particularly around the Russia-Ukraine conflict and persistent instability in the Middle East, continued to support safe-haven assets such as gold while pressuring energy and shipping markets. Overall, investor sentiment in December was cautious, balancing hopes of a 2026 slowdown in tightening with lingering structural and geopolitical risks.

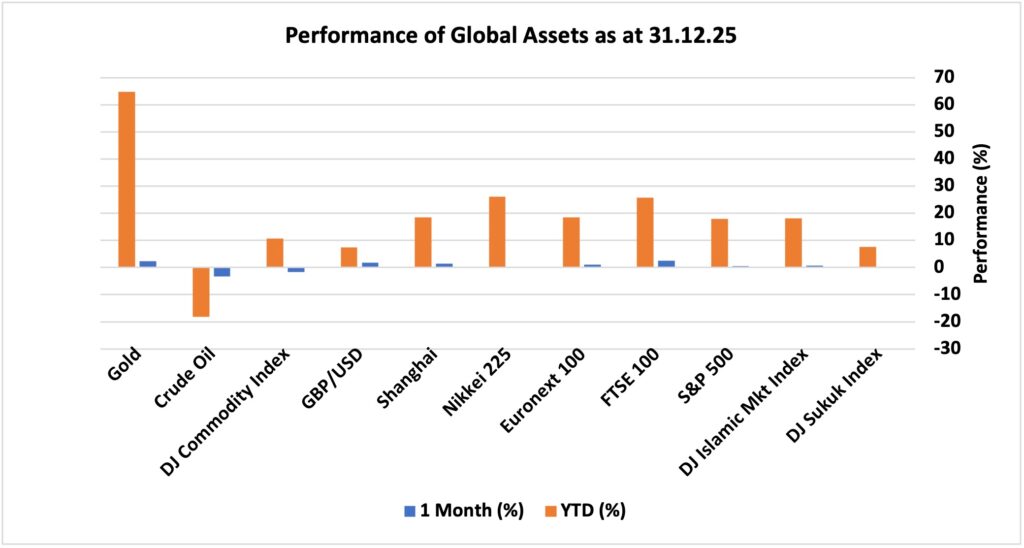

Looking at the performance of major asset classes, key indices exhibited varied performances as markets digested macroeconomic, geopolitical, and sector-specific drivers. UK FTSE 100 finished December positive, contributing 2.45% to a 25.8% yearly gain in 2025, outperforming many peers on strong mining and defence gains and rate-cut optimism. China’s Shanghai Composite was up 1.4% in December with broader 2025 returns up to 18.4% on renewed growth signals. The U.S. equity market benchmark S&P 500 rose 0.6% supported by AI tech enthusiasm while European equity market Euronext 100 ended the month 1% up. The benchmark for shariah-compliant investments, DJ Islamic market index, surged 0.73% as overall performance mirrored broader market uptrends while Japan Nikkei 225 index gained by 0.30% in the month. In response to easing narrative around monetary policies, yields moved lower that helped DJ Sukuk Index end the month with 0.2% upside. Gold continued to shine as a strong bet for safe haven with 2.31% surge, adding to yearly gain of 65%. Lastly, UK pound gained 1.81% against US dollar.

The following snapshot provides a detailed breakdown of the performance of different asset classes in December 2025, as well as their progress year-to-date, offering a comprehensive overview of market dynamics during a period marked by both optimism and lingering uncertainty.

Market Snapshot

News & Key Events in December:

UK

• The annual inflation rate in the UK eased to 3.2% in November 2025, marking the lowest level recorded in eight months. This slowdown is a notable improvement from the 3.6% reported in October and also comes in below both market forecasts of 3.5% and the Bank of England’s own projection of 3.4%. The decline in inflation is primarily attributed to moderating energy prices and a stabilisation in food costs, providing some relief to households facing persistent cost-of-living pressures. However, inflation remains above the central bank’s 2% target, underscoring ongoing challenges for policymakers.

• Responding to the easing inflation and accumulating signs of economic weakness, the Bank of England decided to lower the Bank Rate by 25 basis points to 3.75%. This is the lowest level since 2022 and represents the first rate cut since August, signalling a shift in monetary policy towards supporting growth. Policymakers cited subdued consumer spending, softer business investment, and weaker labour market data as key factors prompting the decision, aiming to help stimulate economic activity and bolster confidence during a period of stagnation.

• The UK economy saw minimal expansion in the third quarter of 2025, with GDP rising by just 0.1%. This figure confirms preliminary estimates and highlights a slowdown compared to the 0.3% growth recorded in the previous quarter. The sluggish pace reflects ongoing headwinds such as subdued consumer and business confidence, higher borrowing costs, and lingering uncertainties around fiscal and trade policies, all of which have constrained economic momentum.

• The UK unemployment rate edged up to 5.1% in the three months to October 2025, aligning with market expectations and marking a slight increase from the previous period’s 5.0%. This uptick in joblessness is indicative of cooling labour market conditions, with some sectors experiencing hiring slowdowns and redundancies amid economic uncertainty. While the rise is relatively modest, it reinforces the picture of a fragile recovery, with job security and wage growth remaining key concerns for households and policymakers alike.

US

• In December 2025, the annual inflation rate in the United States fell to 2.7%, marking the lowest level observed since July of the same year. This outcome was notably below both market expectations, which had anticipated a rate of 3.1%, and the 3% rate recorded in September. The decline in inflation suggests that price pressures in the US economy are easing, which may provide some relief to consumers and businesses after a period of elevated inflation.

• At its December meeting, the Federal Reserve decided to lower the federal funds rate by 25 basis points, setting it within a target range of 3.5% to 3.75%. This move was in line with market consensus and represented the third rate cut implemented by the Fed during 2025. According to the minutes from this meeting, most members of the Federal Open Market Committee (FOMC) expressed the view that further rate reductions could be warranted in the coming year, provided that inflation continues to moderate over time. This indicates a cautious but responsive approach to monetary policy, balancing the need to support economic growth while keeping inflation in check.

• Economic growth in the United States showed notable strength in the third quarter of 2025, with gross domestic product (GDP) expanding at an annualised rate of 4.3%. This was the fastest pace in two years and exceeded both the 3.8% recorded in the previous quarter and the forecast of 3.3%. The revised estimate highlights the resilience of the US economy, with the growth primarily driven by robust consumer spending, a rise in exports, and increased government expenditure. These factors combined to bolster economic activity despite global uncertainties.

• Despite the positive economic indicators, the US labour market showed signs of softening, as the unemployment rate rose to 4.6% in November 2025. This increase from 4.4% in September surpassed market expectations, which had anticipated the rate would remain steady at 4.4%. The November figure represents the highest unemployment rate since September 2021, suggesting some cooling in the jobs market and highlighting ongoing challenges for American workers even as the broader economy continues to grow.

Europe

• The annual inflation rate in the Eurozone was revised down slightly to 2.1% in November 2025, from an earlier preliminary figure of 2.2%. This adjustment brings the November figure in line with the reading for October, suggesting price pressures remained stable over the two-month period. The revision reflects updated data on consumer prices across member countries and signals that inflation is gradually approaching the European Central Bank’s target levels.

• At its December 2025 meeting, the European Central Bank (ECB) opted to maintain borrowing costs for the fourth consecutive time. The main refinancing rate stayed at 2.15%, while the deposit facility rate was kept at 2.0%. This decision was widely anticipated by financial markets, as policymakers continue to emphasise a cautious approach by relying on the latest economic data and evaluating conditions at each meeting. The ECB reiterated its commitment to a data-driven strategy, indicating that any future adjustments to interest rates will be determined by ongoing economic developments and inflation trends.

• Economic growth in the Eurozone showed modest improvement in the third quarter of 2025, with GDP growth being revised upwards to 0.3% from the initial estimate of 0.2%. This increase marks an acceleration compared to the 0.1% expansion recorded in the previous quarter, hinting at a gradual recovery in economic activity. The revision is based on more complete data and points to slightly better-than-expected performance in sectors such as manufacturing and services.

• The unemployment rate in the Euro Area held steady at 6.40 percent in October, indicating that the labour market has remained resilient despite ongoing economic challenges. The stable rate suggests that job creation has kept pace with the expansion of the workforce, and there has been no significant deterioration in employment conditions during this period.

China

• China’s annual inflation rate increased to 0.7% in November 2025, rising from 0.2% recorded in the previous month. This acceleration in consumer prices was in line with market consensus and represents the highest inflation rate observed since February 2024. The uptick was largely driven by a rebound in food and energy prices, as well as a gradual recovery in consumer demand. The latest figures suggest that deflationary pressures seen earlier in the year are beginning to ease, providing a more positive outlook for China’s domestic economy.

• The People’s Bank of China (PBoC) opted to keep its key lending rates at record lows for the seventh month in a row during December. This decision was widely anticipated by analysts and investors. The central bank also maintained the seven-day reverse repo rate at 1.4% this month, which now serves as its primary policy instrument. These actions reflect the central bank’s view that there is less immediate need for further monetary easing, as the economy appears on track to achieve this year’s official growth target. The PBoC’s cautious approach signals confidence in the current policy stance but leaves room for additional support should the economic outlook deteriorate.

• China’s gross domestic product (GDP) expanded by 1.1% quarter-on-quarter in the third quarter of 2025, outperforming market forecasts of a 0.8% increase. This followed a modestly revised 1.0% gain in the second quarter. The stronger-than-expected growth was underpinned by a series of supportive measures from Beijing, including liquidity injections to boost credit availability and targeted interventions aimed at stabilising financial markets. These efforts helped to mitigate the impact of weak domestic demand and curb deflationary risks, reinforcing the government’s commitment to supporting economic stability.

• China’s surveyed urban unemployment rate remained steady at 5.1% in November 2025, unchanged from the previous month and consistent with market expectations. This rate matches the lowest level recorded since June, reflecting a relatively stable labour market despite ongoing challenges in some sectors. The steady unemployment figure suggests that recent government policies and economic support measures have been effective in preserving jobs and maintaining social stability during a period of economic uncertainty.

Others

• Japan’s annual inflation rate edged down to 2.9% in November 2025 from October’s 3-month high of 3.0%, as food inflation hit its lowest in a year (6.1% vs 6.4% in October) amid the slowest rise in 15 months for rice prices. The BoJ raised its policy rate by 25 basis points to 0.75% at its December meeting, marking the highest level since 1995. Officials at the Bank of Japan broadly agreed that further interest-rate increases and a gradual reduction in monetary accommodation are appropriate to achieve sustainable price stability, according to the Summary of Opinions from the BoJ’s December meeting.

• The headline inflation rate in Canada held at 2.2% in November of 2025, unchanged from October, below expectations of 2.3%, and still loosely converging toward the 2% threshold in the near term as projected in the Bank of Canada’s baseline scenario. The Bank of Canada held its target overnight rate at 2.25% in December 2025, keeping the Bank Rate at 2.50% and the deposit rate at 2.20% after signalling in October that the policy rate was about right.

• The annual inflation rate in Russia fell to 6.6% in November 2025 from 7.7% in the previous month, the lowest since September 2023 and below market expectations of 6.7%. The Bank of Russia cut its benchmark interest rate by 50bps to 16% on December 19, 2025, in line with market expectations, reflecting progress in disinflation amid a gradual return of the economy to a more balanced growth path.

• Turning to digital assets, Bitcoin, recognised as the world’s largest cryptocurrency, began the month trading at approximately $87,000 per token. Throughout December, the cryptocurrency experienced modest fluctuations but maintained an overall upward trend, ultimately closing out the month just above $89,000. This steady growth suggests a sense of cautious optimism among investors, possibly reflecting broader confidence in the digital asset market and anticipation of future developments in cryptocurrency adoption and regulation.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.