Overview

In August 2025, global financial markets were shaped by a dynamic mix of macroeconomic trends, tariff policies, and geopolitics. Slightly cooling U.S. inflation revived expectations of a September Fed rate cut, lifting Wall Street and supporting risk assets, while the Bank of England’s rate cut underscored lingering weakness in the UK economy. Meanwhile, trade tensions persisted as the Trump administration’s tariff deadlines approached, prompting volatility in currency and commodity markets. Geopolitical risks, particularly the Russia-Ukraine potentially fragile ceasefire talks and ongoing Gaza conflict, fuelled safe-haven demand for gold and sovereign bonds. Oil prices softened despite OPEC+ output adjustments, while equities across the U.S., Europe, and Asia delivered solid positive performance. Overall, markets balanced optimism around inflation and monetary policy with caution over trade frictions and geopolitical flashpoints.

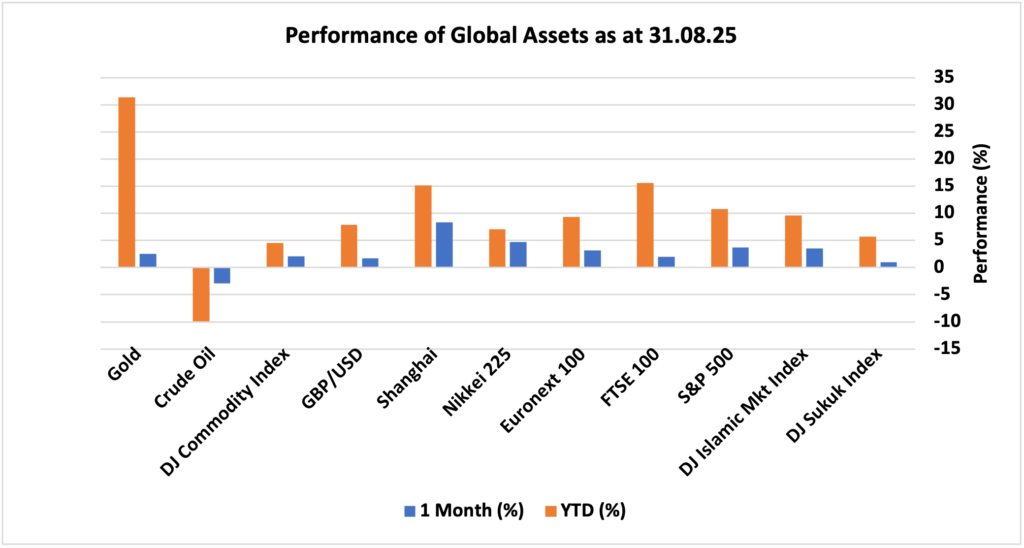

Looking at the performance of major asset classes in August 2025, global financial markets rallied broadly as major stock indices ended the month on the strong footings. UK FTSE 100 reached a record closing high at approximately 9,321 on 22 August, before reiterating slightly lower, up just under 2% in August, reflecting renewed optimism as well as concerns over UK interest rate cuts and energy-driven inflation approaching 4%. Europe’s Euronext 100 finished August up approximately 3.1%, despite the mixed picture in continental Europe amid uneven growth signals. US S&P 500 gained 3.7% over the month, supported by strong earnings, resilient GDP growth, and mounting anticipation of a Fed rate cut in September. The DJ Islamic markets index also returned 3.5%. China’s Shanghai Composite ended the month with strong upside momentum, gaining around 8.4%, driven by active retail participation and strong daily turnover despite easing enthusiasm. Meanwhile, Japan’s Nikkei 225 rose approximately 4.7%, as inflation continued falling. Gold rose 2.5% amid USD losing 1.7% against GBP. On the fixed income front, DJ sukuk index returned 1% as yields softened with the hope of interest rate cut in September. The following snapshot provides a detailed breakdown of the performance of different asset classes in August 2025 and year-to-date.

Market Snapshot

News & Key Events in August

UK

• The annual inflation rate in the UK jumped to 3.8% in July 2025, the highest since January 2024, up from 3.6% in June and above market expectations of 3.7%. The main upward pressure came from transport, where prices climbed 3.2% (vs. 1.7% in June), driven by a 30.2% surge in airfares, likely reflecting the timing of school summer holidays.

• The Bank of England cut interest rates by 25 bps to 4%, the lowest since March 2023, in a rare two-round vote that underscored sharp divisions over how to tackle sticky inflation and a softening economy. Five of the nine MPC members backed a 25bps cut, while four voted for no change. Governor Andrew Bailey called it a “finely balanced” decision and reiterated that future cuts will be “gradual and careful.”

• The British economy grew 0.3% qoq in Q2 2025, slowing from a 0.7% expansion in Q1 but surpassing forecasts of just 0.1%, according to preliminary estimates. The moderation partly reflects activity being brought forward to February and March ahead of April’s stamp duty changes and the announcement of new US tariffs.

• The United Kingdom’s unemployment rate stood at 4.7% in the three months to June 2025, unchanged from the previous period as the market expected.

US

• The US annual inflation rate remained at 2.7% in in July 2025, the same as in June and below forecasts of 2.8%. Price pressures increased for used cars and trucks (4.8% vs 2.8% in June), transportation services (3.5% vs 3.4%) and new vehicles (0.4% vs 0.2%) while inflation steadied for food (2.9% vs 2.9%).

• The US economy grew at an annual rate of 3.3% in Q2 2025, a sharp rebound from the 0.5% contraction in Q1, according to second estimates.

• The US unemployment rate rose slightly to 4.2% in July 2025 from 4.1% in June, aligning with market expectations. The number of unemployed increased by 221,000 to 7.236 million, while employment fell by 260,000 to 163.106 million.

• The University of Michigan consumer sentiment for the US dropped to 58.2 in August of 2025 from the five-month high of 61.7 in the previous month, revised down from the preliminary estimate of 58.6 and well under the initial market expectations of 62. It was the first drop in the sentiment gauge in four months, mainly due to growing inflation concerns and sharply worse buying conditions for durable goods, which fell to their lowest in one year.

Europe

• Euro area consumer price inflation edged up to 2.1% in August 2025, a modest acceleration from July and slightly above market expectations of 2.0%. This uptick was driven by persistent pressure in energy and food costs, as well as notable increases in services. The continued rise in prices prompted renewed debate within the European Central Bank regarding the timeline for any potential adjustment in monetary policy, with policymakers weighing the risks of premature easing against the threat of inflation overshooting targets.

• Meanwhile, the Euro Area’s seasonally adjusted unemployment rate declined to 6.2% in July 2025, improving from June’s 6.3%. The drop suggests a steadying labour market, as job creation remained resilient despite broader economic headwinds. Sectors such as manufacturing, logistics, and hospitality all contributed to the better-than-expected employment figures, with Germany and Spain leading the gains. Analysts noted that while the employment landscape remains robust, wage growth is only beginning to catch up with inflation, leaving real incomes stretched for many households.

• In terms of business activity, the HCOB Eurozone Manufacturing PMI climbed to 50.7 in August 2025, surpassing both the flash estimate of 50.5 and July’s reading of 49.8. This represents the first monthly improvement in factory conditions since June 2022, suggesting that the region’s industrial sector may be turning a corner after a prolonged period of stagnation. Rising orders and increased output underpinned the headline figure, reflecting a gradual recovery in demand across key markets. However, input costs remain elevated, and many manufacturers continue to grapple with supply chain disruptions and uncertainty around future energy prices. Industry leaders remain cautiously optimistic, pointing to ongoing investment in automation and green technologies as potential sources of resilience in the coming quarters.

China

• China’s consumer prices were flat from a year earlier in July 2025, surpassing market expectations for a 0.1% drop and following a 0.1% gain in the previous month.

• The People’s Bank of China (PBOC) maintained key lending rates at record lows for the third consecutive month during the August fixing, in line with market expectations. The decision came despite recent economic data suggesting that the economy might be losing momentum. The one-year Loan Prime Rate (LPR)—the benchmark for most corporate and household loans—was kept steady at 3.0%, while the five-year LPR, which guides mortgage rates, remained unchanged at 3.5%.

• China’s surveyed unemployment rate rose to 5.2% in July 2025, up from 5% in June and above market expectations of 5.1%. This marked the highest reading since March.

Others

• Japan’s annual inflation rate eased to 3.1% in July 2025 from 3.3% in the previous month, marking the lowest reading since November 2024.

• The annual inflation rate in Canada eased to 1.7% in July 2025, from 1.9% in June and below market forecasts of 1.8%, staying beneath the BoC’s 2% mid-point for a fourth consecutive month.

• The annual inflation rate in Russia eased for a fourth straight month to 8.8% in July of 2025, the softest since October of last year, from 9.4% in June. The development was in line with the Bank of Russia’s forecast that inflationary pressures were unlikely to remain at the elevated level from the first half of the year, but price growth still held well above the central bank’s 4% target.

• In the sphere of international relations, in August 2025, Russian President Vladimir Putin made his first formal visit to U.S. soil since 2015, attending a high-profile summit with President Donald Trump at Joint Base Elmendorf-Richardson in Anchorage, Alaska, marking the first-ever U.S.-hosted Russia summit on American military property. The red-carpet welcome and warm optics were seen as lifting Russia’s diplomatic isolation, even as Western leaders expressed alarm at his renewed visibility on the global stage. The summit, focused on the Russo-Ukrainian War, concluded without any formal ceasefire but underscored Putin’s ability to reclaim international relevance amid ongoing sanctions. Though no agreement was secured, discussions reportedly touched on territorial “swaps” and mutual understandings, with Putin framing the meeting as a strategic success.

• Cryptocurrency markets also saw notable moves. Bitcoin’s price remained volatile, ending the month at $109,000 per token, booking the gains of sharp price rise in July-August. However, it remains well below its mid-August peak of $122,800, indicating ongoing volatility and sensitivity to shifts in investor sentiment.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.