Year 2025 was both challenging as well as exciting for the economies and financial markets. Here is a comprehensive “2025 Year in Review” covering key global trends across macroeconomics, technology (especially AI and data centres), financial markets, geopolitical developments, and trade policies.

1. Macroeconomic Landscape

Global growth & inflation

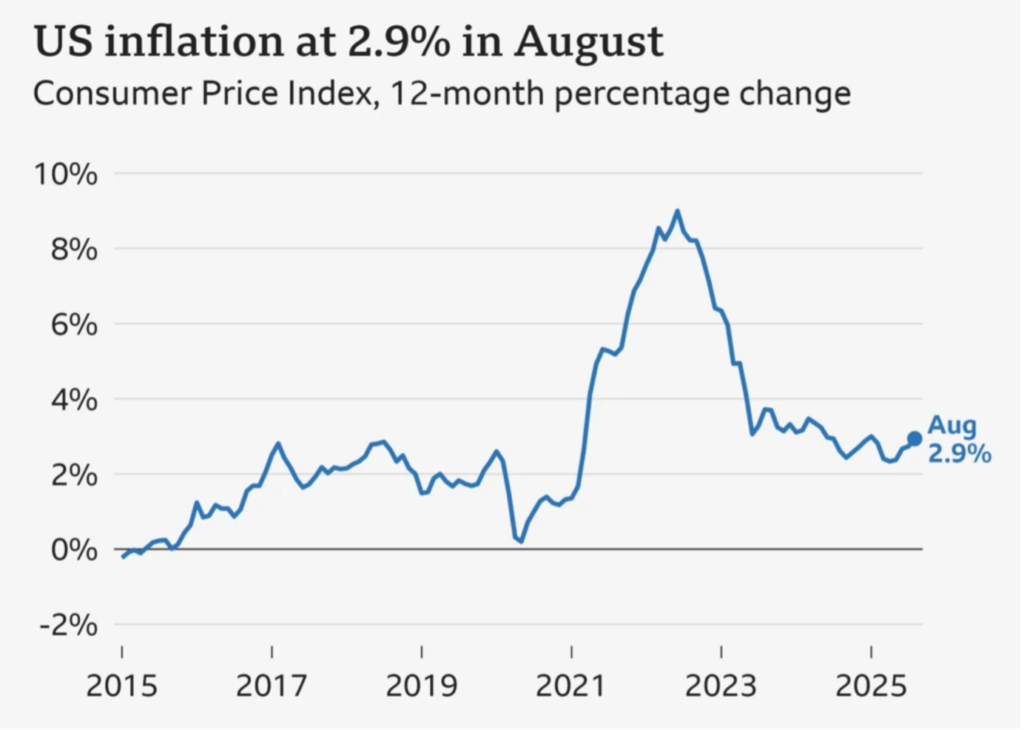

In 2025, global economic growth was modest and uneven. According to IMF forecasts, world growth remained subdued at around mid-to-low single digits, with developing economies slightly outperforming advanced ones. Inflation cooled globally toward 3-4% after multi-year highs in earlier years, though divergence persisted: the U.S. and some EMs saw stickier inflation while much of Europe approached central bank targets.

Key points:

• United States: Growth remained resilient albeit slowing from earlier post-pandemic rebounds. Inflation remained above targets but trending downward.

• Eurozone: Growth was moderate with inflation near ECB goals, providing policy room for gradual easing.

• China: Continued to grow around 5% but faced structural headwinds from property sector weakness and demographic challenges.

• India: Strong outlier with growth around 7%, driven by domestic investment and services expansion.

Unemployment & labour markets

Global unemployment stayed relatively low compared with decade averages, though tight labour markets in the U.S. and Europe coexisted with slower job creation in parts of Asia. Wage growth moderated, balancing inflation pressures without triggering sharp rate increases.

Interest rates

2025 was largely a transition year for monetary policy:

• Central banks in advanced economies mostly pivoted from tightening to a cautious easing cycle or held rates at elevated levels.

• Persistent inflation concerns limited outright cuts until late in the year.

• This evolving backdrop supported equity markets while tempering bond yields.

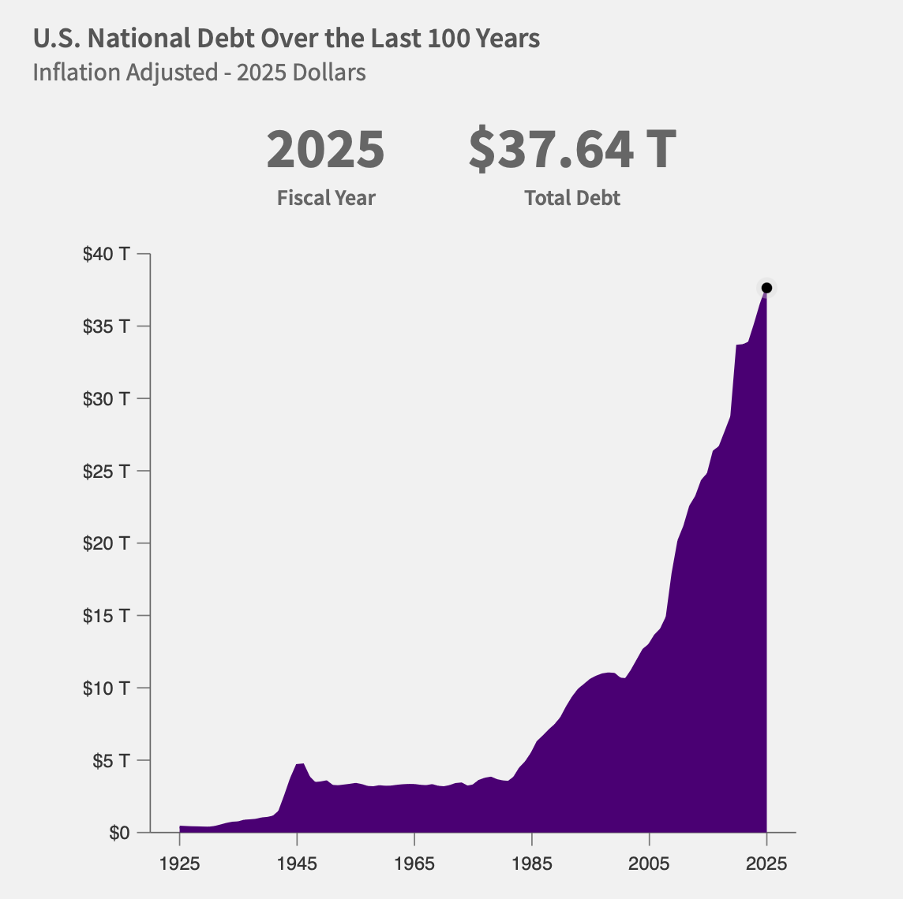

Government Debt

Fiscal deficits and high government debt remained a legacy concern from prior pandemic and stimulus spending. While debt servicing costs edged down with softer yields, major economies continued to grapple with structural budget pressures, especially Japan, Italy, and the U.S.

2. AI Technology & Infrastructure Boom

AI advancements

2025 was defined by both enthusiasm and introspection in AI:

- Generative AI and deep learning continued to diffuse across sectors, from healthcare to finance.

- China touted national scientific progress and AI breakthroughs, tying tech development to broader strategic goals.

- Global dialogue intensified on responsible AI use, with major summits such as the AI Action Summit convening policymakers and industry leaders.

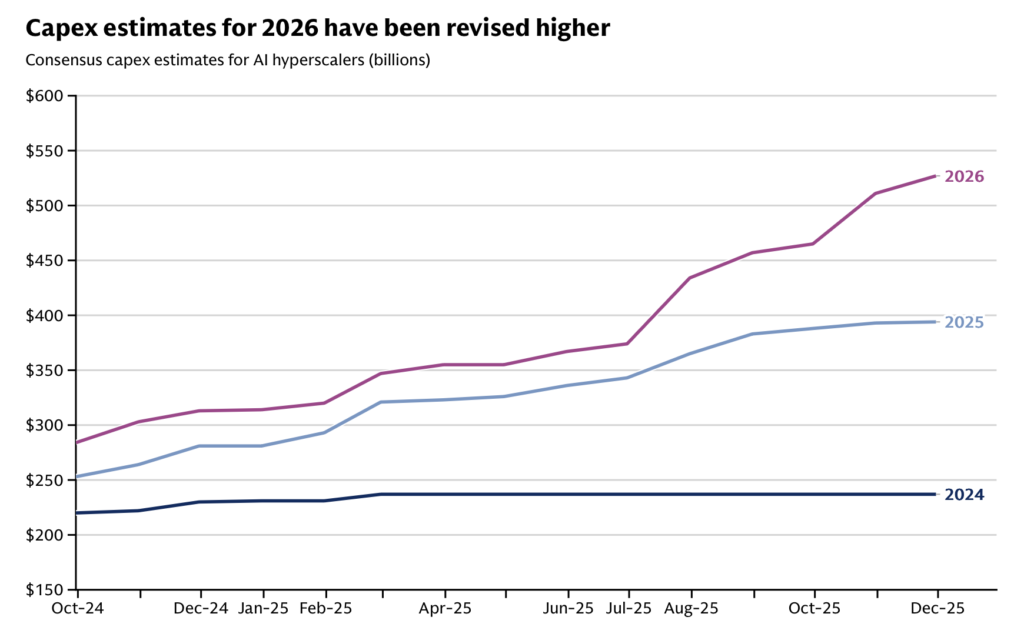

Data Centre and AI CapEx

AI-fuelled infrastructure spending surged in 2025, with hyperscalers and cloud providers driving massive investments in compute facilities:

- Major U.S. tech companies each committed tens of billions to AI-optimized data centres globally.

- Industry forecasts projected global AI spending going up significantly, with infrastructure (data centres, semiconductors, supporting power & cooling) absorbing a substantial share.

- Large projects like OpenAI’s “Stargate” data centre network illustrated the scale, expected commitments north of hundreds of billions over several years.

Data centre expansion became a structural growth engine, boosting capex, job creation, and technological capability, though questions lingered about productivity payoffs and energy demands.

Source: Goldmansachs

3. Financial Markets Performance

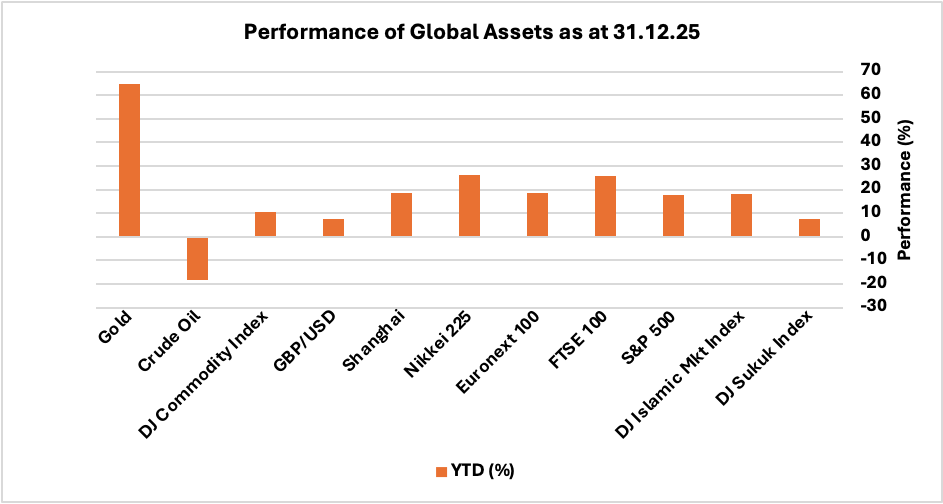

Looking at the performance of major asset classes, key indices exhibited strong performances mainly driven by AI technology revolution although investors continued to remain concerned about macroeconomic factors, geopolitical environment, and sector-specific drivers. In the equity markets, Japan’s Nikkei 225 index was a star performer that surged 26.20% in 2025 driven by corporate reforms while UK FTSE 100 finished the year on the strong footings, delivering a 25.8% yearly gain, outperforming many peers on strong mining and defence gains and easing monetary policy. The U.S. equity market benchmark S&P 500, European equity market Euronext 100, DJ Islamic market index, and China’s Shanghai Composite, all delivered close to 18% yearly gains supported by AI tech enthusiasm. In response to easing narrative around monetary policies, yields moved lower that helped DJ Sukuk Index end the year with 7.6% upside. Gold continued to shine as a strong bet for safe haven and standout performer with gain of 65%. Crude oil was the only loser that plunged roughly 18% amid oversupply and weaker demand growth. Lastly, UK pound gained 7.45% against US dollar as the later experienced a multi-year weakening trend, supported by rate expectations and fiscal dynamics.

The following snapshot provides a detailed breakdown of the performance of different asset classes in 2025, offering a comprehensive overview of market dynamics during a period marked by both AI-driven optimism and lingering uncertainty around macroeconomic environment.

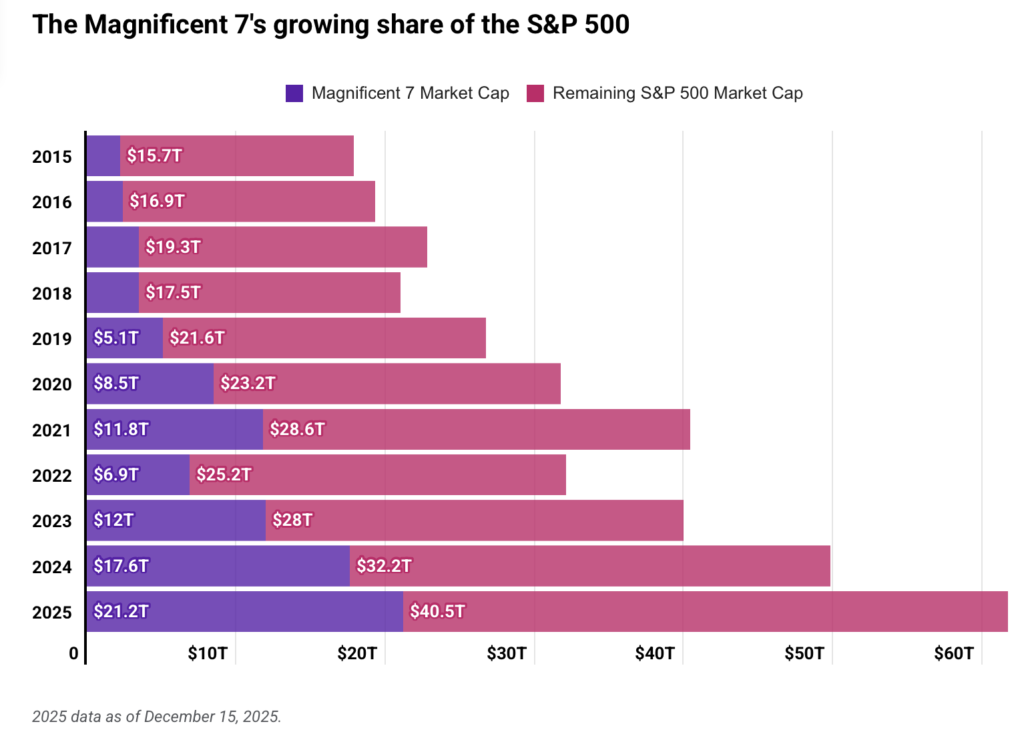

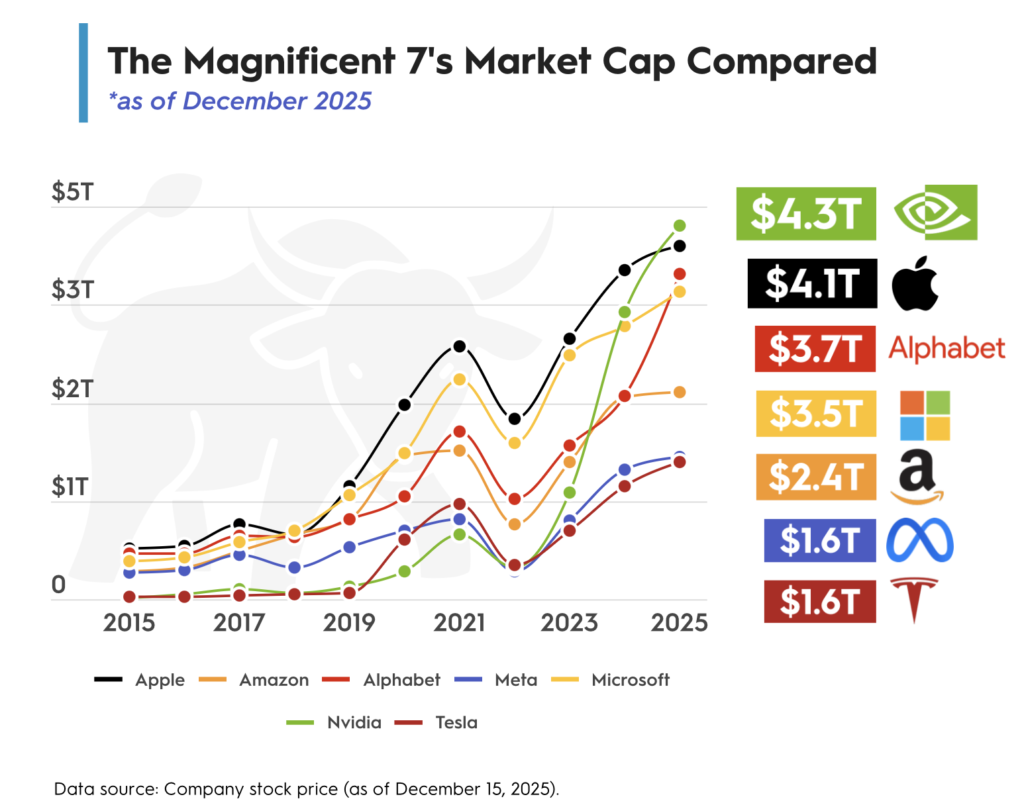

Magnificent Seven vs. S&P 500

The so-called Magnificent 7 (Apple, Alphabet, Amazon, Meta, Microsoft, Nvidia, Tesla) dominated headlines:

- Their combined valuation accounted for roughly a third of the S&P 500 by year-end 2025.

- However, performance was mixed: some members (e.g., Nvidia, Tesla, Alphabet) outpaced the S&P 500, while others lagged.

- Broad market advance was supported by strong corporate earnings, but concentration risk remained a key concern among strategists.

Source: Motley Fool

Nvidia led the AI Tech boom

Within the Magnificent Seven, Nvidia clearly emerged as the standout beneficiary of the AI technology boom in 2025. Explosive demand for AI accelerators and data-centre GPUs drove strong revenue growth, margin expansion, and repeated earnings upgrades. Nvidia’s dominant position in AI hardware, software ecosystems, and hyperscaler partnerships reinforced its leadership across global equity markets. As a result, its share price significantly outperformed both its mega-cap peers and the broader technology sector during the year.

Source: Motley Fool

4. Geopolitical Landscape

Russia–Ukraine

The Russia–Ukraine conflict remained unresolved, continuing to affect energy markets, defence spending, and European stability throughout 2025.

Middle East

Tensions involving Israel, Hamas, and Iran shaped risk pricing in markets and commodity outlooks. While localized eruptions caused periodic spikes in energy prices, global oversupply limited long-term price escalation.

U.S.–China Relations

Relations between the U.S. and China remained competitive and complex:

- Strategic rivalry in technology and AI intensified.

- Trade tensions and tariff threats led to market volatility, especially in Q1–Q2.

- Some tariff pressures eased later in the year via negotiation, helping restore market confidence.

- China promoted national self-reliance in high-tech sectors while managing slower growth.

5. Trade Policies & Tariffs

Protectionism & Tariff actions

2025 witnessed notable trade policy shifts:

- The U.S. implemented broad tariff measures on imports, triggering early-year market corrections before partial retreat and negotiation.

- Retaliatory responses from trading partners maintained friction, particularly between the U.S. and China.

- Europe and Asia navigated tariff implications with targeted trade agreements aimed at stabilizing supply chains.

- Overall, trade policy uncertainty weighed on global investment planning and contributed to cautious business sentiment.

6. Structural & policy implications going forward

- AI productivity: Heavy AI capex spending highlighted a structural transformation, but questions persist about when broader productivity gains will materialize beyond tech sectors.

- Market concentration: Equity advances underscored both investor confidence and structural risk due to concentration in a few mega-cap tech names.

- Energy transition: Slowing oil demand and rising metals demand linked to EVs and renewables pointed to long-term structural shifts.

- Geopolitics & growth: Persistent geopolitical risks and trade barriers injected volatility into markets and economic forecasts, underscoring the need for adaptive policy frameworks.

Summary:

2025 stood as a year of continuity and change, modest global growth, cooling inflation, record equity gains, an AI infrastructure boom, divergent commodity trends, and shifting geopolitical and trade dynamics. Markets and economies showed resilience, even as structural shifts and policy uncertainties shaped the narrative.

To explore our range of tax-efficient investing solutions (ISAs, JISAs, SIPPs) as well as other investment management products and financial advice service, visit our website here.

You can book a free consultation with one of our Financial Advisers to learn more about our investment approach and how we can help you.

Disclaimer

This article is for information only. Please do not act based on anything you might read in this article. Past performance is not a reliable indicator of current or future returns. This article contains general information only and does not consider individual objectives, taxation position or financial needs. Nor does this constitute a recommendation of the suitability of any investment strategy for a particular investor. It is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy to any person in any jurisdiction in which such an offer or solicitation is not authorised or to any person to whom it would be unlawful to market such an offer or solicitation.

When you access a shared link of third-party websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites.