Silver is both a monetary metal and a high‑value industrial material, so its price and role in portfolios sit between gold and base metals. This article covers its significance, uses, relationship with gold, price drivers, recent performance, and outlook.

What silver is and why it matters

Silver is a precious and noble metal, meaning it is relatively rare, valuable, and resistant to corrosion and oxidation. It also has the highest electrical and thermal conductivity of all metals, and strong reflectivity and antibacterial properties. These physical traits make silver important in:

- Money and investment (coins, bars, ETFs).

- Jewellery and silverware.

- Electronics, energy, and medical applications.

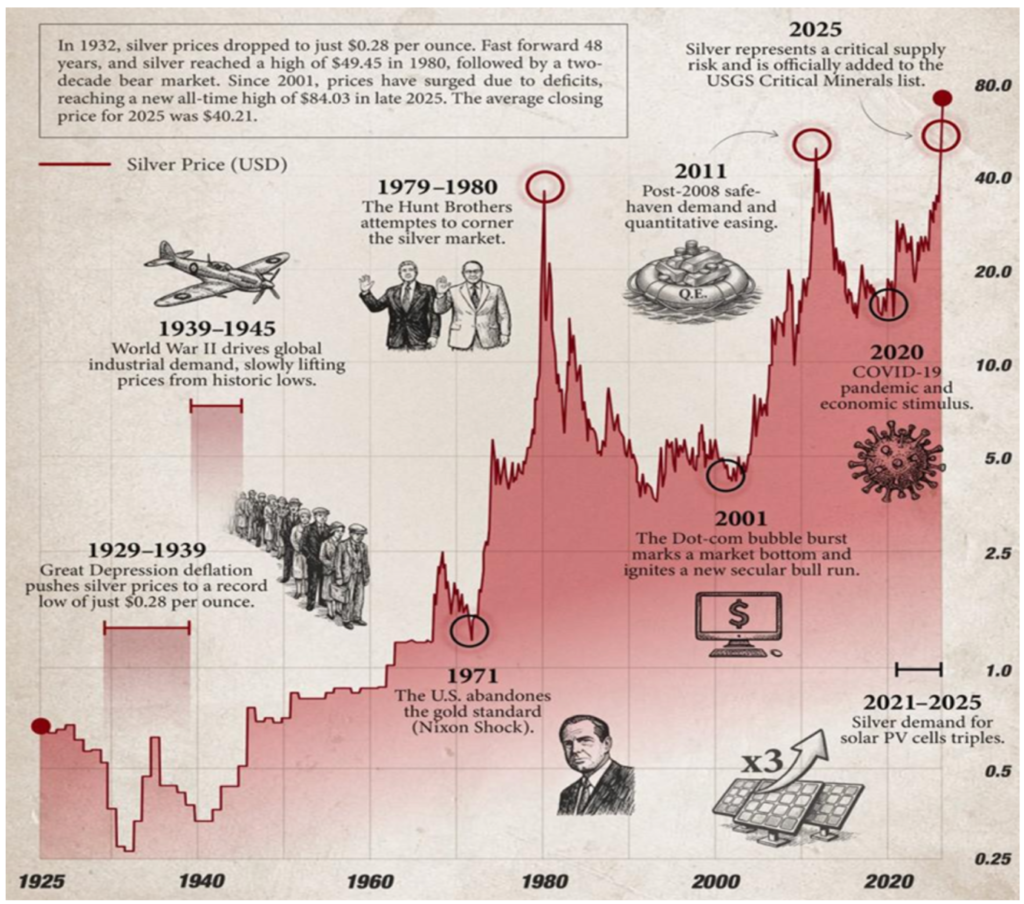

Because it is both an industrial input and a store of value, silver tends to be more cyclical and volatile than gold. The following graph explains 100 years history of silver driven by major events and policy shifts.

Source: Kotakmf.com

Main uses and real‑economy significance

Silver’s demand today is broadly split between industrial uses, jewelry/silverware, and investment holdings. Key uses include:

- Electronics and electrical: Conductive pastes, connectors, contacts, and solders in consumer electronics, vehicles, and industrial equipment.

- Solar and renewables: Silver paste in photovoltaic (PV) cells is critical for efficiently conducting electricity in solar panels, making green‑energy growth a major demand driver.

- Batteries and EVs: Use in high‑performance batteries and electrical systems supports demand from electric vehicles and energy storage.

- Medicine and hygiene: Antimicrobial silver ions are used in wound dressings, medical device coatings, catheters, breathing tubes, and some consumer antibacterial products.

- Water and food safety: Silver is used in water purification systems and in some food‑contact applications due to its ability to inhibit microbial growth.

- Jewellery and silverware: Provides aesthetic demand that is sensitive to income levels and fashion trends.

Historically, silver was also heavily used in film photography; that demand has declined, which removed a substantial structural pillar of consumption.

Correlation with gold and the silver–gold ratio

Gold and silver often move in the same direction because both respond to macro forces like interest rates, inflation expectations, the US dollar, and risk sentiment. Over rolling one‑year periods, their correlation has frequently been high (roughly 0.7–0.95), though in recent years it has weakened at times as gold traded more like a monetary asset and silver more like an industrial metal.

Silver–to–gold ratio

The silver–to–gold ratio (often expressed as gold–silver ratio) is the price of gold divided by the price of silver. Historically, this ratio has averaged around 60:1 and the ratio was over 90 in 2025, however, as of late January 2026, the gold-silver ratio is approximately 46:1 to 47:1. It has dropped due to silver’s parabolic rise. This means it takes roughly 46-47 ounces of silver to purchase one ounce of gold. This ratio represents a significant decrease (closer to silver being more expensive relative to gold) from recent highs, driven by a recent strong rally in silver prices.

In precious‑metal bull markets, this ratio tends to contract because silver usually outperforms gold, reflecting its higher beta and cyclical industrial demand. Investors sometimes treat very high ratios as a signal that silver could have catch‑up potential if macro conditions favour metals broadly.

Gold Silver Ratio:

Source: goldsilver.com

Key drivers of silver’s price in recent years

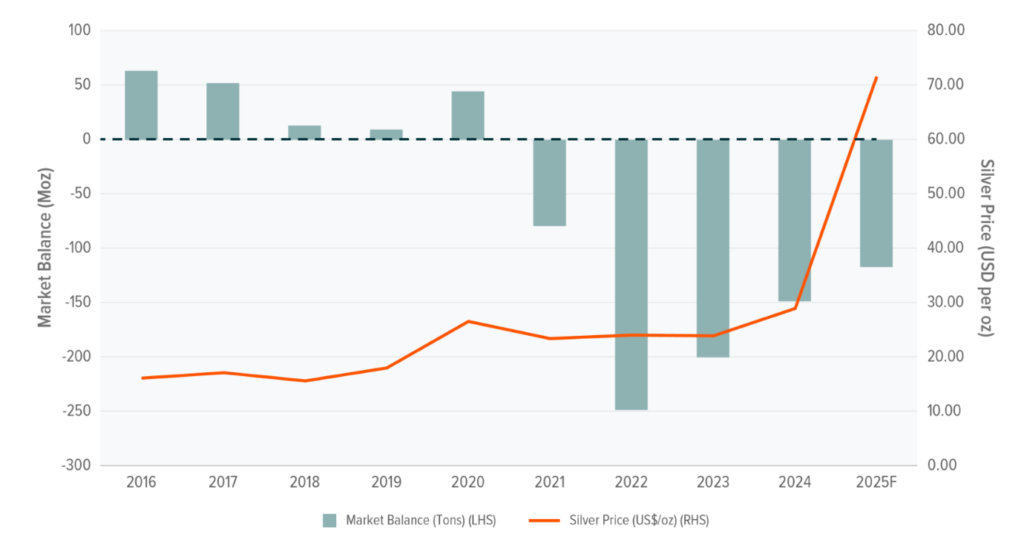

Silver prices are shaped by a mix of monetary and industrial factors, often summarized in empirical models that include gold prices, real interest rates, ETF flows, and industrial activity. Supply shortage while demand accelerated played a critical role in silver’s price in recent years as shown by the following graph.

Source: Globalxetfs

Major drivers of silver price recently:

- Global interest rates and real yields: Lower real yields tend to support precious metals by reducing the opportunity cost of holding non‑yielding assets like silver. Shifts in expectations for central‑bank policy (especially the US Federal Reserve) have therefore been a major short‑term driver for price performance.

- Gold price movements and investor sentiment: Silver often follows gold, with gold acting as the primary monetary benchmark; empirical studies show gold prices explain a large portion of silver’s year‑over‑year moves. When risk appetite for metals rises (e.g., on inflation or geopolitical worries), both metals typically rally.

- Industrial demand cycle: Industrial indicators such as US and global manufacturing PMIs and industrial production correlate strongly with silver demand because so much consumption is tied to electronics, solar, and other manufactured goods. Stronger Chinese and global growth has historically been associated with a tighter gold–silver ratio and better relative performance for silver.

- Solar, EVs, and energy transition: Growth in solar panel manufacturing and the broader energy transition has increased structural demand for silver in PV cells and advanced electronics, partially offsetting the long‑term decline from photography. Expectations for continued grid and renewable‑energy build‑out have become a key medium‑term bullish factor.

- Investor flows and ETFs: Silver ETF holdings and coin/bar purchases reflect monetary demand, and changes in these holdings have been shown to explain a meaningful share of price variability in quantitative studies. Periods of strong retail and institutional inflows (often during inflation scares or speculative episodes) have led to sharp rallies.

- US dollar and currency moves: Because silver is traded globally in US dollars, a weaker dollar (as we have seen most recently) typically supports higher dollar‑denominated silver prices by making it cheaper for non‑US buyers.

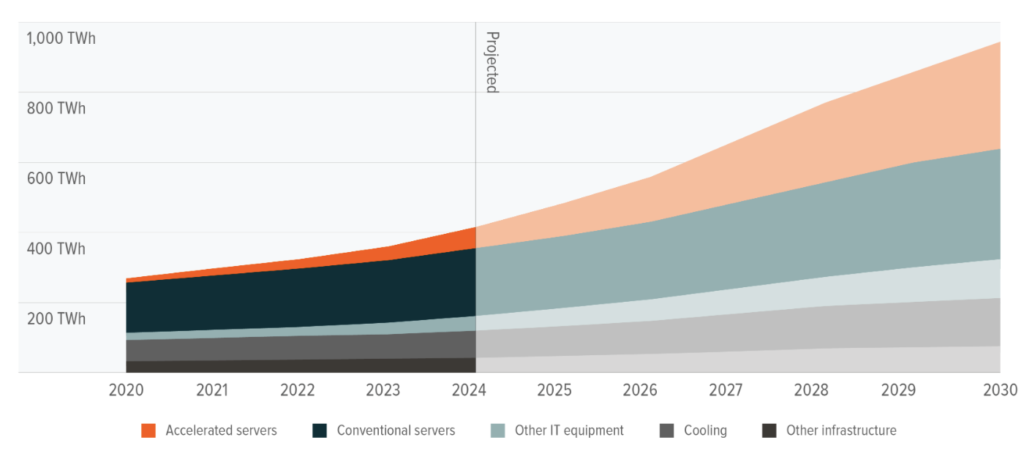

In addition to the above-mentioned factors, the recent shift to AI data centres changed the narrative from cyclical metal to a more sustained critical material. The rapid expansion of AI data centres is emerging as a powerful structural driver of silver demand. Silver’s unmatched electrical and thermal conductivity makes it essential for high-performance chips, power management systems, advanced networking equipment, and efficient cooling infrastructure used in AI workloads. As hyperscalers race to build energy-intensive, high-density data centres, silver usage per facility is quietly rising across servers, connectors, and power grids. This creates a long-term, technology-driven demand tailwind for silver that goes beyond traditional industrial and investment cycles.

Source: Globalxetfs

Role of silver in an investment portfolio

As 60/40 portfolios are not perfect solutions for today’s changing investment landscape, alternative assets making their appeal. Silver can play several roles, but with distinct risks compared with gold. Potential benefits include:

- Inflation and currency hedge: As a real asset, silver can help protect purchasing power during periods of monetary debasement or negative real interest rates, though with more volatility than gold.

- Diversification: Silver’s return profile is not perfectly correlated with equities or bonds, which can help reduce overall portfolio concentration in traditional assets.

- Cyclical upside: Because of its industrial demand, silver has historically outperformed gold during strong economic recoveries and bull markets for commodities.

- Tactical relative trade: Some investors use the gold–silver ratio tactically (e.g., overweighting silver when the ratio is far above its historical average) to seek relative value.

Key risks and considerations:

- Higher volatility: Silver’s annual price fluctuations and drawdowns are historically much larger than gold’s, with analyses showing significantly higher variability and bigger peak‑to‑trough losses.

- Sensitivity to industrial cycle: Weak manufacturing or a slowdown in China and other key economies can weigh more heavily on silver than on gold.

- Liquidity and product choice: Investors must choose between physical bullion, coins, ETFs, mining equities, and derivatives, each with different risk, cost, and storage profiles.

In practice, portfolio allocations that include precious metals often tilt more toward gold for stability, with a smaller allocation to silver to add cyclical and higher‑beta exposure. We at Simply Ethical gave a decent allocation to both gold and silver couple of years back purely for portfolios diversification and optimisation purposes, which helped to add in the return profile of different portfolio prepositions. We are still maintaining a sizeable allocation to them backed by the factors highlighted in this article. You can explore different investment portfolios here (including Personal Pensions, ISAs, and General Investment Accounts) that best describes your risk/return profile and investment objectives.

Silver – historical performance:

Source: Tradingeconomics

Outlook for silver

Silver’s outlook reflects a tug‑of‑war between its monetary and industrial roles.

Constructive factors:

- Structural demand from solar and the energy transition is expected to remain strong, supporting baseline industrial consumption.

- If global growth stabilizes or improves, industrial demand and investor risk appetite could favour silver over gold, potentially compressing the elevated gold–silver ratio.

- A sustained environment of low or falling real interest rates and continued concerns about debt, deficits, or currency debasement would tend to support precious metals, including silver.

- Silver’s categorisation into critical minerals’ list adds another layer to its appeal.

Headwinds and risks:

- A significant global slowdown or recession would likely weigh on industrial demand, which could offset some monetary‑safe‑haven benefits for silver and keep volatility high.

- Technological changes that reduce silver intensity in solar cells or allow substitution by other materials could moderate long‑term demand growth.

- If central banks continue to focus their official‑sector purchases on gold rather than silver, gold may retain a structural performance edge as a reserve asset.

Summary table: gold vs silver

| Feature | Gold | Silver |

| Main demand drivers | Central‑bank buying, jewellery, investment | Industrial uses (electronics, solar, EVs) plus investment |

| Typical volatility | Lower | Higher (larger percentage swings) |

| Role in portfolios | Defensive store of value, crisis hedge | Higher‑beta precious metal, cyclical/inflation hedge |

| Long‑run average ratio | – | Gold–silver ratio ≈ 60:1 long‑term average |

| Recent ratio levels | – | Approximately 46:1 to 47:1 as of late January 2026 |

Putting this together, many experts see silver as having asymmetric potential – higher upside than gold in a pro‑metal, pro‑growth or inflationary environment, but also more downside risk in a hard landing or if industrial demand underperforms. For a diversified investor, that suggests using silver as a smaller, higher‑beta complement to gold rather than a direct substitute for it.To explore our range of tax-efficient investing solutions (ISAs, JISAs, SIPPs) as well as other investment management products and financial advice service, visit our website here.

To learn more about how we can help you and our investment approach, book a free initial consultation with one of our Financial Advisers.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.